Successful dividend investing is simple, though not necessarily easy. There are nuances which trip up many investors (including most professionals!) These twists and turns create “yield alpha” opportunities for contrarian-minded income investors like us.

If everyone else in the market were perfectly grounded and calculated, there would be no chance for us to make above-average returns. After all, the 11.3% and 17.5% annualized returns that my Contrarian Income Report and Hidden Yields readers are earning would be snapped up in a perfectly efficient market.

Thanks to these inefficiencies, we are able to bank big yields and price returns in Dividend Land. Ready to retire on dividends? Follow these seven steps and we’ll do it together. Let’s start with an obvious yet underappreciated rule for income investors.

Step 1: Count Your Dividends

Since we focus on high yield, most of our returns come from the “yield” component of stocks. So let’s not forget about them when figuring out our returns!

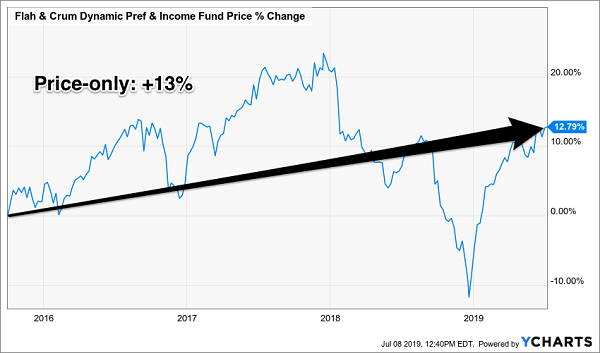

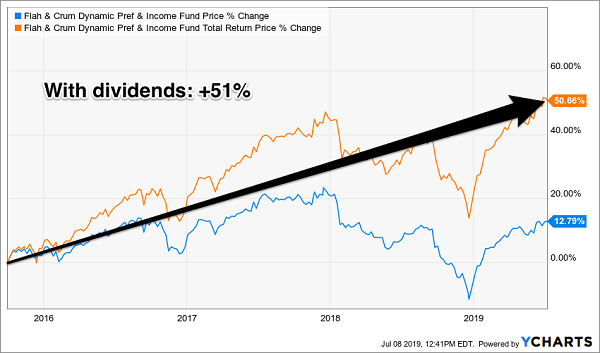

For example, we added this preferred stock fund to our portfolio in October 2015 and its price-only returns look quite pedestrian:

Don’t Fixate on Price Alone…

We’ve gained 51%, while the price is up only 13%. The majority of our fat 51% gains have been delivered via cash dividends. So let’s make sure we add in the orange (top) line below to reflect the big driver of our profits!

… Remember to Add Those Dividends!

Step 2: Find Price Upside, Too

While we could build a portfolio that’s 100% invested in these types of safe bonds and do just fine, we’re better off putting 50% or so of our cash in stocks. The upside is too good to ignore.

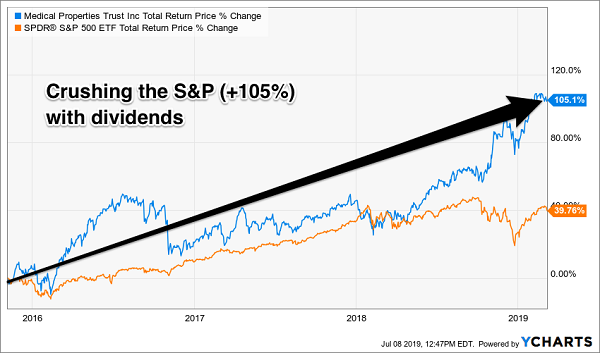

Dividend growth is, over the long haul, the main driver of higher stock prices. We added this stock in November 2015 and received three dividend raises over the ensuing three-and-a-half years. The result? We enjoyed 105% total returns and really crushed the broader S&P 500:

Why We Buy Dividend Stocks, Too

Step 3: Monitor Dividend Coverage

A dividend hike is the ultimate sign of dividend safety, so I prefer stocks that consistently raise their payouts. The likelihood that a company is going to raise its dividend (or cut it) is directly related to its payout ratio, or the percentage of its profits (or cash flows) that it is dishing out to shareholders as dividends.

