If you were taking a break from your family on Christmas Day, you may have caught my article on how Jay Powell’s recent “hawkish cut” is set to light a fire under high-yielding (and tax-free!) municipal bonds.

Here’s why: Jay cut rates by a quarter point in December, but gave investors a stern pre-holiday “talking-to,” with the Fed slashing its rate-cut forecast to two from four in 2025.

Stocks, as you’d expect, threw a one-day fit. But here’s the thing: The yield on the 10-year Treasury note (the so-called “long end” of the yield curve, which has a mind of its own) spiked.

In other words, the Fed cut but interest rates still rose.

The bond market is clearly telling Jay, in no uncertain terms, that the job on inflation is not done. And finally, he appears to be listening. Which is where our contrarian opportunity in muni bonds comes in.

“Adult in the Room” Jay Set to Trigger the Next Muni-Bond Rise

You and I both know that everyone is expecting inflation (and therefore interest rates) to head higher under Trump 2.0. And in the longer run, that may be true. But, contrarians we are, we also know that when everyone expects something to happen, something else usually does.

What we’re talking about here may be the first investment surprise of 2025: That rates top out and turn lower thanks to Jay’s new-found sternness. As they do, bond prices will rise.

Rates down, bonds up. That’s just the way it goes in bond-land.

And today’s high 10-year yield means bonds are despised right now. Did someone say “despised”? We’re interested! Especially when we can tap these “loathed” income plays for some of the safest, highest (not to mention tax-advantaged) dividends on the board: those paid out by municipal bonds.

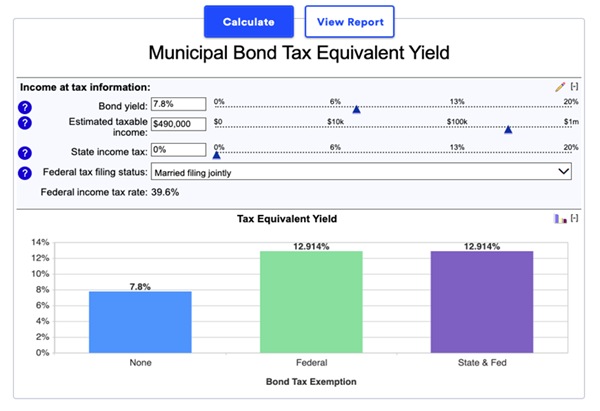

Muni-Bond CEFs: Our Source of Steady 7.8% Dividends (and 0% Taxes)

“Munis” are issued by state and local governments, mainly to fund infrastructure projects. The key thing we love about them is that, for most Americans, muni dividends are tax-free. That can amount to a lot—especially for those in the top tax bracket.

As you can see below, to get the equivalent of a 7.8% tax-free muni-bond dividend—the payout on the closed-end fund (CEF) we’ll delve into next—a top-bracket taxpayer would need a 12.9% yield on a taxable payout, like that on a stock.

Source: Bankrate.com

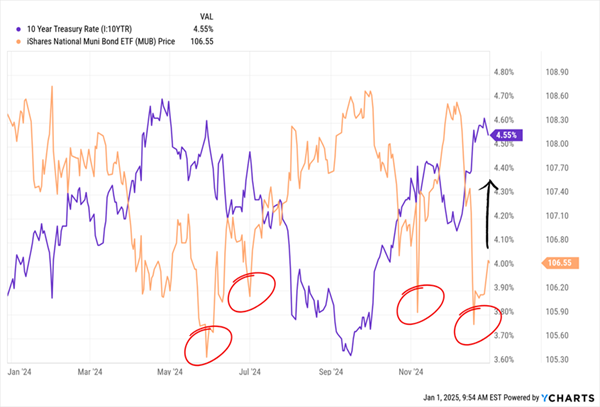

Upside? Well, the relationship between munis and the 10-year Treasury rate is clear in the chart below. If you’d bought the muni-bond benchmark ETF, the iShares National Muni Bond ETF (MUB) each time rates peaked, you’d have grabbed yourself some nice upside.

Buying Munis on The Dip Always Pays (and Our Next Buy Window Is Here)

But we’re not buying MUB, for a couple reasons:

- Wimpy payouts: MUB yields just 3% as I write this.

- No discounts: Since ETFs (unlike CEFs) can issue new shares at will, they always trade at (or close to) their portfolio values. As I write this, MUB trades at a 0.15% discount to net asset value (NAV)—basically zero!

