No matter the financial headlines, all roads will—eventually—lead to (even higher) inflation. So, we should use pullbacks and rallies alike to make sure we are inflation-protecting our retirement portfolios.

We’ll talk specific stocks and funds in a moment. First, let’s review the mechanics of money printing.

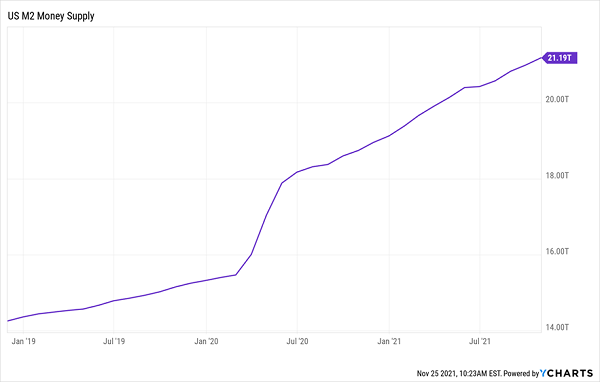

The accommodative Federal Reserve has already increased the M2 Money Supply by 38% since the start of 2020! That’s a lot of dough that has flowed into the financial markets. With the Fed continuing to stand by to support the stock and bond markets, we should look past current concerns and realize that the “solution” to any setbacks will be more easy money.

Hence, our focus on inflation. Now the playbook for inflation-proofing is going to be different this time. Gold is 1970s thinking! When inflation strikes, we want to go on offense, buying up dividend payers whose payouts offset inflation and whose businesses wring big profits from it.

(I’ll have two corners of the market—and two cash-flush stocks yielding 5%, with double-digit upside—for you shortly.)

How Buying Gold Would Have Handed You a 7.7% Loss

To see how outdated thinking can cost you when inflation hits, let’s wheel back and talk about gold for a second. If it’s such a great inflation hedge, why has it fallen in the past year as inflation worries hit?

Gold Steals Investors’ Money Faster Than Inflation

That’s right, gold, as tracked by the SPDR Gold Shares (GLD), has dipped 1.5% as I write this, so if you add the erosion caused by the 6.2% year-over-year inflation rate we saw in October (as measured by the consumer price index), the money you have parked in gold is actually worth 7.7% less! (I mention GLD because if you are keen to invest in gold, it’s the best way to do so—it simply tracks the gold price, saving you the cost of storing gold bars and coins.)

That’s why we offensive-minded dividend investors shun gold. Another is that we want dividends! Gold bars pay none, gold miners typically pay little (if anything), and GLD yields zip, too.

With a healthy dividend, you’ve already got a head start on inflation in the form of quarterly payouts. Then you can “tack on” price gains as these inflation-loving businesses rack up big profits.

Look to “Fed Fueled” Dividends Yielding 5%+

But where do we find these dividend darlings? We’ll look to two corners of the market directly benefiting from the wave of cash rolling off Fed Chair Jay Powell’s money printer bond-buying program.

And when I say “wave,” I’m not kidding! Consider that 38% of all greenbacks in circulation have been “created” since the pandemic hit in March 2020.

And unlike in 2008, where the cash the Fed used to buy bonds mainly stayed with banks, this time we sent out checks, so the cash did get into the economy, fueling inflation. And with Americans holding some $3.7 trillion in savings, according to Oxford Economics, it’ll be a while before it works its way through the system.

No Way This Isn’t Inflationary

That means we have time to work this fiat money to our advantage. So let’s get to the first sector that’s cashing in on that spending.

This 5%-Yielding CEF Will Profit When Rates Rise

Our first Fed-fueled money-maker is the finance sector, which profits as the gap between yields on the 10-year Treasury note, pacesetter for the loans banks make to customers, rises, while the Fed’s key lending rate (at which banks lend to one another) stays at essentially zero. And whenever rate hikes start, it’ll still be a long time before they reach pre-pandemic levels.

In any event, I expect Treasury yields to break over 2%, and possibly go as high as 3%, in the months ahead (though perhaps with a slight delay if the new COVID variant ends up slowing economic activity). That doesn’t sound like much, but a move to just 2% is a 25% rise from here, which would be a boon to bank profits.

A nice play here is the John Hancock Financial Opportunities Fund (BTO). The closed-end fund (CEF) yields 5.2%, held its payout steady through the crisis and is in good position to raise it, given the 55% return its underlying portfolio (known as the net asset value, or NAV) has posted in the past year.

