Mainstream investors are stuck with cheesy dividend ETFs paying measly sub-3% yields. But we contrarians can grab ourselves a lot more dividend cash with a “switch” in our portfolio that more than doubles our yield, to 6.6%!

We’ll be fully diversified, too, with bonds, S&P 500 stocks and real estate populating our holdings—703 investments in all. And they’re all hand-picked by expert money managers who evaluate credit and interest rate risk for us.

Plus, this “6.6% retirement solution” has more price upside! The 3 battleship funds we’ll get into below are geared to grind higher as they pay their dividends, no matter what the market does.

The Inside Story on Our Instant “Dividend Double”

Think about the typical income investor’s situation for a second. They likely hold some mix of bonds, stocks and real estate—the “Big 3” drivers of most people’s wealth.

The trouble? All three are lousy income generators!

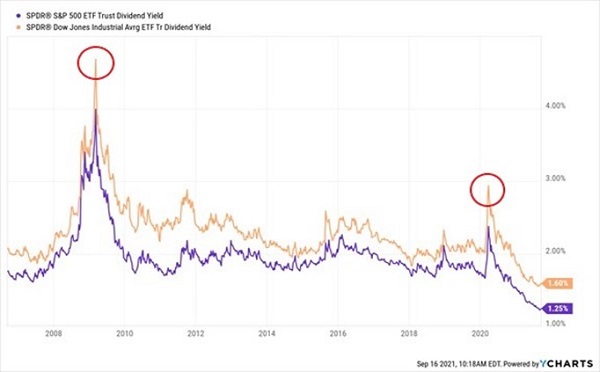

Let’s start with stocks: right now, the S&P 500 benchmark SPDR S&P 500 ETF Trust (SPY) yields 1.25%. So even with a million bucks invested, you’re only getting $12,500 in dividends. Poverty-level income! The Dow Jones Industrial Average isn’t much better, yielding 1.6%.

Granted, stock dividends are near 20-year lows, as the bounce from the March 2020 mess crushed yields (as yields and prices move in opposite directions). But let’s be honest: the only times you’ve been able to grab a decent yield from the S&P 500 or the Dow is if you had the nerve to buy when the market was a tire fire:

Stock ETFs Only Pay When They’re Getting Creamed

But that doesn’t mean we should give up on blue chips! Because the truth is, not much else can top them for growth. We just want more of our return in dividends.

Which leads us to the three “dividend swaps” that’ll give us to that 6.6% payout I mentioned earlier. To show you how much more cash these three funds—closed-end funds (CEFs), to be specific—give us, we’re going to mold them into a $750K portfolio that will let us retire on dividends alone.

That’s much less than the million bucks most advisors say we need. And in fact, thanks to these big yields, many folks may be able to retire on a lot less.

“Dividend Swap” No. 1: “X” Marks the Spot for 6.4% Cash Payouts

Our first stop is a CEF called the Nuveen Dow 30 Dynamic Overwrite Fund (DIAX)—just DIA with an “X” on the end.

DIAX holds the stocks in the Dow Jones Industrial Average, such as Microsoft (MSFT), Home Depot (HD) and McDonald’s (MCD), but with a twist: the fund sells call options—or the right for investors to buy its holdings at a future date at a set price. In return, DIAX gets cash premiums, which fuel its 6.4% dividend.

That’s a huge difference over DIA. Let’s say we’re splitting our $750K portfolio three ways between stocks, real estate and bonds. In that case, our $250K in stocks gets us $16,000 a year in dividends with DIAX, compared to $4,000 with DIA.

That’s an extra $12,000 just for adding an “X” to DIA’s ticker!

Now you do lose a bit of upside here, due to the fact that some of DIAX’s holdings will be sold and “called away” as they rise. But if we’re headed into retirement (or are in retirement) we’ll gladly take that deal in return for the massive dividend!

Plus we should see some extra upside as DIAX’s 4% discount to net asset value (NAV, or the value of the stocks in its portfolio) inevitably disappears.

“Dividend Swap” No. 2: The Bond God Rules All (and Pays Us 7.4% in Cash)

Now that we’ve padded our nest egg’s dividend income by $12,000, let’s boost it even further on the bond side as we invest our next $250K.

These days, holding high-yield corporate bonds makes a lot of sense. Corporates yield much more than 10-year Treasuries, with the SPDR Bloomberg Barclays High-Yield Bond ETF (JNK) paying 4.4% today, versus 1.3% for the 10-year.

We can do better still with our next CEF, the DoubleLine Income Solutions Fund (DSL), payer of a 7.4% dividend that drops into our account monthly.

