Healthcare stocks are selling off with the turbulence in the Middle East.

But, why? The best plays here are geopolitical-proof. They print money regardless of what’s going on in the world.

So this is a good time to check in on healthcare. In a moment we’ll review five dividends between 6.0% and, get this, 14.1%!

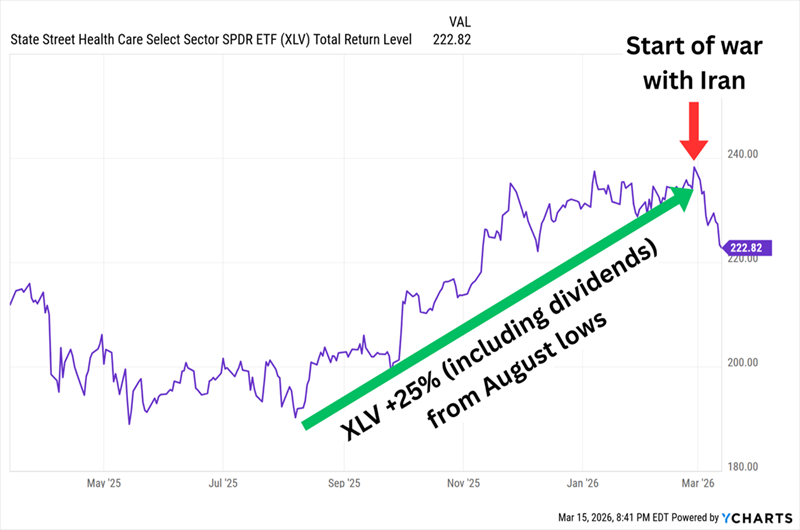

First, though, let’s unpack the reasons for the recent pullback. Back in August, I flagged how Medicaid cuts, health research funding, pharmaceutical tariffs and a cocktail of other headwinds had kept the sector pinned down for months. However these resilient companies have a habit of getting back up—and sure enough, healthcare went on a new tear, returning about 25% through late February.

Then Healthcare Got Caught Up in the Market’s Recent Turmoil

Here are five healthcare stocks handing us up to 9-times the sector average yield. Are these payouts worth purchasing? Let’s look under the hood and analyze the fundamentals.

Pfizer (PFE)

Dividend Yield: 6.5%

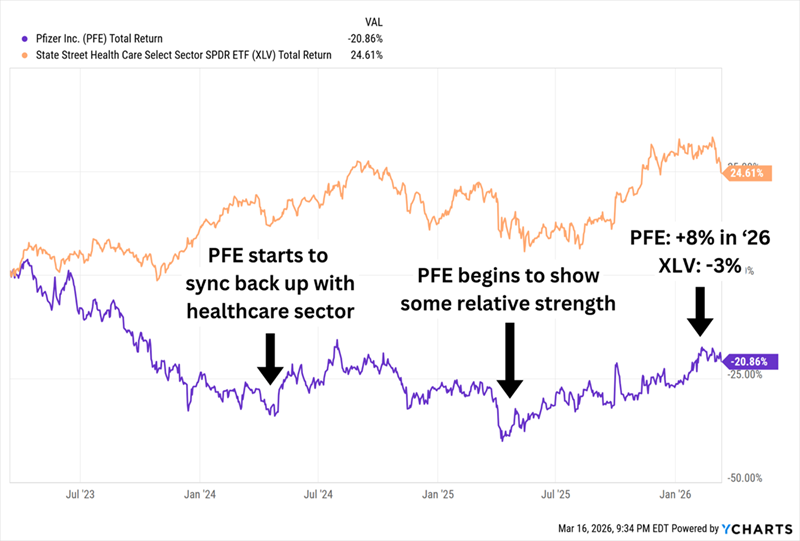

Pfizer (PFE) was for years one of healthcare’s most dependable blue chips, built on successful blockbuster brands like Lipitor, Viagra and Zoloft. But near the end of 2021, the bottom started to fall out of the stock. Today, shares are worth only half of what they were then.

