Wall Street is treating Venezuela like the next “black gold” rush.

Nah—I don’t think so. Let me explain why and share my favorite US-based energy dividends up to 8.4%.

Vanilla investors are piling into the majors like Exxon Mobil (XOM) and Chevron (CVX), betting that regime change is a “buy” signal for anyone with a drill bit near Venezuela’s flush Orinoco Belt. But we careful contrarians know better. Energy infrastructure does not simply bounce back overnight. (Fictional TV “landman” Tommy Norris is not taking a plane south to instantly fix production with a few phone calls, hard lines and Michelob Ultras!)

Venezuela’s oil system has been decaying for decades. It is beyond broken. Rusted shut, really.

Let’s stay home while the Wall Street suits board their private jets to chase their new shiny geopolitical gusher. The real money is here in America with the “toll bridges” that are actively pumping oil and moving gas today.

Traffic is what the US energy system does in 2026. We produce. We refine. We export. Oil is cheap but the pipes are still filling up. Whether prices move higher or lower, we want companies that will get paid.

Diamondback Energy (FANG), my “Permian Prince,” is the most efficient operator in the most prolific oil patch on the planet. This is a cash cow hiding in plain sight.

Diamondback doesn’t “explore” in the traditional sense; they basically manufacture oil. They’ve turned the Permian Basin into a factory floor, using “Simul-Frac” technology to frack multiple wells simultaneously like an assembly line. This relentless focus on efficiency has slashed their corporate breakeven to a rock-bottom $37 per barrel.

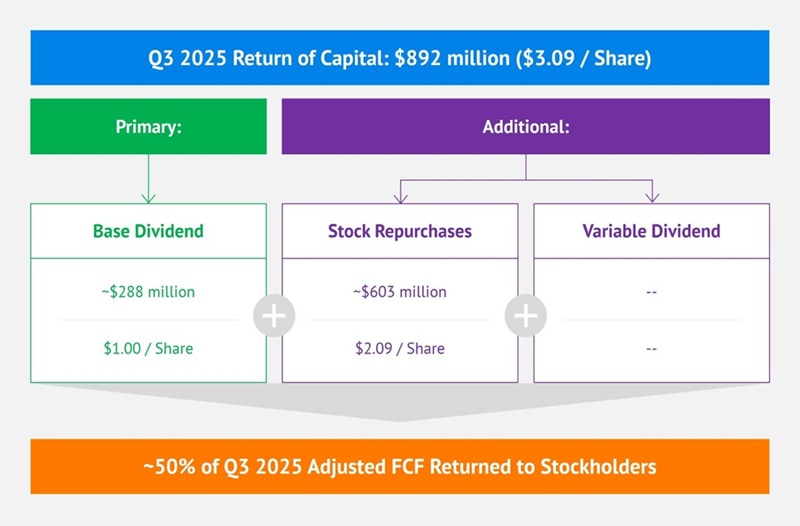

Let me repeat: Diamondback makes money down to $37. Oil can crash from today’s $57, OPEC can argue, the global economy can stumble, but Diamondback still throws off free cash flow. And they’ve committed to piping 50% of that cash back to us through a combination of stock repurchases plus a unique “base + variable” dividend model:

Diamondback’s Shareholder Reward Plan

And Diamondback just acquired Endeavor Energy, quietly making the combined company more efficient and profitable. Endeavor was the largest private explorer in the Permian, with top-tier Midland Basin acreage. By swallowing them, Diamondback “high-graded” its inventory.

Think of it like a puzzle board. Before the merger, Diamondback owned pieces of land next to Endeavor’s pieces. Now, they own the whole board. This allows them to drill longer laterals, extending their horizontal wells from 10,000 feet to 15,000 feet. Longer wells mean more oil for the same surface work.

Management expects $550 million in annual synergies. This cash drops straight to the bottom line—and then into our pockets via dividends and buybacks. Diamondback yields 2.7% but remember, this is only the “base dividend.” When the variable kicks in, this divvie has upside.

And the domestic energy dividends don’t stop at the wellhead. The “toll collector” that moves the gas quietly powering the US economy is Kinder Morgan (KMI). Kinder is a must-have in the AI age, a “pick-and-shovel” play that few investors think of. Every query to a chatbot taps into server racks that draw electricity on the scale of a small city. Which is why AI is evolving from a tech to a power story.

Kinder runs 79,000 miles of pipelines, moving an incredible 40% of the natural gas produced in the US. They get paid whether gas trades for $2 or $10. This energy toll collector threw off $5 billion in distributable cash flow last year, comfortably covering the 4.2% dividend.

And for those yelling: “More yield!” I hear you. Kayne Anderson Energy Infrastructure (KYN) owns the top names in energy logistics, including a large position in Kinder.

The appeal of KYN is that it yields 8.4% and trades at an 11% discount to its net asset value (NAV) It’s a way to buy Kinder & Co. for just 89 cents on the dollar.

Why is this dividend deal available in a supposedly efficient market? KYN is a closed-end fund (CEF), and CEFs trade crazy. Sometimes they fetch premiums to NAV, other times they demand a discount. It depends whether retail investors (the big players in CEFland) are salivating with greed or panicking.

When they freak out, KYN’s price drops, we grab the fund.

And by the way, KYN avoids the K-1 hassle that many of its individual holdings generate come tax time. The fund issues one neat 1099 form, just like a regular stock.

Bottom energy line? Let’s leave the “shiny objects” in Venezuela and instead focus on the cash cows in our own backyard. Go ahead and chase away, Wall Street. We’ll stay home and collect the tolls.

Diamondback and Kinder are current plays in our Hidden Yields portfolio. We beat the herd to the energy punch! If you didn’t invest alongside us, you’re missing out—please dial in your recession-resistant retirement here!

Recent Comments