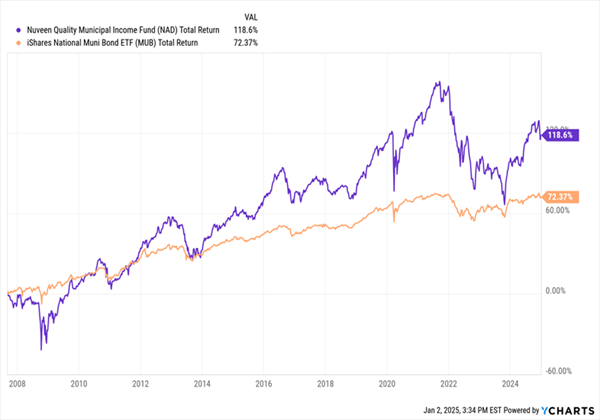

Instead, we’re buying the most discounted muni-bond CEF held by my Contrarian Income Report service, the Nuveen Quality Municipal Income Fund (NAD).

As mentioned, this one kicks out a 7.8% tax-advantaged yield, and that payout comes our way monthly. That drives the 12.9% taxable-equivalent yield we saw above, for my top-bracket ballers.

But the discount is the straw that really stirs the drink here. As I write this, NAD trades at an unwarranted 8.3% discount to NAV. That’s well below its pre-election peak of 5.5%. And consider that back at the end of 2021, before the Fed’s last rate-hike cycle started, NAD was close to par.

Both of those numbers suggest that today’s discount, with rates looking at a fair bit of upside resistance from here, is overdone.

And when it comes to past performance, NAD is a lock, helped by the team at Nuveen. They manage $429 billion worth of bonds. When municipalities issue bonds—or think about it—they call the big whale Nuveen. The muni giant throws its purse around to secure the best deals for its investors.

That’s helped NAD (in purple below) outrun MUB over the last 17 years or so, since MUB’s launch:

NAD Delivers a Double (All in Dividend Cash)

Sure, NAD’s return was more volatile than that of the ETF, but remember that reinvested dividends drove this gain, so NAD investors were getting more liquidity than MUB holders, who had to rely more on price gains due to the fund’s lame dividend.

This also shows how important it is to hold these funds for the long haul to reap the biggest tax-advantaged returns from them. And of course, those tax advantages are sweeter when you apply them to a 7.8% current yield than they are on a 3% payer!

When it comes to munis (or any bonds, really), we need to pay attention to two key risks: duration risk and credit risk.

Credit risk is a non-issue with NAD, thanks mainly to munis’ safety, with default rates in the basement, below 0.1% since 2013. With 1,171 bonds in its quiver, even in the unlikely case that one did default, the impact on the portfolio would be microscopic.

Duration risk? That, in a nutshell, is the concern that higher rates in the future will make the yields on the fund’s current holdings look lame. But if rates top out and move lower, long-duration bonds rule, and NAD only has about 13% of its holdings maturing in the next 13 years. Its average duration, adjusted for leverage, is a lengthy 12.5 years.

Speaking of leverage, the fund borrows against 40% or so of its portfolio, which magnifies its returns in an up market and, yes, can magnify losses when markets drop (which is why NAD’s performance is more volatile than that of MUB in the last chart we looked at).

Here, we trust Team Nuveen to deftly throttle leverage as conditions change. Lower rates would mean NAD’s current leverage would give its price an extra lift. And, of course, the fund’s borrowing costs would dip, too, further supporting our high (and tax-free) payouts.

This Urgent 2025 Buy (11% Yield!) Is Set to Drop Its Next BIG Payout

NAD, with its huge tax-free dividend, is a great buy for 2025. With a payout like that (and proven long-term performance), it’s a lifeline for the year ahead, which I expect to be more volatile than 2023 or 2024.

That’s our theme for 2025: Big, safe dividends that allow us to keep our bills paid (and our retirement fully funded) no matter what happens with the Fed or the markets.

Buy NAD Now—But Don’t Forget to Grab This 11% Payer, Too

Which brings me to the other big payer I’m pounding the table on now. Not only does this 11% payer have a long history of keeping its huge payout rolling shareholders’ way—it sports a history of dividend growth, too.

This exclusive pick is the ultimate investment for 2025, and I don’t want you to be left without access to its huge, steady cash stream. And with its next big payout set to drop soon, the time to get in is now.

When you look back on this buy in early 2026, I think you’ll be thrilled at the double-digit income stream you’ve collected. But that won’t happen if you don’t make your move right away. Click here to learn more about this incredible 11% payer and get in line for its next regular payout.

Recent Comments