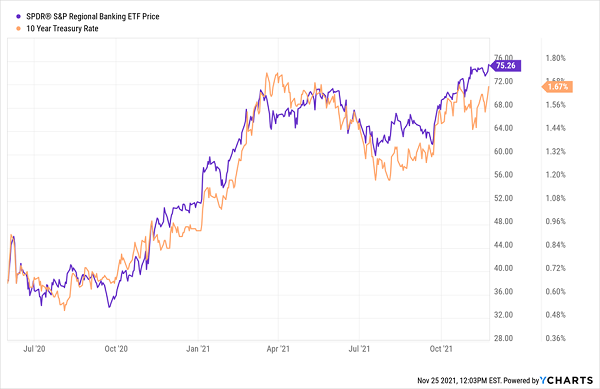

The fund targets regional banks: top holdings include Huntington Bancshares (HBAN), Fifth Third Bancorp (FITB) and U.S. Bancorp (USB). That’s a savvy setup, as we discussed in my October 19 article, because smaller lenders are especially sensitive to a rise in Treasury yields, as you can see below, with the SPDR S&P Regional Banking ETF (KRE) tracking Treasury yields higher over the 18 months leading into the Thanksgiving holiday:

Treasuries Call, Small Banks Answer

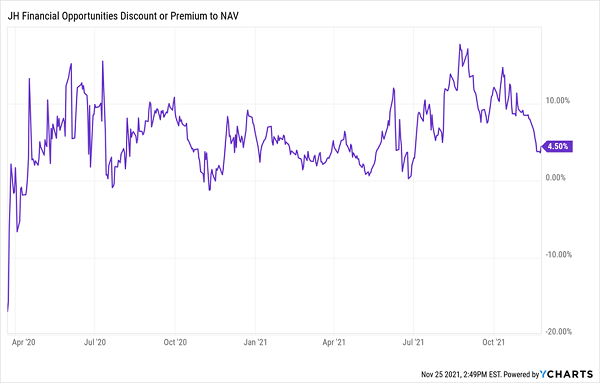

Then there’s BTO’s discount to NAV, a critical indicator for CEFs. As I write, the fund’s market price is trading at a 4.5% premium to NAV. Normally we demand a discount with CEFs, but with some, like BTO, a discount hardly ever appears.

That’s when we have to look to history, and as you can see below, the fund’s current premium is on the low end of its range since the crisis began—as recently as late August, BTO traded at a ridiculous 17% premium!

BTO Is Never “Cheap”

So even if its premium returned to double digits (reasonable, in my view), you’d be looking at strong price upside here, before accounting for NAV gains (and not including your 5% dividend, either).

Oil: Our Crash ’n’ Rally Play Will Roll On

The black goo has gone crazy as a result of the Fed’s actions, and I expect it to end up above $100 when supply and demand eventually balance out, in the usual two-steps-forward, one-step-back pattern. Its latest pullback, on fears of a new COVID variant, has given us an opening.

Here’s how oil’s predictable crash ‘n’ rally pattern, which comes our way about once a decade, plays out:

- Demand for oil evaporates and its price crashes (2008 and 2020).

- Energy producers scramble to cut costs, so they cut production aggressively (2009 and 2020).

- The economy slowly recovers (2009 and late 2020), energy demand picks up, but supply lags.

- And lags. And lags. And the price of oil rallies until supply eventually meets demand (2009 to 2014 and 2020 to present).

And there is oil out there to be tapped, with the US alone sitting on 47.1 billion barrels of proven reserves, as of the end of 2019 (the latest figures available), according to the US Energy Information Administration.

That’s enough to meet America’s needs for seven years, without considering imports, and it should keep the price slowly rising as shale producers cautiously open the taps, as they’ve been doing, having been burned by overproduction before.

A savvy dividend play here is integrated oil major Chevron (CVX), payer of a 4.7% yield as I write this.

That payout is backstopped by the company’s free cash flow (FCF), which, as I wrote in an August article, has nearly bounced back to pre-pandemic levels as oil prices—and demand—pick up. That’s pulling the share price along with it:

Bouncing Cash Flow Fires Up Chevron Stock

If we look at the latest quarter (a reasonable approach, given the beating Chevron’s—and all oil majors’—FCF took in late 2020), we see that the dividend accounts for 39% of FCF, which is very safe—and likely to result in a significant hike, given the rocket ride FCF is on. That would lift the shares as investors note the higher payout and jump in.

Finally, let’s talk valuation: even though the stock has nearly doubled since March 2020, we can still get in at a reasonable 14-times forward earnings. Management knows that’s a sweet deal—the company bought back $650 million of shares in the third quarter and plans to buy $750 million worth in the fourth.

Those buybacks (which inflate earnings per share—and share prices with them), plus Chevron’s attractive valuation and likely dividend growth, hand us strong upside potential. That’s before we talk about a shortage-driven rise in oil prices.

7 MORE Fed-Fueled Stocks to Buy Now (With Safe Dividends Up to 7.4%)

These are far from the only opportunities rolling our way courtesy of the Fed’s printing press—which, make no mistake, will keep printing over the coming months.

In fact, I’ve got 7 MORE “Fed-Fueled” stocks I see as even better buys than these two. They boast solid dividends up to 7.4% that are built to keep paying us reliable income no matter what the economy throws at us—inflation, deflation, new virus variants, you name it.

And like Chevron and the regional banks held by BTO, they’re perfectly positioned to net the new cash the Fed is pouring into the market, setting you up for strong double-digit upside in addition to the huge dividends they pay.

If the market tumbles from here? No problem—due to their Fed-fueled business models and attractive valuations, I expect these 7 stocks’ prices to hold up just fine, letting you collect their huge cash payouts in peace.

Now is the perfect time to buy these 7 Fed-fueled dividends. I’ve got full details on all 7 of them waiting for you right here, including their names, tickers, current yields, my unvarnished take on their management teams and everything else you need to know before you buy.

Recent Comments