Natural gas prices are ripping. And we’re going to play it through a “contrarians-choice” 5.9%-payer whose stock is headed in the other direction.

This is a perfect contrarian setup, and I don’t expect it to last.

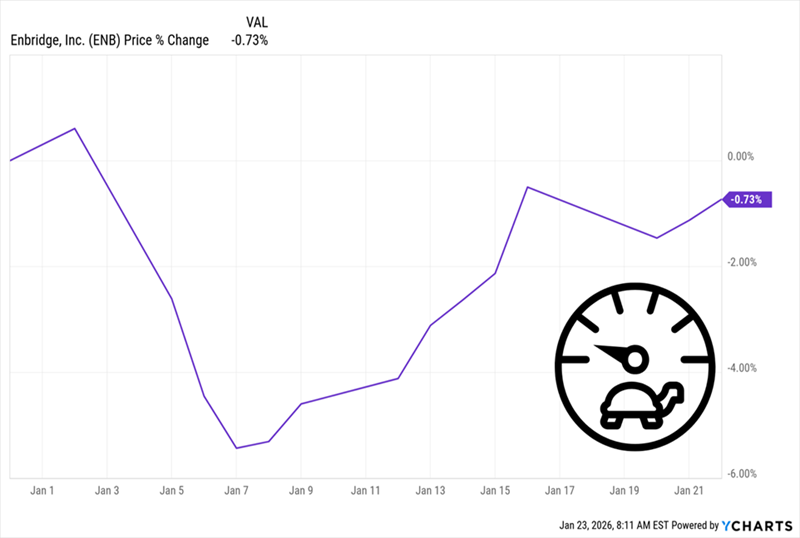

I’m talking about Enbridge (ENB), whose share price has lagged in the first few weeks of 2026, even as gas prices went to the moon:

Gas Soars—and Enbridge Gives Us an Opening

To be sure, this gas-price spike is driven by the arrival of a “generational” winter storm here in the US. But it’s a sign of things to come, as gas demand is not going anywhere.

And Enbridge, our Canadian “natty” king, is here for it.

This low-key pipeline operator is a holding in my Contrarian Income Report service; it’s delivered a sweet 44% total return for us since we bought it in March 2023. And I’m now recommending CIR members buy more.

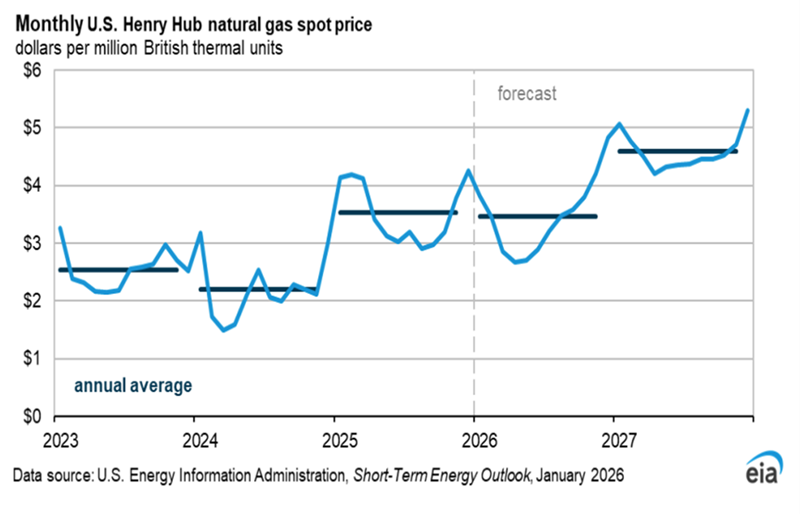

Here’s why: According to the Energy Information Administration (EIA), natural gas prices will remain more or less flat this year after pulling back a bit from last year. But here’s the twist: they’re forecast to jump 33% in 2027 as demand pops, thanks to more LNG exports and higher power use here in the US.

If you’re thinking data centers have a lot to do with that, you’re right. They’re a big reason for that spike in power use, whether the resulting power bills are paid by the likes of Microsoft (MSFT), Alphabet (GOOGL) or consumers themselves.

