Need more dividend yield in 2025? Consider real estate investment trusts (REITs), which were literally mandated to be dividend-paying machines. Income is the point—by law.

Select REITs even yield 10% or more. What a payout! We’ll discuss seven of them—and their prospects for 2025—in a moment.

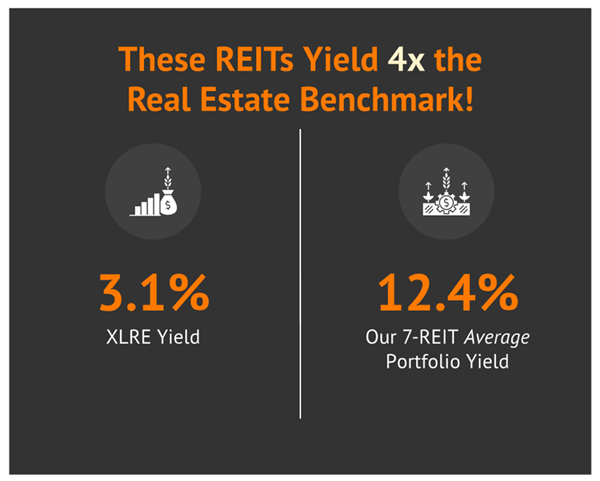

Now we can’t just blindly pick any ol’ a REIT. The real estate sector—using the Real Estate Select Sector SPDR (XLRE) as a proxy—only pays 3% right now.

But the average yield among this REIT 7-pack is 12.4%. That’s 4x what the sector pays!

That level of income would easily allow us to retire on dividends alone. But REITs aren’t all a slam dunk heading into 2025.

The Federal Reserve handed the real estate sector a boost in the form of three cuts to its benchmark rate in 2024. In fact, equity REITs have already been making the most of an improved cost of equity capital by issuing new shares to raise funds.

But the Fed also tightened up its expectations for further cuts, with the official “dot plot” signaling that the central bank expects to reduce its benchmark rate by only a half a percentage point in 2025—as early as September, they had expected a full point in rate cuts.

Let’s review this group of REITs yielding 10.4% to 15.3%, with a special focus on business and financial quality.

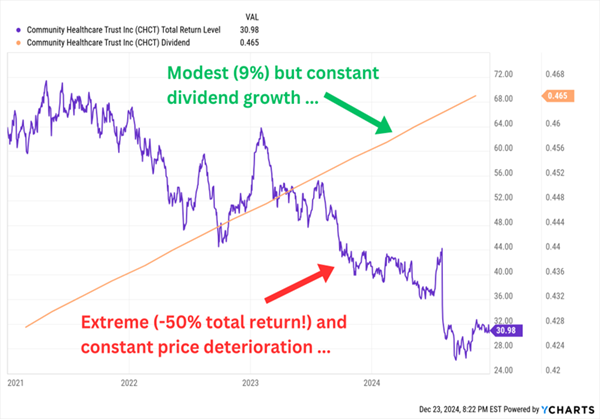

Community Healthcare Trust (CHCT, 10.4% yield) is an extremely diversified healthcare real estate owner. It boasts roughly 200 properties—including medical office buildings, urgent care centers, surgical centers, dialysis clinics, and many more types—across 35 states, leased out to 315 tenants.

And it’s the owner of one of the most curious charts I’ve ever seen:

Stock Prices, Dividend Amounts Aren’t Supposed to Move in Opposite Directions

CHCT has taken a page out of the Realty Income (O) playbook, delivering dividend increases each and every quarter for years. In fact, Community Healthcare is up to 37 quarters of uninterrupted dividend growth. But this run has been conservative and deliberate, with CHCT only raising by 0.25 cents quarterly for much of that streak.

However, the company’s funds from operations (FFO, a vital REIT earnings metric) are down below 2020 levels. A large part of the negativity in shares comes from CHCT hopping from one tenant flare-up to another. One of its tenants, GenesisCare, declared bankruptcy in 2023, resulting in a variety of outcomes for its leases, including some being assumed and assigned, and others remaining with the operating GenesisCare entity. As that was being resolved, another significant tenant began paying rent in late and/or partial amounts—though CHCT has put a consultancy team in place to resolve that issue.

