When the Wall Street cheerleaders actually dislike a stock—well, that sure commands our contrarian attention.

Today we’ll cover one of my favorite traditions, which is fading the opinions of analysts. You know, the guys who typically slap a Buy rating on everything they see?

It sounds counterintuitive, but we don’t want Buy ratings on our stocks. Give us Holds and Sells and general apathy. Or, even better, disgust.

When every analyst rates a stock a Buy, it feels “safe” to purchase. But really, it’s anything but. With nobody left to upgrade, there is nothing to do but wait for the dreaded downgrade.

Which can send a stock price lower. And trip up our devotion to retiring on dividends and keeping our principal intact.

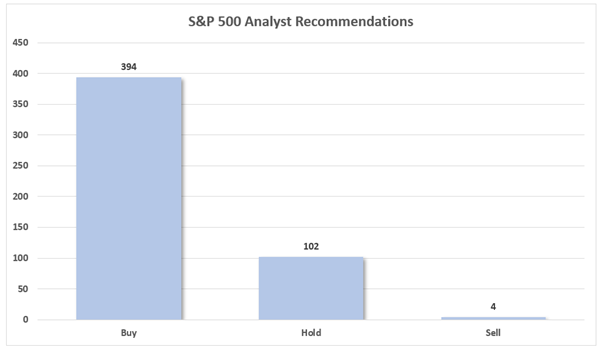

Bearish calls are better because upgrades are the future for the hated stocks. Unfortunately, these calls are also rare. Analysts know how they get their advantageous access, and it’s by having a generally rosy outlook whenever possible. It’s actually very unusual to find stocks that are consensus Sells.

How unusual? Less than 1% of the S&P 500 is rated Sell right now.

Source: S&P Global Market Intelligence

I’ve cast a wider net to see if we can catch any contrarian stocks. So let’s sift through a 7-pack of massive yields (all the way up to 12.4%) to see if we should be buying anything that Wall Street’s pros are selling right now.

BDCs

Business development companies (BDCs) provide funding to small businesses—a difficult way to earn a buck. But they routinely throw off enormous yields, so we always want to at least keep our eyes on this niche industry.

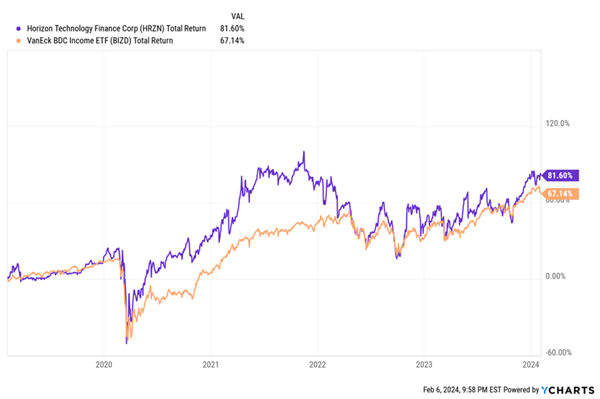

Horizon Technology Finance (HRZN, 10% yield), for instance, delivers double-digit income while offering venture capital-esque exposure. It holds 56 secured loans, as well as warrant and equity positions in 103 portfolio companies, with a focus on technology, healthcare tech, life science and sustainability.

The good news? HRZN has delivered industry-beating performance over the past few years—as well as an increase to its monthly dividend and several consecutive years of special payouts in that time.

A Higher Ceiling at Horizon

Horizon recently disclosed that debt investments in Nexii Building Solutions, representing 5% of debt investments at cost, were on non-accrual as of Dec. 31, 2023; total non-accruals are estimated to be around 10%. While hardly fatal, it’s problematic—especially for a BDC that’s priced for perfection. HRZN currently trades at 126% of net asset value (NAV), which is one of the industry’s highest valuations. That explains a bearish consensus of 1 Buy, 3 Holds, and 3 Sells—and it’s hard to disagree.

The pros are similarly down on Prospect Capital (PSEC, 12.4% yield), which primarily invests in senior secured debt of roughly 130 portfolio companies. It currently has just 1 Sell and 1 Hold, but the lack of analyst coverage on a $2 billion-plus firm is telling in and of itself—many analysts, when sufficiently bearish enough, simply drop coverage rather than keep a prolonged Sell call.

The bearishness has nothing to do with valuation—it’s in spite of it! PSEC is dirt-cheap at just 63% of NAV. But prolonged underperformance and operational stagnancy is why PSEC is considered “dirt-cheap” and not “dirt-value.”

MLPs

It’s hard to imagine Wall Street being too bearish on the master limited partnership (MLP) space—after all, though oil prices and traditional energy stocks have largely been lifeless, pipelines and other energy infrastructure have put up respectable returns over the past year or so.

USA Compression Partners LP (USAC, 8.5% yield), for example, has shot up 30% over the past 12 months. It’s a bit of an oddball in the space—it provides natural gas compression services, including designing, operating, servicing and repairing its compression units, and maintaining related support inventory and equipment.

Wall Street has 2 Holds and 2 Sells on USAC units—the MLP is heavily levered, and high levels of investment will impede its ability to de-lever in the short term.

USAC’s yield as attractive the leverage remains elevated and the company’s robust investments leaves minimal cash for deleveraging. Still, high demand and limited supply (in part thanks to supply-chain issues) should help the firm’s pricing power. For now, keep an occasional eye on this stock.

Cheniere Energy Partners LP (CQP, 8.4% yield) could be a more difficult ride over the next year-plus. Shares have grossly underperformed the industry, but CQP hasn’t exactly emerged as a value play. Instead, the pros are down on Cheniere’s MLP, at 7 Holds and 8 Sells.

