Here’s an idea that might sound just a little bit odd at first: You can actually get retirement-investing advice that’s too conservative.

That may not sound like a bad thing, right? After all, who doesn’t want to be extra sure they have enough to clock out?

The problem with this, however, is that being overly conservative has the very real consequence of keeping us in the workforce much longer than we need to be.

I bring this up because I was thinking of the “4% rule”—which points to 4% as the amount of your portfolio you can safely withdraw in retirement—the other day. Some people who decide to follow it may get the impression that they can’t retire soon, when in fact they absolutely can.

Let’s dive into this a bit further, starting with something I see as a much better alternative than the tired 4% plan.

Who Needs 4% Withdrawals When You Can Have 0% Withdrawals?

If you’ve been reading my articles for a while or are a member of my CEF Insider service, you won’t be surprised to hear that I see closed-end funds (CEFs), which yield around 8% on average, as a far more important part of retirement planning than the 4% rule.

Consider a CEF called the Liberty All-Star Growth Fund (ASG), which yields 8.7% as I write this. The fund’s dividend and growth history show that CEFs can generate the high, reliable income stream we need to not only retire earlier, but maybe do so without drawing down our portfolios at all.

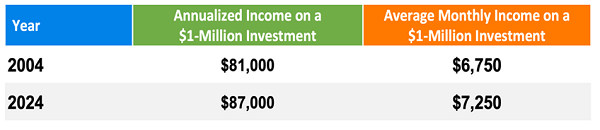

If you’d invested $1 million in ASG 20 years ago, not only would that investment still be intact today, but you’d have collected a significant income stream, too.

Twenty years ago, ASG traded at $4.75 a share, and it’s around $5.61 as I write this. While that gain might not seem huge, the real win here is in the dividends. Over this period, ASG paid out $7.71 in total dividends per share, translating into a robust average yearly yield of 8.1%.

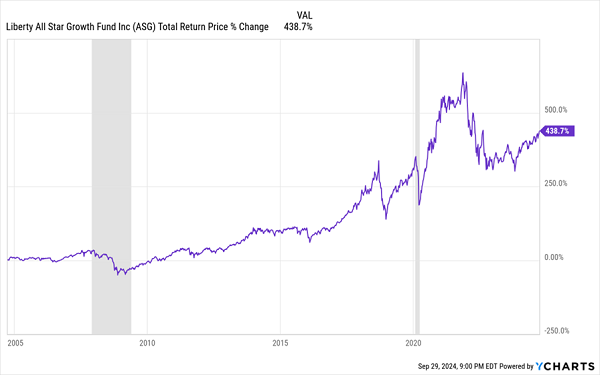

The end result is that, with dividends reinvested, ASG has posted an outsized 439% total return.

(This brings up a key thing we need to keep in mind with CEFs: By looking only at price returns, we get only part—and often a small part—of their performance history. For the full picture, we need to look at total returns, which include dividends).

439% Total Returns, Fueled By Big Dividends

Before we go further, we should note that ASG has a policy of paying about 8% of its net asset value (NAV, or the value of its underlying portfolio) as dividends every year, in quarterly installments. As a result, its payout does tend to fluctuate a bit.

That said, let’s continue, keeping our focus on ASG’s income stream, because its size more than makes up for this variability. If you’d invested $1 million in the fund two decades ago, you’d have received about $6,750, on average, monthly in dividends. And as stated, today that yield is even higher, at 8.7%.

Thanks to that higher yield, you’d now be collecting $7,250 per month in dividends, essentially giving yourself a pay raise just for holding on to a strong investment.

Rethinking the 4% Rule

Here’s where the 4% withdrawal rule comes back into the picture: If you can generate steady dividends from CEFs like ASG, you could take more than 4% from your portfolio each year, all while preserving your initial investment.

That, in turn, could let you achieve financial independence much sooner.

In fact, with an average yield of 8.1% as an asset class, CEFs like ASG generate payouts that, when averaged out on a monthly basis, could cover our living costs without needing to deplete our core capital at all.

And bear in mind that many CEFs pay us every month, too. Of the 22 funds in our CEF Insider portfolio, 18 pay monthly.

Then there’s the growth side of things: Many CEFs trade at discounts to NAV, which lets us buy their holdings for less than we’d pay if we bought these assets on the open market—and sets us up for price gains as those discounts disappear.

Higher Yields, Greater Freedom

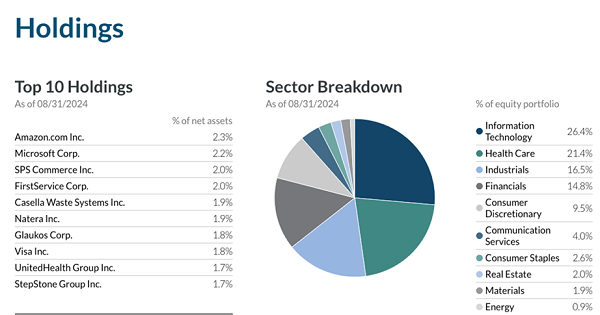

Let’s dig into ASG’s portfolio to see how this is all possible.

Source: Liberty All-Star Funds

Since ASG has invested in leading tech innovators, such as Amazon.com (AMZN) and Microsoft (MSFT), the fund’s portfolio is booking strong gains that management then turns into dividends for investors.

Add ASG’s diversification—health care is its second-largest sector, followed by industrials, financials and consumer discretionary—and you can see how the fund is as diversified as an S&P 500 index fund while yielding more than seven times more.

As a result, after 20 years, an investor’s upfront investment hasn’t only been maintained but has grown modestly, while the dividends have provided strong income.

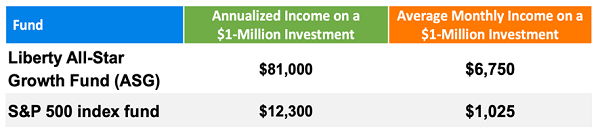

Compare that to someone following the 4% rule, withdrawing from a static portfolio of S&P 500 stocks. For them, $1 million yields a fraction of the income ASG does.

By adhering to conventional “wisdom,” investors are limiting themselves to a smaller income stream and a slower path to retirement.

Finding Financial Freedom With CEFs

ASG is a good example of how you can avoid delaying retirement because of flawed guidelines like the 4% rule. CEFs like ASG have proven their ability to deliver income and growth, and many pay strong dividends that are even bigger than ASG’s 8.7% payout. It just takes a bit of research and a willingness to look a little outside the everyday options to find them.

Forget Unstable Payouts: These 10.5%-Yielders Drop Dividends Every Month

ASG is one of my favorite CEFs—it’s always either in our portfolio or high on our watch list at CEF Insider. But I do recognize that some people don’t love the variable dividend payout. They want (and in some cases need) a regular, predictable dividend instead.

Which is why I’ve put together my 5-CEF “Monthly Dividend Portfolio,” which yields an outsized 10.5% today.

If you need (or indeed just want) a collection of investments that pays every month, this “mini-portfolio” is for you. Drop in, say, $200K and get a sweet $$1,750 a month. And of course, you can scale that payout higher or lower, depending on how much you want to invest.

Click here to learn more about this portfolio (plus the fast 20% price upside I expect from these stout monthly payers, too). I’ll also give you a free Special Report naming each and every one of these high-paying funds. Don’t miss out.

Recent Comments