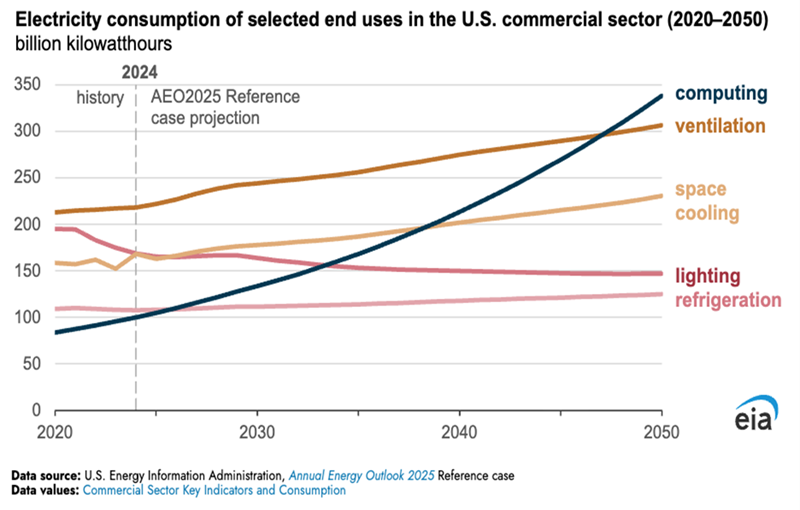

Take a look at this chart, also from the EIA:

That’s right: By the mid-2040s, the amount of power businesses use for computing could eclipse what they use for, well, pretty well everything else!

This is great news for a company that sits in the middle of North American energy flow. Enbridge’s pipeline network moves 20% of the natural gas consumed in the US and 30% of North American crude-oil production (more on that in a moment).

In other words, it’s a classic “tollbooth” play, collecting “fees” for every barrel of oil and cubic foot of gas that rolls through its pipes. So while it’s not benefiting from higher gas prices directly, it is cashing in on the higher demand they represent.

And while renewables are growing, let’s be honest: The sun doesn’t always shine and the wind doesn’t always blow, so natural gas will be needed for a long time to come. But management has hedged its bets either way, nicely covering the renewable angle, too.

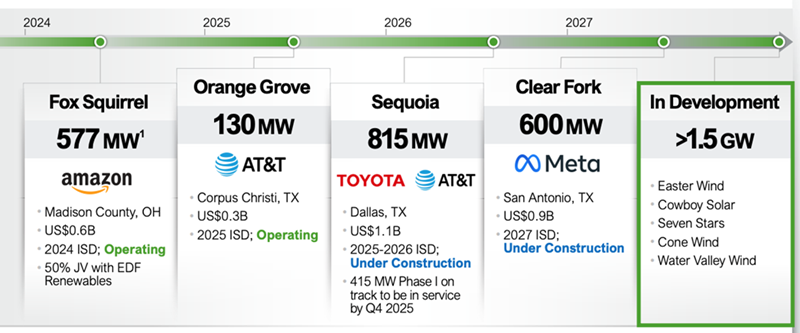

As of now, Enbridge has a little over seven gigawatts (total, before accounting for shares of this power going to joint-venture partners) of renewable power projects up and running or under construction around the world. Those include plenty here in the US supplying major tech and communications firms like Amazon.com (AMZN), Meta Platforms (META) and AT&T (T).

Source: Enbridge Q3 2025 earnings presentation

This is a smart move because while renewables are out of favor in the US now, energy companies think in terms of decades, not years. Adding to its renewable portfolio puts Enbridge in a good spot no matter which way energy policy goes in the future.

Now let’s talk oil, because it’s another reason why we’ve got a nice opportunity on this 5.9%-payer now.

A Contrarian Play on Venezuelan Oil

Recently, Enbridge has been focusing on expanding its Mainline system, which ships crude from the Canadian oil sands to the US for refining.

The first phase will boost Mainline’s capacity by 150,000 barrels a day starting in 2027. Phase 2 will add another 250,000 barrels by 2030.

Now you might have heard that Venezuela produces a similar type of heavy crude as Canada. So what if this oil displaces our northern neighbor’s crude—and weakens the traffic on Mainline?