The biggest risk staring Pfizer in the face is a common one in pharmaceuticals: the patent cliff. Eliquis, Ibrance, Xtandi, Prevnar 13 and other drugs that combined deliver about $17 billion of Pfizer’s annual revenue are scheduled to go over the patent cliff between now and 2030. For context, PFE’s revenue guidance for 2026 is $61 billion at the midpoint. The company has also been held back by changes to Medicare’s Part D prescription-drug coverage and declining COVID drug sales.

But Maybe, Just Maybe, Pfizer Is Turning Things Around

Pfizer is looking toward GLP-1 weight-loss drugs to help counterbalance its patent-cliff expirations. It has made several additions to its GLP-1 pipeline of late, including a $7 billion acquisition of Metsera, a collaboration with China’s YaoPharma, and a rights deal worth up to $495 million with China’s Sciwind Biosciences.

The stock technically has been in bargain territory for years, as I pointed out in both 2024 and 2025; it remains that way, at about 9 times 2026 earnings estimates and a yield that’s still north of 6%. What’s been missing are positive catalysts; its GLP-1 moves are a start.

Alexandria Real Estate Equities (ARE)

Dividend Yield: 6.0%

Pfizer is a rare 6%-plus yield out of pure-play healthcare stocks. Usually, for that level of income, we need to seek out related real estate investment trusts (REITs).

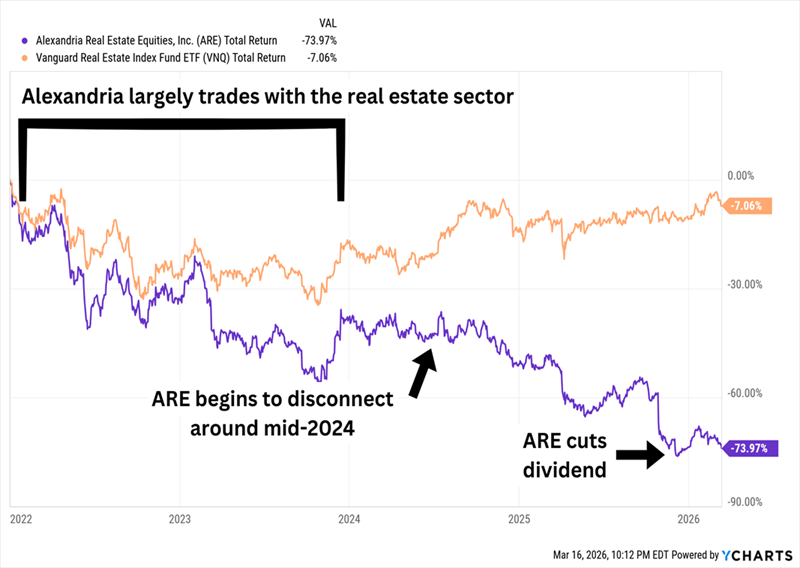

Alexandria Real Estate Equities (ARE), for instance, owns 340 properties representing some 35.9 million rentable square feet of operating properties, as well as another 3.5 million in Class A/A+ properties that are currently undergoing construction. Its properties are leased out to biotechnology, life science, biomedical, pharmaceutical, and other healthcare companies.

However, that means Alexandria is ultimately also an office REIT, and the stock has acted like it. Shares peaked in 2022 and have since crashed by nearly 75% amid a number of headwinds. Rising interest rates hit ARE along with the rest of the sector in 2022 and 2023; the stock was also weighed down by an oversupply in lab space, tightening NIH funding and FDA leadership turnover under the new administration, declining venture capital for startups, among other issues.

I warned in early 2023 that ARE was among several stocks that could cut their dividends. It took a couple of years, but Alexandria’s issues finally came to a head in December 2025, and the REIT announced it would slash its dividend by 45%.

Real Estate Found Its Footing in 2024; Alexandria Didn’t.

Alexandria is making up for at least some of the slack in life sciences demand by leasing out to technology companies. It has also been reducing capital expenditures, as well as its property count, which has shrunk from 391 at the end of 2024 to 340 today.

The company remains cheap, though at about 9 times AFFO estimates for 2026, it’s not the kind of swinging deal we’d hope for out of a company that’s been in perpetual decline. The dividend is much more realistic, at just 55% of AFFO projections—that’s good, but less than what we’d want out of what’s clearly still a fixer-upper.