DSL is managed by the “bond god,” Jeffrey Gundlach. He’s called that because his consistent outperformance grabbed the bond crown from former PIMCO manager Bill Gross many years ago.

Gundlach and his team scour the world for the best bond deals. No wonder three of their top five holdings are overseas offerings that we mere mortals can’t access. Oh—and they have coupons above 7%!

That access, by the way, is why we want an actively managed fund when we buy corporates. Because having a pro like Gundlach pick our bonds means we’re almost certain to beat JNK over just about any timeframe.

That’s certainly been the case since we added DSL to the portfolio of my Contrarian Income Report service in April 2016. Since then, it’s handed us a tidy 75% return in gains and dividends, compared to just 44% for JNK. And that return is net of fees!

Sure, we do have to pay for Gundlach’s expertise—DoubleLine’s fee is 2.28% of assets (including interest on the reasonable amount of leverage DSL employs—Gundlach borrows against 28% of the portfolio).

That does sound high. But it doesn’t really matter to us because the return I just mentioned is net of fees, as are all the returns I give you. I don’t know about you, but I’m fine with paying a bit more in fees if I’m all but guaranteed to outperform the benchmark!

And the fee story gets better: DSL trades at a 3.6% discount to NAV, much more than DSL’s fees, so we’re essentially getting Gundlach’s talents for free!

If you’re keeping score, we’re now two-thirds of the way through our CEF-powered $750K portfolio (with $500K invested so far) and we’re already collecting $34,500 in income, versus $15,000 for the ETF version. So let’s move on to our final pick.

“Dividend Swap” No. 3: Triple Your Real Estate Income in 1 Buy

When it comes to real estate investing, most people think of rental properties. Trouble is, your real returns are often a pittance once you account for your costs (not to mention the time you need to put in finding tenants, unplugging toilets and chasing down rent checks).

Wall Street, of course is happy to provide a solution in the form of the Vanguard Real Estate ETF (VNQ), a go-to for the sector that gives us broad diversification, with holdings like cell-tower owner American Tower (AMT), warehouse REIT Prologis (PLD) and data-center owner Digital Realty Trust (DLR).

Trouble is, VNQ yields just 2.2%, which is sad when you consider that REITs are pass-through entities: they skim enough off the rent to keep the lights on and the buildings in order, then hand the rest to us as dividends.

That’s where a CEF like the Cohen & Steers Quality Income Realty Fund (RQI) stands apart. It holds many of the same REITs as VNQ, but with a key difference: dividends! As I write, RQI pays 6%, nearly triple the payout of VNQ—and, as with DSL, it hands us that cash monthly!

And talk about performance: Cohen & Steers is among the top management firms in the CEF game, and they’ve guided RQI to an 86% total return in the last five years, crushing VNQ in the process.

RQI Rules Real Estate

Even with that gain, we can pick up RQI at a discount today—it trades a little over 4% below NAV as I write this.

Final Score: CEFs Beat ETFs by $29,250

With RQI, our three CEFs give us that mammoth 6.6% income stream I mentioned off the top, or $49,500 in dividend income on our hypothetical $750K nest egg.

Compare that to our three ETFs holding bonds, Dow stocks and REITs, which pay just 2.7%, or $20,250 in dividends on our $750K. That $29,250 difference clearly shows why CEFs are a much better choice.

Urgent Note From the Publisher

Kevin Wallen here. I’m the publisher at Contrarian Outlook.

A couple days ago, Michael Foster, our in-house CEF guru, showed me the “dividends only” retirement portfolio he recently crafted.

If you’re on the hunt for huge dividend payouts and double-digit price gains (and who isn’t?!), you must check out what Michael has put together here.

It’s an incredibly diversified 5-CEF portfolio throwing off a hefty 6.5% dividend. And that’s just the average! The highest payer of the bunch yields an outsized 8%.

Those are the kinds of yields that could let you retire on dividends alone, and on a lot less than a million bucks (and probably much less than $750K, too!).

In fact, just $500K invested would give you $32,500 in dividends, easily enough for many folks to retire on. And then there are the discounts: these CEFs are so undervalued that Michael is calling for 20%+ price gains in the next 12 months.

Add it up and you could be looking at a 27% total return by this time next year!

But you need to hurry. As these are smaller funds, we can only allow a few investors in. Too many and we risk moving their prices, leaving those who come in a little bit late out in the cold. I think you’ll agree that this wouldn’t be fair.

Don’t miss out. Click here to get full details—names, tickers, dividend histories and everything you need to know—on these 5 high-yield CEFs.

Recent Comments