Shares have stabilized of late, though. The Fed’s recent rate cuts should help the company’s cost of capital, though, and most earnings models show the company rebounding after a difficult 2024. But I’d be watchful. While CHCT has rarely struggled with dividend coverage (based on its non-GAAP “funds available for distribution”), that coverage could tighten, at least in the short-term.

Global Medical REIT (GMRE, 10.8% yield) is another double-digit yielder in the healthcare real estate space. GMRE currently owns 187 off-campus medical office and post-acute, inpatient medical facilities, leased out to 275 tenants, with an occupancy rate just above 96%.

Earlier in 2024, I said that “GMRE likely bottomed out in late 2022 after one of its tenants, Pipeline Health System, entered Chapter 11 bankruptcy protection. Regardless, it has been a roller coaster to nowhere, still down by roughly a quarter of its value over the past three years after a lot of hills and valleys.” GMRE has had to deal with another bankruptcy—Steward Health Care—and has lost another 10% since then.

There are reasons for optimism. GMRE has been able to sign a 15-year triple-net lease for its large Beaumont, Texas property that was previously leased to Steward Health. The company also went on the offensive across 2024, including closing on a 15-property portfolio for $80.3 million and more recently announcing a five-property acquisition for $69.6 million that will close in 2025.

The dividend still warrants a close eye. Global Medical REIT pays out 21 cents per quarter, and is on pace to deliver 90 cents per share in adjusted funds from operation (AFFO). That’s a 93% payout ratio—rather tight unless GMRE starts growing again.

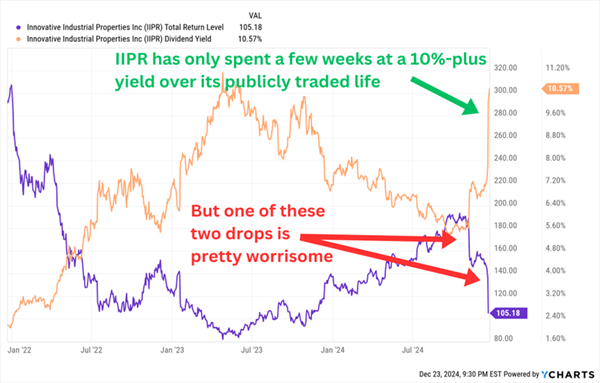

Innovative Industrial Properties (IIPR, 10.8% yield) isn’t a typical real estate investment trust. It doesn’t deal in residential properties or office buildings or warehouses. It deals in weed.

Innovative Industrial Properties provides capital for the regulated cannabis industry through a sale-leaseback program. IIPR buys freestanding industrial and retail properties (primarily marijuana growth facilities), then leases them right back, providing cannabis operators with much-needed influxes of cash that they can use to expand their operations. At the moment, it owns 108 properties representing nearly 9 million square feet across 19 states, leased out to 30 tenants.

IIPR was once the REIT industry’s growth darling, delivering nearly 900% in total returns between 2018 and its 2021 peak before cratering, losing 70% of its value since then. That includes a similarly hot-and-cold 2024, with shares up as much as 40% before cratering to 20%-losses for the year-to-date.

A Rare Opportunity to Own IIPR at a 10%-Plus Yield. But There’s a Catch.

IIPR’s shares have fallen off in quick order across two events, one of them much more worrying than the other:

- In November, shares dropped after the company missed revenue and normalized funds from operations (FFO). The double-digit dip was even big enough to bring out the class-action suit firms. (For what it’s worth, shares also slipped a little more a few days later after Florida’s recreational-marijuana amendment was voted down.)

- Just a few days ago, Innovative Industrial Properties announced that PharmaCann, a tenant representing 11 properties and 17% of IIP’s total rental revenues across 2024’s first nine months, defaulted on its rent obligations for six of the 11 properties, which thanks to cross-default provisions, meant PharmaCann effectively defaulted on all of its leases.