The immediate first, second and third strikes against CQP are expectations of distribution reductions in the next year or so as the company builds cash for an expansion in the Sabine Pass.

Regular Stocks

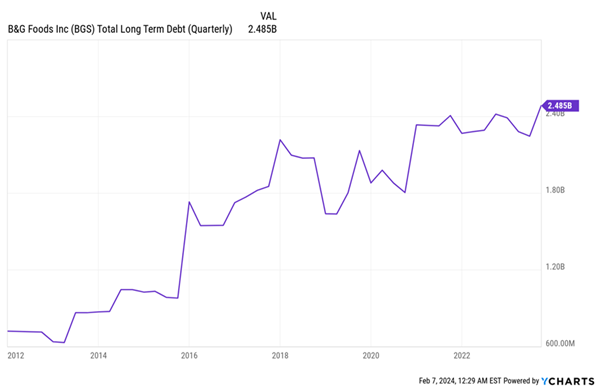

BGS Foods (BGS, 7.4% yield) is a consumer staples name you might know better as the parent of Crisco, Cream of Wheat, Green Giant and other well-known grocery brands. It’s a name I’ve explored before, and it’s one that analysts are only getting more bearish on. A few months ago, it had five Hold ratings and one Sell—fast forward to today, and the picture has worsened, to four Holds and three Sells.

Regular readers will remember BGS was once a Dividend Swing Trader play—and importantly, it was never anything more for us because of its weak fundamentals. We cut bait in 2020; a couple years later, B&G cut its dividend by 60% and hasn’t raised it since. Through the first three quarters of 2023, the company was operating in the red. In the meantime, total debt keeps creeping higher—at $2.5 billion, those IOUs are roughly 3x BGS’s market cap.

This Is One Chart You Don’t Want to See Head Higher

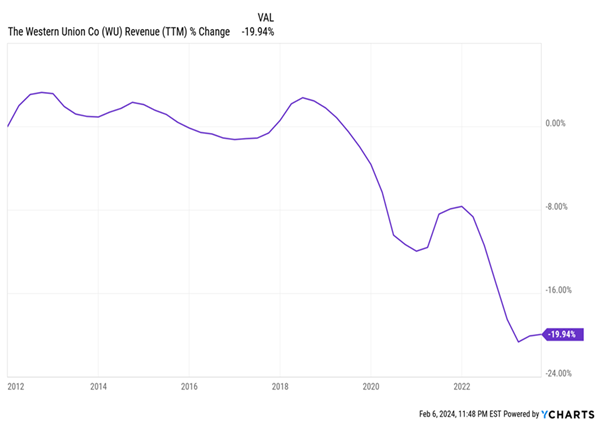

Western Union (WU, 7.9% yield) isn’t exactly a spring chicken, and a host of fintech companies—PayPal (PYPL), Wise, and more—clearly have it out for this once-proud payments giant’s lunch. Wall Street isn’t calling for WU’s head, but it’s not optimistic, either, with the stock currently garnering 2 Buys, 12 Holds and 6 Sells. And why not? Revenues have been on a sharp slide for several years.

Is the Future Coming for Western Union?

But I said nearly a year ago that “while Western Union is absolutely down, it’s not necessarily out.” And indeed, it has managed to at least temporarily stop its top-line bleeding and has put up a respectable 20% gain over the past 12 months. And its dividend, while stagnant, yields more than 7% and only makes up a little more than half of next year’s expected profits.

We’ll want to see whether these recent revenue gains are sticky—but its investments in the digital business and “Evolve 2025” strategy, in which it plans to offer services beyond money transfer, is at least showing green shoots.

Leggett & Platt (LEG, 7.9% yield) is an institution—a manufacturer that has done business for 140 years. LEG designs and makes bedding products, furniture, flooring, and high-performance specialized products that are used in aerospace, automobiles, construction and other industries. And it’s a nearly 8% yielder that has improved its payout each year for more than a half-century.

The analyst community isn’t overly bearish on LEG—just four analysts cover the stock, giving it 3 Holds and 1 Sell. But that could get worse in here in the coming months. Leggett recently announced a major restructuring plan in the Bedding division that will involve a more than 30% reduction in its facilities and an outright exiting some products. Management has told analysts that it remains committed to its dividend, but they’ve admitted that they could underearn it over the next year and possibly longer.

A Once-in-50-Year Retirement Storm Is Hitting Us NOW (Here’s Our Gameplan)

As much as I love a contrarian play, there’s a difference between going against the experts’ wisdom and going against common sense. And investing your hard-earned money in a company without the fundamentals to back its dividend just doesn’t make much sense.

And now, more than they have in a very long time, fundamentals matter.

That’s because we’re in the midst of a rare, once-in-every-50-years retirement storm that requires us to laser-focus on quality—or risk cracking our nest eggs wide open.

The last time we saw anything like this was the late 1970s! But if you were investing back then, you’ll also remember that right afterward, stocks took off in a raging bull market that led straight into the early 2000s.

Sure, history never repeats exactly, but it does rhyme, which is why I see better days ahead. I’ve explained my rationale in a Special Investor Bulletin you can read right here.

But what about right now? How do we protect our dividends until the skies clear?

We’re not powerless. Far from it.

Our goal right now is to safeguard our cash and set ourselves up for gains (and outsized dividends) on the other side of this mess.

When you read my Special Investor Bulletin, I’ll show you how to access three special reports that both lay out the high yielders best positioned to hand us sturdy dividends and upside as we roll through a potentially turbulent market—and reveal the 12 stocks you MUST sell now before these dividend pretenders yank the rug out from underneath you.

Recent Comments