Forget about it.

Despite Wall Street’s initial euphoria, rushing as investors did into ExxonMobil (XOM) and Chevron (CVX) after the capture of Nicolas Maduro, the truth is Venezuela’s oil system has been decaying for decades. It is beyond broken. (Fictional TV “landman” Tommy Norris is not taking a plane south to instantly fix it with a few phone calls, hard lines and Michelob Ultras!)

It will be years—if ever—before Venezuelan crude will compete with Canadian “heavy.” Remember too that Canadian producers and US refiners have relationships going back to the 1950s. Refiners here will be loath to give those up for uncertain Venezuelan supply.

Despite this, worries about Canadian crude almost certainly added to ENB’s fall in early January, as we saw in the first chart above. That signaled the start of our opportunity.

A Rising Dividend With an Exchange-Rate “Kicker”

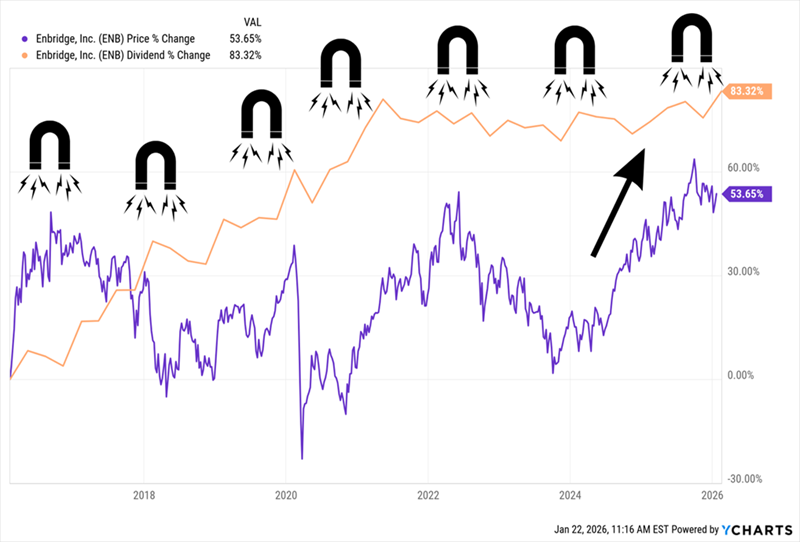

Let’s wrap up with the dividend: ENB recently announced its 31st consecutive payout increase. As you can see below, the share price (in purple) trails that payout (in orange), though it is starting to close the gap—the stock’s “Dividend Magnet” in action:

ENB’s Share Price Lags Its Dividend (But Has Momentum)

As I’ve written before, share prices ultimately track dividend growth. That’s because, when investors see a recent hike, they bid the stock up in response. The fact that ENB lags its payout—but is starting to close the gap—shows the stock is undervalued, but investors are starting to take note. That’s an ideal time to buy.

You probably also noticed that the dividend line above is not the serene “stair step” we’re used to seeing in our US dividend payers. That’s because Enbridge pays dividends in Canadian dollars. That’s a plus for us because, with the US dollar slipping, those payouts “translate” into more greenbacks when converted from Canadian “loonies” (a nickname for their currency, not their people).

And with interest rates likely headed lower in 2026 as a new “administration-friendly” chief takes over at the Fed, I expect the USD to fall further—giving us one more reason to grab shares of our Canadian “natty” king now.

This 11%-Paying Fund Is My Top Monthly Dividend Play for 2026

ENB is just the start. I’ve got another prime pick for you that, like ENB, profits as rates move lower. And it’s cheap today, too.

And that 11% headline yield is the real deal. For every $10K you invest, it pays $1,100 back in yearly dividends. That alone cuts your risk while bolstering your portfolio’s income stream.

This fund’s big monthly payout is not only steady—it’s risen since it was launched in 2021. Management has dropped two special dividends on investors, too.

The time to buy this under-the-radar income play is now, so you can start collecting its rich monthly dividend as soon as possible. Click here and I’ll tell you more about this 11%-paying pick and give you a free Special Report revealing its name and ticker.

Recent Comments