If you’re reading this, I assume you are already bullish on oil. Or at least intrigued by the upside possibility. And why not? There are three reasons crude may continue to crescendo.

First, we have the Middle East situation… ‘nuff said.

Second, it is increasingly looking like the Federal Reserve is cutting rates sans the usual impending recession. Rather than a hard or soft landing, it looks like we will see “no landing” at all in which the economy continues to grow.

We contrarians called this no-landing scenario five weeks ago. Since then, it has gained traction on Wall Street as employment numbers have stayed strong. Friday’s September jobs report was the latest example, showing stronger-than-expected growth. A bubbling economy keeps energy demand high.

Third, China recently started throwing everything including the kitchen sink at its own economic woes.

The People’s Bank of China (PBoC) announced a sweeping set of stimulus measures. The PBoC lowered interest rates (including mortgage rates) and announced “stock market support” plans to help companies buy back their own shares and allow investors to borrow against their portfolios. (Giddyup, China!)

Shares of Chinese firms spiked and copper popped, but energy prices remained relatively subdued until Iran lobbed ballistic missiles at Israel. The popular who’s who of energy names have predictably attracted the early money, but values remain.

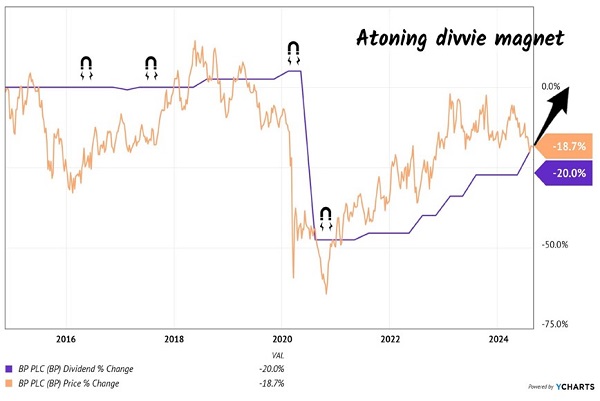

BP PLC (BP) is the biggest bargain in the bin, yielding 5.8% and trading for less than half of its yearly sales. We all know the British energy giant, which has been around more than a century. Like the old British Empire the sun never sets on BP’s 61-country operation.

BP produces crude oil and natural gas; deals in wind power and hydrogen and carbon capture; owns thousands of miles of pipelines; holds commercial operations such as convenience and retail fuel stations, Castrol lubricants and EV charging; trades oil, gas, and renewable and non-renewable power; and even sports a bioenergy business.

BP cut its dividend by 50% in 2020 and “dividend magnet” dragged the stock price down the same. Since then, the giant has revived. Sales doubled between 2020 and 2023 and today BP is solidly profitable again.

The “payout penance” continues for BP, with four hikes on the books since its infamous cut. This reminds us, once again, that CFOs are like carpenters—they measure twice and cut the dividend just once if they can help it. So far, so good. BP’s dividend sits 50% higher than after the cut. Still off its peak but trending positively as the producer atones for its 2020 divvie reduction:

Path From Dividend Doghouse

Yet for first-level investors income scars (and memories of them) are slow to heal. BP trades for only 8-times earnings and half of its trailing sales. Energy stocks have been hot, yet BP remains in the dividend doghouse. Contrast BP with Contrarian Income Report alum Exxon Mobil (XOM) which trades for 1.5-times sales and 15-times earnings!

This sad pup will soon be rescued by income-hungry investors. The company recently completed a $3.5 billion share repurchase program and initiated a new one. If as promised it’s completed by year end, the energy giant’s float shrinks another 4%!

Alerian MLP ETF (AMLP) has rallied since we called it a “no landing” favorite last week. Shares still pay a sweet 7.9% and look attractive here.

EOG Resources (EOG) meanwhile is a pure play on higher energy prices. It has the largest drilling permit portfolio in the entire industry.

The producer owns thousands of federal onshore drilling permits—more than any other company. EOG is also the number one permit holder in the flush Permian basin, which is known for its high-quality oil reserves.