On the one hand, IIPR now trades for less than 8 times its annualized FFO (based on 2024’s first nine months). On the other hand, this gut shot is emblematic of a marijuana industry that seemingly refuses to make money despite the actual marijuana trade exploding.

Let’s stand back and let the smoke clear.

Once upon a time, Brandywine Realty Trust (BDN, 11.1% yield) was an office-focused REIT, but it has since diversified into a hybrid REIT with a mix of properties, largely focused on greater Philadelphia and Austin, Texas. The projected net operating income of its current pipeline, for instance, is 42% office, 32% life science, and 26% residential.

Following a 2023 that saw Brandywine reduce its dividend by 21%, the REIT enjoyed a stable, uneventful and even outperforming 2024. While it’s facing some issues in Austin, its Philadelphia portfolio is thriving. Its two most exciting projects are Philadelphia’s Schuylkill Yards and Austin’s Uptown ATX, which could help drive long-term FFO growth. It also trades at a thin 6 times next year’s FFO estimates—not terribly surprising considering the recent dividend cut, though its dividend coverage has improved.

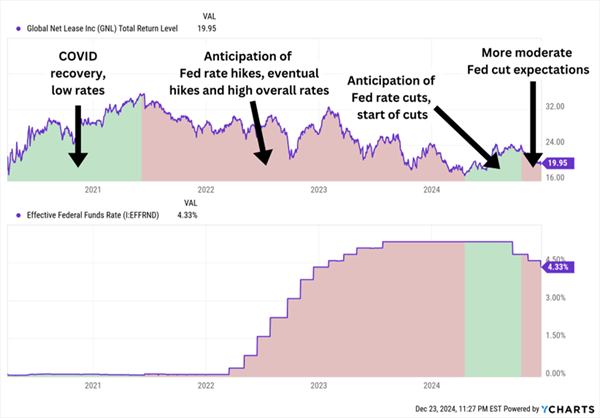

Global Net Lease (GNL, 15.3% yield) is a commercial REIT operator with 1,223 properties in 11 countries, leased out to 723 tenants in 89 industries. The U.S. accounts for roughly 80% of straight-line rents, though it also has a presence in Canada, as well as western European nations including the U.K., the Netherlands and Germany.

It’s also one of the highest-yielding equity REITs, at a whopping 15%-plus, despite what appears to be management’s best efforts to keep the dividend low. GNL has slashed its payout almost in half since 2020, across three cuts, including a 22% reduction in 2024.

Global Net Lease is currently selling off properties left and right in an attempt to bring down its leverage—it’s on pace for nearly $1 billion in dispositions in 2024, and Wall Street sees some $500 million to $600 million more in 2025. Net debt to adjusted EBITDA, at 8.4x at the start of 2024, is projected to come in at 7.8x-7.4x by the end of the year.

It’s a much healthier position, but it’s difficult to ignore the dividend track record. GNL’s high sensitivity to interest rates could also be a problem should the Fed clam up in 2025:

GNL Loves Low/Declining Rates

Double-digit yields are a relative rarity among equity REITs, but they’re commonplace among mortgage REITs (mREITs), which usually don’t own physical properties, but instead invest in “paper” real estate.

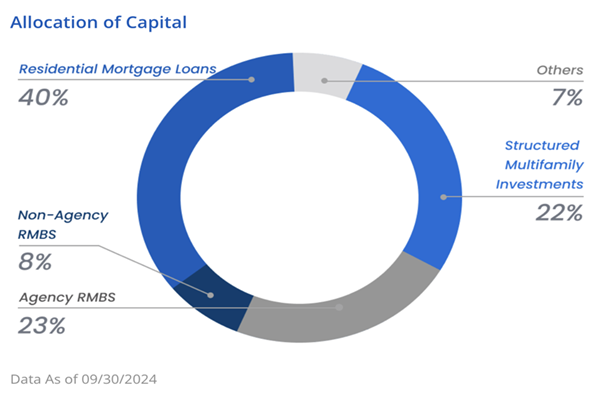

New York Mortgage Trust (NYMT, 13.7% yield), for instance, invests in a variety of mortgages and other securitized products, including residential mortgage loans, agency residential mortgage-backed securities (RMBSs), non-agency RMBSs, structured multifamily investments and more.