Healthpeak Properties (DOC)

Dividend Yield: 7.0%

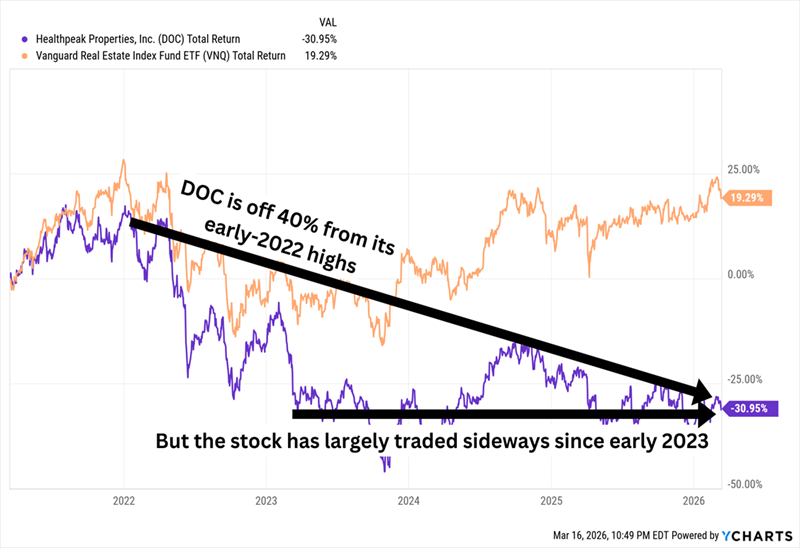

Healthpeak Properties (DOC), like Alexandria, is off significantly since 2022, but its trajectory looks somewhat different—and healthier.

We’d Like to See Better Than This, But It’s Not a Tailspin

But a new development will significantly alter this healthcare REIT.

Healthpeak, as of late February, owned 689 properties representing 50 million square feet and 10,422 units across outpatient medical facilities, laboratories and senior housing. Its tenants included biopharma firms, health systems, physician groups, medical device manufacturers and retirement housing companies, among others.

I use the past tense because the business is about to slim down.

The company recently announced the launch of its initial public offering (IPO) of Janus Living—a pure-play spinoff of its senior housing portfolio. Healthpeak isn’t completely detaching from the business—indeed, it will still own a “substantial” majority share after the IPO, and it will externally manage the company. But it does expose Healthpeak even further to the weak fundamentals of life science real estate. The primary hope there is Healthpeak’s belief that real estate fundamentals there “are at or near an inflection point,” and even then, “a full recovery will take time.”

We’re collecting a 7% yield—now paid monthly, a nice upgrade from last year—with coverage at just a hair above 70% of 2026’s AFFO estimates. And the stock trades at a decent 10 times those expectations. But we’ll want to see the dust settle on the Janus offering, and some genuine signs of life from the life sciences industry, before loading up.

BlackRock Health Sciences Trust (BME)

Distribution Rate: 7.9%

It should be no surprise to regular readers that the fattest sector yields can be found by tapping closed-end funds (CEFs).

BlackRock Health Sciences Trust (BME), for instance, gets us nearly 8% on a portfolio of Big Pharma, biotech and medical devices names.

That last industry has taken a shellacking over the past year, with holdings such as Intuitive Surgical (ISRG), Danaher (DHR) and Boston Scientific (BSX) ceding some of their influence over the portfolio to companies like AbbVie (ABBV) and increasingly AI-powered biotech play Gilead Sciences (GILD). Similar to the broader healthcare index, that exposure has put BME behind pure-play pharma and biotech funds.

But zoom out and this BlackRock fund has outperformed most noteworthy healthcare index funds since it launched more than two decades ago. And in true CEF fashion, we get to buy those holdings at a modest 4% discount to net asset value (NAV)—a hair wider than its long-term average.

The fund uses next to no leverage, nor does it sell covered calls or use other options strategies. Instead, its high yield is the product of disciplined capital gains distributions.