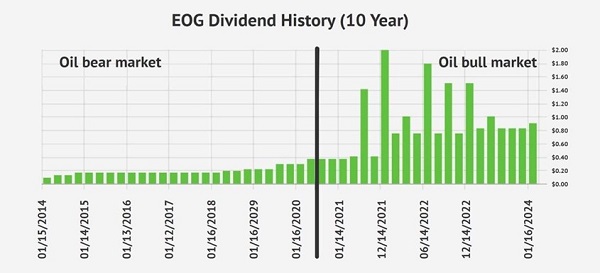

EOG has been good at pumping oil and dishing dividends to shareholders for the last ten years, which encompass a bear and bull cycle.

The first six years, from 2014 to 2020, was a brutal bear market in oil. Crude dropped from above $100 in 2014 to below zero in 2020. (If we weren’t there to see it, we wouldn’t believe it.) Yet, during this tough environment, EOG kept on paying and raising its dividend:

EOG Dividend History

Source: Income Calendar

The oil market began to flip from brutal to favorable in late 2020. Uncle Sam sent out a bunch of economic stimulus (“stimmy”) checks to juice the economy. Americans started traveling again and burning oil. Good times were back, baby.

And they went from good to great for EOG shareholders. Check out those post-2020 dividends! The big bars that you see, by the way, are special payouts, possible thanks to EOG’s permit portfolio and high prices. The company returns roughly 75% of its cash flow to investors via regular and special dividends every year.

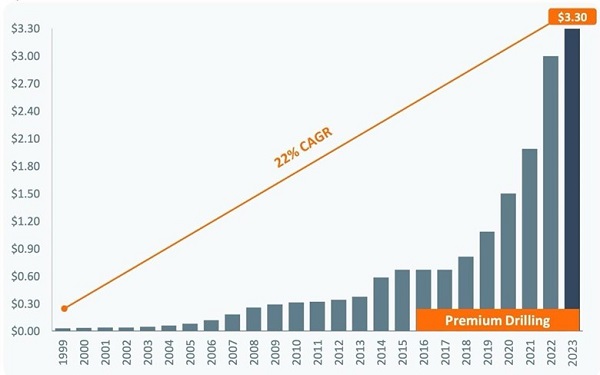

The “long view” of the permit king’s payout is equally impressive. Since inception, EOG has grown its dividend by 22% per year:

The Permit King’s 22% Per Year Payout Growth

And oh by the way, this chart is already dated–EOG hiked its 2024 dividend to $3.64. An increase of 10.3%.

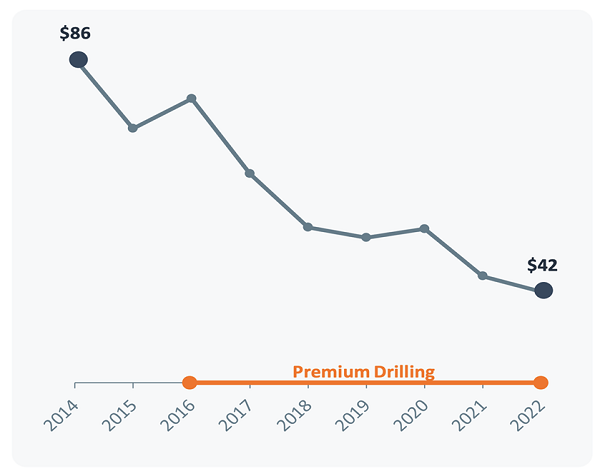

Since 2014, the oil price required by EOG to achieve 10% return on capital (ROC) has dropped from $86 per barrel to just $42 last year:

Oil Price EOG Needs for 10% ROC

Which means upside on oil is pure cash for EOG. The stock pays 2.7% while longs wait for it to moonshot.

Finally, the refiners are looking frisky here again. Few investors have the stomach for these volatile stocks. Most investors have no clue because they don’t understand refiners.

They confuse them with energy producers, who drill for oil and natural gas and then sell the raw products.

Refiners buy oil from producers and turn it into gasoline, diesel fuel, heating oil and other end products. Their dependency on others—from the cost of oil as the input to economic activity as the driver of demand—can create several Wall Street “boom and bust” cycles per year.

This makes them lovely stocks to trade! We can net a year’s worth of gains in one multi-month move. Phillips 66 (PSX) and Valero Energy (VLO) are my two favorites for a rally into the year’s end.

BP and AMLP are active holdings in our 9% No Withdrawal Retirement Portfolio. If you like these ideas and wouldn’t mind more dividend stocks and funds that yield a nifty 9% per year in dividends, read about my 9% No Withdrawal Retirement Portfolio here.

Recent Comments