Source: New York Mortgage Trust

30-year mortgage rates have rocketed from less than 3% in mid-2021 to the high-6%s today. That has wreaked havoc on the mREIT’s residential securities. In turn, NYMT shares and the dividend have both been cleaved in half—the latter across a pair of cuts announced in 2023.

The company has almost completely unwound a multifamily joint venture that has weighed on book value, and shares trade at just 54% of adjusted book value. But the company’s undepreciated earnings (a non-GAAP financial metric NYMT uses) haven’t covered the dividend in at least three years. I’d be wary, though management seems unconcerned, saying they expect earnings will move closer to the dividend in time.

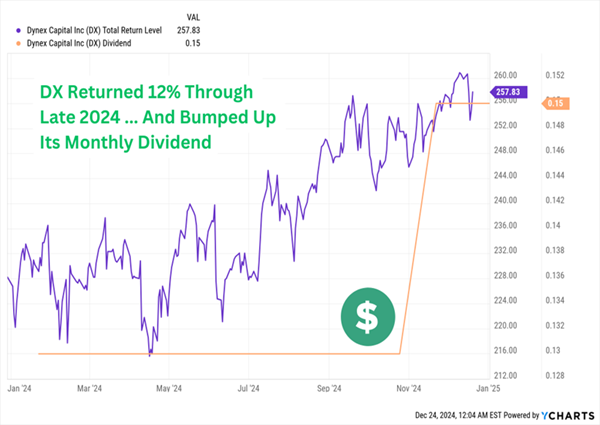

Dynex Capital (DX, 14.4% yield) is almost entirely invested in agency debt. The market’s longest-tenured mREIT is a specialist in agency MBSs—residential agency MBSs make up a whopping 97% of the portfolio, and commercial agency MBSs are another 2% or so. Non-agency CMBSs make up the remaining fraction.

Agency MBSs are considered “safer” than non-agency, but they also generally pay lower rates. As a result, agency MBS-focused REITs will utilize a lot more leverage to try to maximize performance and income. Dynex’s leverage decreased in the most recent quarter—to 7.6x, a still very robust rate.

I said in summer 2024 that “should the yield curve steepen (the gap between short- and long-term rates widen), Dynex is positioned well to benefit.” The yield curve obliged.

And Dynex Shareholders Benefited—In Two Ways

It’s an encouraging step in the right direction. The story of Dynex’s dividend has largely been one of collapse—DX paid 87 cents per share (on a reverse split-adjusted basis) back in 2012, but a series of cuts whittled it down to just 13 cents until the most recent hike.

The One 11% Dividend to Own in 2025

Several of these REITs have very real potential as we enter 2025.

But I’ll be honest with you: I have my horse blinders on. That’s because the Fed outlook for the year has me laser-focused on my One 11% Dividend to Own Now.

We’ve only seen a handful of Washington “clean sweeps” in American history, and each one was followed with some of the nation’s most sweeping policy changes.

Does that mean growth? Possibly.

Does that mean uncertainty? Certainly.

The ultimate safety net for times like these are secure dividends—cash in your pocket, right here, and right now, no matter whether your tickers are flashing green or red.

And an 11% dividend yield is an awful lot of protection.

My One 11% Dividend to Own Now is a rare machine capable of generating a simply ludicrous amount of cash. A 11% yield, in the most practical terms, is:

- Nearly $1,000 a month from a mere $100,000 investment

- $55,000 a year—a proper salary in many parts of the U.S.—from a mere $500,000 nest egg

- A wild $110,000 annually if you have a million bucks to put to work

Paid out for sitting around and doing nothing but waiting.

That kind of money doesn’t just buy you things. It buys you comfort. It buys you peace of mind. It buys you a break from restless nights, tossing and turning as you worry about whether the Fed is about to punish your portfolio again.

It could even buy you the ability to live off of dividends alone, without ever laying a finger on your nest egg.

But you don’t have much time. If you miss the deadline to get on the list now, in a few days, you could be leaving money on the table—and might not be able to lock in this 11% payout when the next distribution comes around.

Recent Comments