Let’s talk about recession-resistant dividends because, if history is any guide, we are certainly “on the clock” for a slowdown if not already in one. Here at Contrarian Outlook we have been preparing for slower economic readings, and our recession divvies have already delivered.

Why the focus on slowdown safety? The Federal Reserve began hiking rates 2+ years ago. This is around the time something usually snaps in the financial markets. Sure enough, the Japanese yen of all things caused a VIX spike last seen in the 2008 and COVID crashes.

Our recession focus of late has been defense. Stocks like utilities, with higher yields but slower earnings growth. Today, we play offense—and look for 15%+ total returns per year regardless of what the market does.

The trick here is that we are focusing on companies with the ability to grow sales through a slowdown. Yes, these are fortress business models that generate steady cash flows. Stock prices that move independently of the yen! And tickers that don’t march to the weekly beat of economic data. It is the top line action that makes these stocks the most exciting.

Let’s start with UnitedHealth Group (UNH), most recently featured in my “Made for 2024” Dividend Plan. We buy the health insurer on dips—any and all dips!—because it has a captive audience.

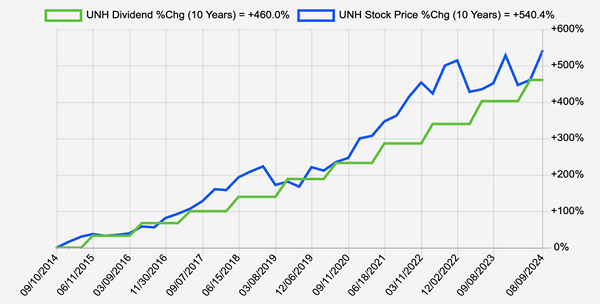

The company raises its dividend significantly every year. Over the past decade, UNH has hiked its payout by an amazing 460%.

Its stock price over the same 10-year period? Up 540%. The ticker followed the payout like a puppy dog—and then recently lunged ahead!

UNH’s “Dividend Magnet”

Source: Income Calendar

The ever-rising dividend is a result of ever-increasing cash flow. UNH’s perennial growth isn’t simply due to good fortune. Management had the foresight in 2011 to start its own technology driven Optum unit. Optum provides pharmacy benefits, runs clinics and supplies data analytics and other cutting-edge tech to streamline healthcare.

Revenues have nearly quadrupled since UNH launched Optum. This cash cow stays well fed in all economic environments. Perfect for a slowing economy.

UNH has rewarded us with 13% total returns since we last discussed it in January. The stock has rallied past my $550 “buy up to” price, which we track in my Hidden Yields portfolio. Be ready to add on dips.

Blue-chip biotech Amgen (AMGN) is another dividend grower uncorrelated to financial headlines with an underappreciated sales catalyst.

I’m old enough to remember when investors happily overpaid for biotech as they do for AI darlings now. Back in the early 2000s though, investors bought Amgen for hype rather than substance. They paid more than 20-times yearly sales for the right to own Amgen! These vanilla types just had to have this biotech.

Paying 20-times revenues for anything is generally a bad idea. Even if the company had perfect 100% profit margins (which is impossible) and was able to dish 100% of said profits as dividends (equally impossible), its maximum return would be about 5% per year.

Not great. Which is why Amgen shares went nowhere from 2000 to 2012. Yes, the company was growing and generating positive free cash flow the entire time. But the stock was dead money because, well, the price we pay for a stock matters.

Amgen is all grown up these days, with a profitable business and rising dividend and all. As a mature cash-flowing adult, the stock is written off from time to time! (Ah, life.) Most recently, Amgen shares pulled back nearly 19% after topping on February 1.

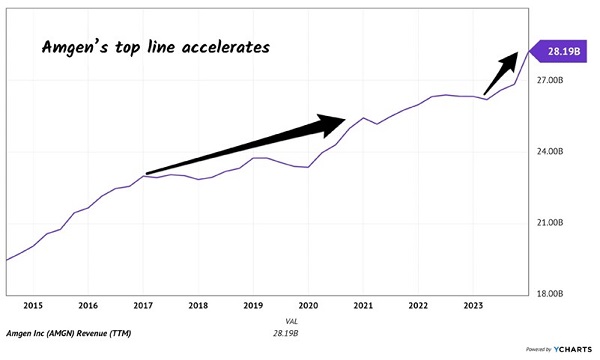

Many established firms like Amgen struggle to grow their sales. It’s the curse of large numbers. This is rarely a problem at Amgen, however. Whenever the drug-development pipeline is thin, management deploys capital to go and buy a promising drug candidate or even a full pipeline!

Recent acquisitions are paying off. Amgen’s top line is not only growing but accelerating. In recent years, Amgen has been aggressively shopping:

- In 2021, Amgen bought TeneoBio for $2.5 billion for access to its early-stage “cell engager” antibody, which has potential oncology applications.

- The following year, in 2022, Amgen acquired ChemoCentryx for $3.7 billion to boost its portfolio of treatments for autoimmune diseases.

- And in 2022, in the largest acquisition in its history, Amgen acquired Horizon Therapeutics for $27.8 billion. The prize was Horizon’s blockbuster drug Tepezza, a treatment for thyroid eye disease.