As a rule of thumb, a payout ratio below 50% is a sign of dividend safety. Some capital efficient firms can pay more and real estate investment trusts (REITs) can pay up to 90% of their cash flows as dividends.

It depends on the company (and if you don’t feel like following the payouts and cash flows of 20 stocks and funds yourself, I’ll gladly do it for you as part of your subscription!)

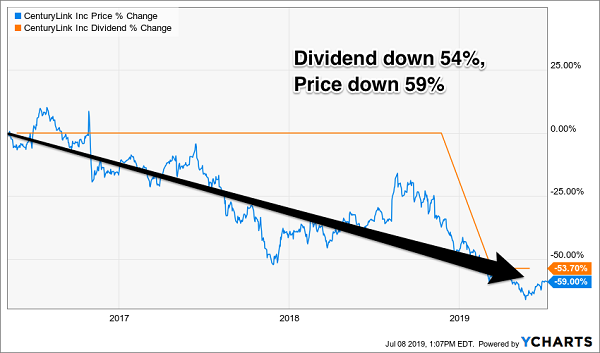

Dividend cuts are no fun. Not only are they a monthly pay cut for us, but (worse) they destroy capital. Take the case of CenturyLink (CTL), which has been writing its investors dividend checks that it couldn’t cash since I called out this “paper telecom tiger” in May 2016 (and many times since!)

At the time, CTL was paying out 135% of its earnings as dividends. The company wasn’t growing profits, either, so the payout eventually had to go. Mr. Market eventually sniffed this out and CTL’s management team finally made the inevitable cut earlier this year:

Stocks Rise and Fall with Their Dividends

Remember the rising dividend that drove our gains in step two? The opposite happened to unfortunate CTL investors here, as their stock’s price dropped 59% while they received a 54% pay cut!

Step 4: Don’t Fight the Fed

“Don’t Fight the Fed” was chapter four in investing wizard Martin Zweig’s legendary book Winning on Wall Street. Here’s why we’ll make it step four here.

Zweig devoted 40 thoughtful pages to teach readers why they should “go with the flow” with respect to the Fed’s trend at any given moment.

Is the Fed raising rates? Then we should favor floating-rate bonds because their coupons (and values) tend to tick higher as rates climb.

Has the cycle topped? When the Fed is prioritizing “easy money,” we should trade in our floaters for fixed-rate bonds, which gain in value as rates fall.

Step 5: Favor Out-of-Favor

What did our winners in step one and two have in common? Two things:

- They were well run, and (most importantly)

- We bought them when each was out-of-favor.

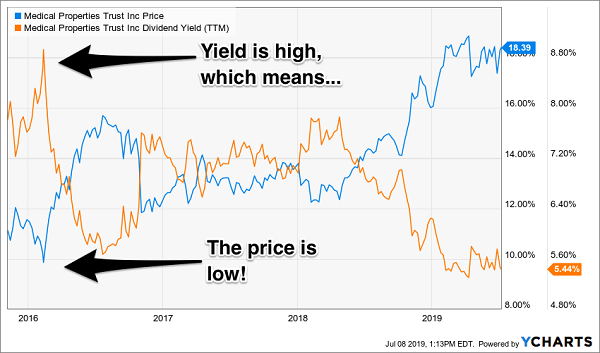

Contrarian investing should be uncomfortable. We want to buy stocks when their yields are high with respect to their norms. To put it plainly, we want to buy this stock when our “dividend per dollar” (as reflected by the orange line) is high. It means the price is low!

High Historical Yield Meant Low Price

And likewise we want to purchase closed-end funds (CEFs) when they are trading at discounts to the value of the assets on their books. This is a unique feature of CEFs because they trade like stocks, with fixed pools of shares. They can and will trade at premiums and discounts to their portfolios, which means we can sit back and wait for bargains.