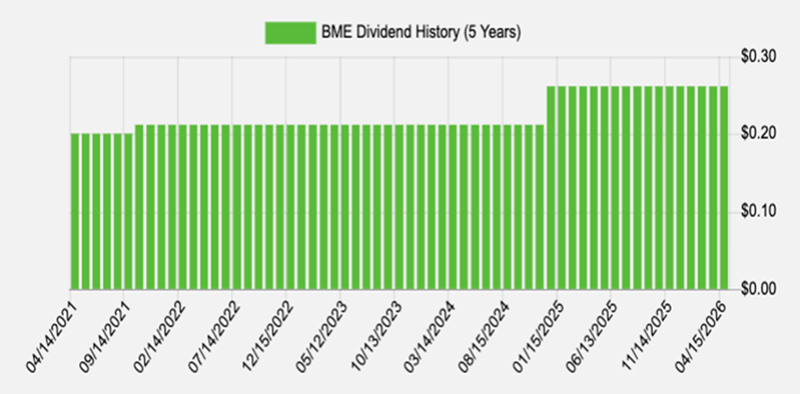

Importantly, though, BlackRock is happy to share the wealth as performance permits. The fund has actually raised its distribution twice over the past five years:

A Monthly Dividend Pointed in the Right Direction

Source: Income Calendar

abrdn Healthcare Investors (HQH)

Distribution Rate: 14.1%

BME doesn’t hold a candle to the sheer yield power of abrdn Healthcare Investors (HQH), which currently throws off north of 14% right now.

The name says “healthcare,” but the portfolio says “biotech.” A little less than 60% of assets are dedicated to biotechnology companies. Pharmaceuticals and healthcare equipment each enjoy double-digit weightings. The rest is splashed around life sciences, managed healthcare and other industries. Importantly, the fund can and does invest a little of its assets in privately held companies—a nice kicker that’s virtually impossible to find in ETFs and mutual funds.

HQH shares a few things in common with BlackRock’s fund. It trades at a nice discount (in fact, it’s even cheaper, at an 8% discount to NAV). And it doesn’t use leverage. Instead, it has a managed distribution policy—but unlike BME, it’s happy to use covered calls to achieve its sky-high rate.

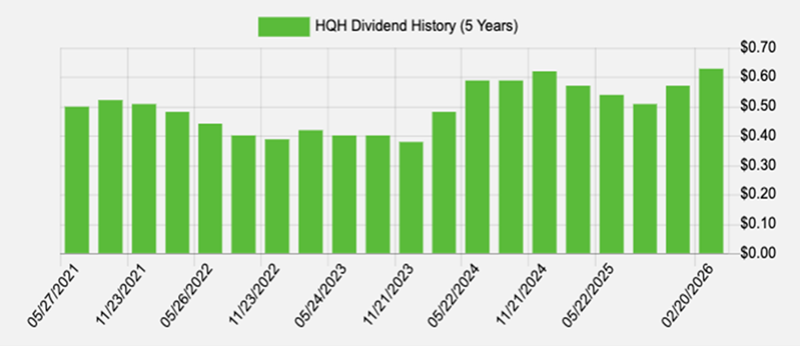

Unfortunately, That Distribution Isn’t as Consistent, And It’s Quarterly

Source: Income Calendar

The catch with covered calls is that they strip away upside potential—and biotechs are famous for their sudden, sharp launches.

My Favorite 11% Dividend Is a Cure for 2026’s Chaos

When HQH’s management sells calls against a biotech portfolio, they’re essentially investing with one hand tied behind their back, handing away gains to generate income.

If I’m taking a swing on a double-digit yield, I’d prefer to let a skilled manager do what he or she does best.

Right now, one of my favorite home-run dividends is a heavily diversified, brilliantly built bond portfolio that yields 11% but is also set up for stock-like gains.

This fund checks off just about every income box I can think of:

- It pays a whopping 11% in annual income!

- It has increased its dividend over time

- It has paid out multiple special dividends

- And it pays its dividends each and every month!

On top of that, Morningstar previously named this fund’s manager a Fixed Income Manager of the Year. He’s been inducted into the Fixed Income Analysts Society Hall of Fame, too.

That’s about as good a resume as we’ll find, and his fund will pay us $1,100 for every $10K we invest.

But the window is closing fast! Premiums on funds like these tend to rise as volatility ticks higher and as investors rotate out of growth stocks and into reliable sources of income like this. I don’t want you to miss your chance. Click here and I’ll introduce you to this incredible 11% payer and give you a free Special Report revealing its name and ticker.

Recent Comments