The theme here is rare diseases. There are more than 10,000 of them identified today, but only 5% have approved medicines. As an established biotech, Amgen has the blend of research and development and manufacturing know-how to bring these drugs to market.

Competition in rare diseases is low, and the addressable markets for these treatments add up. Since 2020, Amgen has boosted its rare disease product sales from $2.2 billion to $3.9 billion. This is the reason Amgen’s top line is accelerating:

Rare Disease Products Boost Sales

Does it matter to Amgen if the Federal Reserve cuts rates by 25 or 50 points in September? Of course not.

The only bummer with Amgen is that it has rallied so far, so fast (21% returns, good for 68% annualized!) since we added it to our Hidden Yields portfolio in April that the stock is now a Hold. I wouldn’t chase it here.

Instead, consider the healthcare star of 2021, which is finally cheap again. Remember these?

Top Landfill Item of 2021

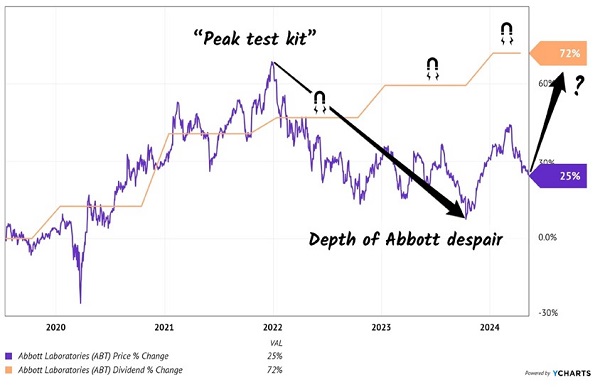

Don’t want to remember them? Me neither. Sorry to dredge up the past. I’m only doing it to point out the group of people that dearly miss these rapid test kits: Abbott Laboratories (ABT) shareholders.

Each rapid test use, whether required or voluntary, was another sale for Abbott. Whether the tests were paid for by Uncle Sam, an insurance company or my credit card at CVS, all sources represented top-line dollars for Abbott.

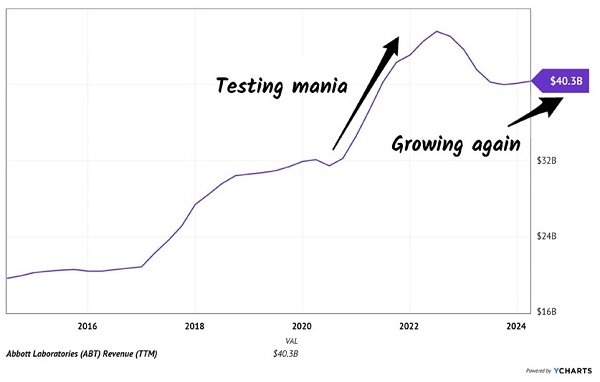

Sales spiked from $32 billion to $45.5 billion in just over two years. That is big growth off an already-big number! Of course, the “testing mania”—thankfully!—didn’t last forever. As it subsided, so did Abbott’s sales, until now:

“Testing Mania” Hockey-Sticked Abbott’s Top Line

Abbott has our attention because as demand for test kits waned, investors discarded this ticker along with their used Q-tips. So long, boogers—and Abbott.

To compound the bear move in Abbott shares, just as test kit sales were peaking, 2022 happened. Higher interest rates and quantitative tightening sent the stock market lower. Abbott dropped 36% peak to trough.

Yet, along the way, management continued to raise its dividend. Abbott’s core business was doing fine. Sure, test kit demand had peaked, but this was predictable. Onwards and upwards with the payout!

Abbott’s Dividend Magnet, Unphased by Test Kit Mania

Health and wellness trends and fads come and go. As they do, Abbott is there to take advantage of them!

Replacing Rapid Tests with a Shake

Case in point, the company recently launched a protein shake called PROTALITY. As people try to lose weight (via caloric restriction, taking medications or weight-loss surgery), sufficient nutrient intake is a challenge. PROTALITY is packed with protein and vitamins and minerals to support this.

Sure, there are plenty of protein and green powders in the world. But few of these providers have their hooks into distribution channels like Abbott. I’m not talking about sponsoring a health podcast here and there. PROTALITY is on the shelves at retailers like Walmart and CVS plus Amazon.

During my recovery from Achilles tendon surgery, I was told to eat my bodyweight in grams of protein. Which, for me, amounted to 200g of protein per day. I’ll tell you from experience, good luck getting that much protein down without a shake or two!

PROTALITY plus current products have Abbott’s top line humming again. The company’s organic revenue growth minus COVID test kits will be 8.5% to 10% for the year. Serious sales growth for a company this big!

The decline in test kit sales continues to blur the near-term outlook for Abbott, but it won’t fog up the front window much longer.

COVID test kits are becoming a smaller and smaller portion of Abbott’s top line. Sales are growing again, and they will accelerate further as test kits decline.

A 36% pullback in a “recession-resistant” stock like Abbott is what we contrarians live for.

And there are even better buys than Abbott here. A slowdown won’t slow these divvie growers! We’ll discuss in Friday’s edition of Hidden Yields.

But I just checked your subscription status and we don’t have you as an active subscriber to Hidden Yields. Don’t miss my new recession-resistant dividend pick, to be released this Friday! Claim your risk-free trial to Hidden Yields here.

Recent Comments