Step 6: Get (and Stay) Fully Invested

The stock market goes up about two-thirds of the time. Permabears miss out on compounding and it’s not as easy to be a part-time bear as it sounds.

To illustrate this let’s consider a study by Hulbert Financial. The firm looked at the best “peak market timers”–the gurus who correctly forecasted the bursting of the Internet bubble in March 2000 and the Great Recession in October 2007.

These were the clairvoyant advisors who had their clients out of stocks and mostly in cash when the S&P 500 was about to be chopped in half. Surely their clients did great over the long haul, given their capital was largely intact at the market bottoms, right?

Wrong. None of these advisors turned in top performances. The reason? While they were good at timing tops, they were terrible at timing bottoms! The bearish advisors didn’t get their clients back into stocks anywhere near the bottom. They had their capital intact, but they didn’t deploy it–and they largely missed out on the epic bull markets that followed these crashes.

Think about the advisors and investors who sold in late December when the “bear market” became official. They moved to cash at the worst possible moment and have been on the sidelines waiting for a low risk “retest” of the lows. Mr. Market loves to confuse the most amount of people, and he really outdid himself this time!

Barely a Bear Market…

… And Right Back to a Bull!

We can be smart about staying in the market by focusing on “pullback-proof” names.

Step 7: Prepare for Pullbacks

Where’s the market going from here? Well, if you own pullback-proof dividend payers, you probably don’t care.

My readers are often asking for safe income ideas. For stocks that pay dividends and never drop in price. It’s a very difficult task, but not quite impossible.

For most long-term investors who want big dividends–I’m talking 6%, 7% and even 8%+ current yields–I recommend holding safe dividend-paying bonds and funds through any market turbulence.

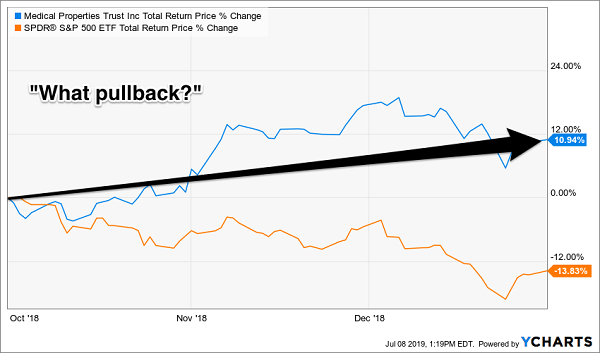

Big dividends are the rubber duckies of the investing world. Wall Street hysteria may push their prices underwater for days or weeks at a time, but as the months and years pass these stocks bounce back to the surface. Let’s revisit our dividend machine from steps two and five. Did its investors even realize we had a market collapse in the fourth quarter of 2018? No.

Q4 2018’s Dividend Rubber Duckie

There’s nothing quite like a pullback-proof dividend machine! And if it’s “2008-proof” then even better. After all, we’re 11 years older now and few of us can afford a 50% drawdown.

If you need big income without the drawdowns, I do love the short and long-term prospects for five 2008-proof dividend payers yielding an average of 7.5%. If you’re worried about a repeat of 2008 (and again let’s be honest, who isn’t), here are five solid payouts you can purchase today without worrying about an overdue pullback (or worse, an all-out crash).

Introducing the “2008-Proof” Income Portfolio Paying 7.5%

The “cash or bear market” no-win quandary inspired me to put together my 5-stock “2008-Proof” portfolio, which I’m going to GIVE you today.

These 5 income wonders deliver 2 things most “blue-chip pretenders” don’t, such as:

- Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

- A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure a safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a SAFE 8.5%.

Think about that for a second: buy this incredible stock now and every single year, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is. These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “2008-proof” plays might have wondered what all the fuss was about!

These five “2008-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out (every year), with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.

Recent Comments