The other day, we broke down how return of capital (ROC) can be both good and bad for investors in 8%+ yielding closed-end funds (CEFs). But in the case of high-quality CEFs, ROC is, contrary to what most people think, a good thing.

Today we’re going to look at some real-world examples to explain how, in fact, return of capital can make up a large share of a fund’s returns.

To do so, we’re going to go into five Nuveen funds, the Nuveen S&P 500 Buy-Write Income Fund (BXMX), Nuveen Dow 30 Dynamic Overwrite Fund (DIAX), Nuveen S&P 500 Dynamic Overwrite Fund (SPXX), Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX) and Nuveen Core Equity Alpha Fund (JCE).

Except for JCE, which I’ll get to in a moment, these are all covered-call funds that hold the index to which they correspond, then sell call options on part of that index, to essentially “translate” volatility into income for investors.

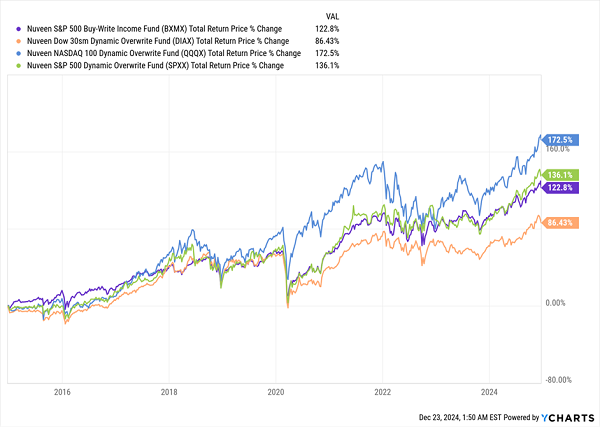

These four funds have strong records of doing this, with all but DIAX up over 100% in the last decade (DIAX, in orange below, is the laggard here, up 86.4%, largely because its index rises more slowly than those tracked by SPXX, BXMX and QQQX).

Solid Long-Term Track Records

These types of funds have a place in a diversified portfolio as a way to collect income, especially since they yield 7.2% on average. That’s obviously much more than the paltry 1.3% the average S&P 500 stock pays, as of this writing.

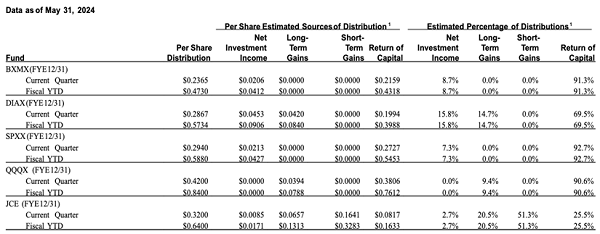

The funny thing about that big yield is that it tends to attract naysayers who will tell you that these funds are just charging fees and giving you back your capital, hence the vast majority of their returns are labeled as return of capital (see right-hand column below).

Source: SEC, Nuveen Investments

In BXMX’s case, 91.3% of the distribution is classed as ROC, while SPXX is a tad higher and QQQX is a tad lower, with DIAX far behind, at 69.5%. JCE appears to be the best of the bunch here, with 25.5% of distributions being ROC.

To be clear, these funds are not just giving you back your capital, as their healthy profits over the last decade prove. We discussed the technicalities of this in Thursday’s article. Now I want to focus on using ROC as an investment signal for these funds.

Already we can tell that ROC is not a useful signal, since DIAX has been the worst performer for a decade, but its ROC ratio is lower than those of BXMX, SPXX and QQQX.

However, this doesn’t mean we should go to the opposite extreme and say more ROC is the sign of a good fund: JCE’s much smaller portion of ROC coincides with it outperforming all of these covered-call funds in 2024, with a 24.6% return year to date, as of this writing.

The reason why JCE has outrun the rest isn’t down to the ROC amounts—it’s because, unlike the others, this is an actively managed fund, meaning management can buy and sell stocks as they see fit. So they can, for instance, lower the fund’s exposure to NVIDIA (NVDA) when that stock shoots up in price.

That’s unlike QQQX, which needs to buy more NVIDIA shares as the stock rises in price and thus becomes a bigger portion of the NASDAQ 100, which QQQX tracks. That’s also why JCE has done better than all of these covered-call funds combined over the last decade, returning 179% versus the covered-call funds’ average 103.6% return.

So we can see that one of the real keys to maximizing profits and income in CEFs isn’t obsessing over ROC, but instead focusing on indicators like portfolio quality, management and historical performance.

This is especially true when we compare funds of different types: JCE is not a covered-call fund, so the nature of its profits to investors is fundamentally different from those funds, since income from selling call options is recognized as capital gains.

What’s more, selling call options also means you’ll sometimes have stocks that are down in price be sold, or “called away,” resulting in the fund realizing losses that offset the capital gains it received from selling the call options.

This is also why covered-call funds tend to underperform over the long haul, especially if they are more passively managed, as our four covered-call funds are.

The key takeaway here is that if you’re shopping for a CEF, do yourself a favor and ignore the chatter about ROC, so much of which is misinformed and confused. In reality, ROC is more often than not an advantage, because it amounts to tax-free income for American shareholders.

And that means using funds that maximize ROC can be a great way to offset gains elsewhere or to boost income without boosting your tax burden.

That’s a great reason why, despite their slight underperformance, funds like QQQX and SPXX might actually give you a higher net profit than a fund that has a higher return on paper, like JCE.

These 4 CEFs Pay $9,800 on Every $100K (Their Holdings Will Surprise You)

With CEFs, the main attraction for most investors is the dividend, with these funds paying 8.7% on average. But few people realize we can use these funds to tap into a broad range of sectors too.

Better still, we can use CEFs to “squeeze” income out of sectors that don’t normally pay out a lot in dividends. That includes a category of stocks that might surprise you: AI stocks.

That’s right, through the 4 CEFs I’m pounding the table on now, you can reap big gains and income as artificial intelligence continues to embed itself in our lives. I’m talking about mammoth 9.8% payouts here.

And thanks to these funds’ deep discounts, we’re buying these AI kingpins—companies like NVIDIA (NVDA), Microsoft (MSFT) and Broadcom (AVGO), as well as smaller, fast-growing firms—at prices that haven’t been seen in months!

This is a terrific time to buy these 4 CEFs, and I can’t wait to give you all the details. Click here and I’ll spill the beans on these 4 bargain-priced, 9.8%-paying AI funds and give you a free Special Report revealing their names and tickers.

Recent Comments