Small cap stocks should benefit from the new administration. Today we’ll discuss four under $20 with yields between 7% and 15.1%.

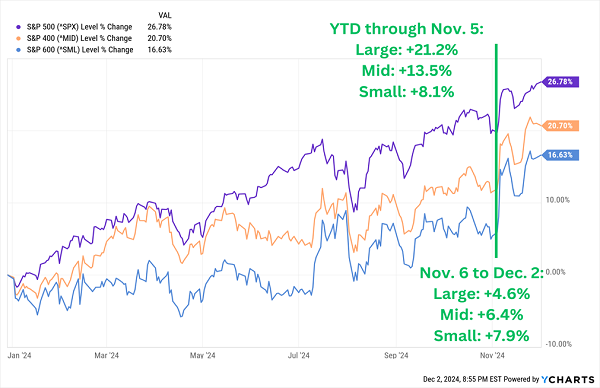

The Trump 2.0 Trade is rolling and small caps are soaring because they are expected to benefit from reduced regulations. Since November 6, the small have become mighty, outperforming their larger counterparts:

Election Flips the Small-Cap Script

Too much too soon? The counterpoint is inflation, which is likely to remain sticky. Which means interest rates will remain higher than Wall Street previously hoped. Higher rates are a headwind for smaller companies, which tend to be debt machines. (They lack the cash flow of the giants.)

Tariffs and immigration policies are more wild cards. Generally speaking they are also inflationary, but tariffs (if implemented) will benefit some companies and hurt others. It is going to be a stock picker’s market, especially in the small space.

Let’s talk about four of them. As a nice bonus all trade below $20, which means it is possible to buy a boatload of shares en route to collecting these big yields. Share counts of course don’t actually matter, but it is fun to play dividend kingpin once in a while.

Guess? (GES)

Dividend Yield: 7.0%

Guess (GES) designs, markets, distributes and licenses clothing and accessories—it’s known for its denim and apparel, but it also offers handbags, watches, footwear and other products. The company sells these products via 1,057 directly operated retail stores and another 541 partner stores across roughly 100 companies worldwide.

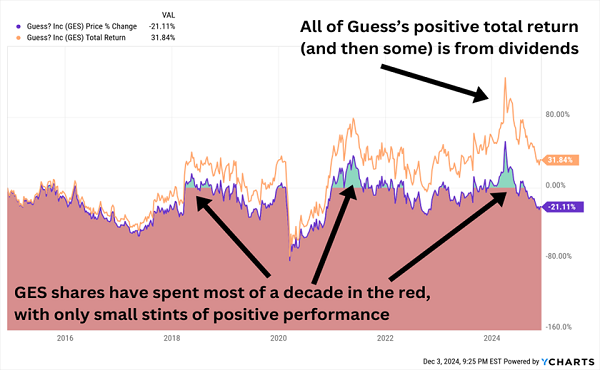

In March, Guess polished off its fiscal 2024 by announcing a massive $2.25-per-share special dividend, payable in April, that added a wild 13 points to its already generous regular payout, for a total annual yield of 20%.

That was management’s way of rewarding shareholders following 15% adjusted earnings growth and cash flow generation well ahead of internal estimates. On top of that, for the current fiscal year, Guess projected revenues up between 11.5% and 13.5%, and adjusted EPS of between $2.56 and $3.00 per share.

Alas, since then Guess has reduced expectations multiple times. So yes, GES is cheap, at less than 8 times earnings estimates, but we can chalk that up to an estimated 40% year-over-year drop in profits.

Guess has run headfirst into a gaggle of headwinds, including weak domestic retail results and a stronger U.S. dollar. A slightly better issue to have: Guess has also had to invest money for the launch of a new Guess Jeans brand, as well as for folding in its recent acquisition of the Rag & Bone fashion label.

GES shares have watched a 35% first-quarter gain evaporate across the rest of the year. Starts and stops like these are par for the course for Guess, which is one of the ultimate examples of fickle fashion stocks.

Without Its 7% Dividend, Guess Is a Long-Term Loser

MidCap Financial Investment Corp. (MFIC)

Dividend Yield: 10.8%

If we’re looking for small-cap stocks with massive yields, we’re going to run into a bunch of business development companies (BDCs). I call these companies “rich-guy loophole stocks” because they effectively let us invest in private equity for $10 to $20 per share.

Take MidCap Financial Investment Corp. (MFIC), for instance.

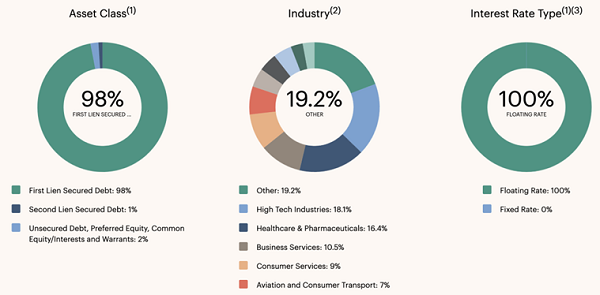

MidCap Financial Investment Corp. provides financing to middle-market companies with annual earnings before interest, taxes, depreciation and amortization (EBITDA) of less than $750 million. Its current portfolio stands at 250 companies across more than a dozen industries, with names including tax software firm Avalara, AI-powered DevOps platform provider Digital.AI and concrete and asphalt paving contractor Pave America. And MFIC works almost exclusively in floating-rate first lien secured debt.

Source: MidCap Financial Investment Corp. (As of Sept. 30, 2024)

MFIC’s loans are sourced by lender MidCap Financial, and both firms are managed by affiliates of Apollo Global Management (APO). One advantage this provides is the ability to access institutional-quality private credit at an extremely competitive fee structure

However, its relationship to Apollo goes deeper. This past year, MFIC merged with a pair of Apollo closed-end funds—Apollo Senior Floating Rate Fund Inc. (AFT) and Apollo Tactical Income Fund Inc. (AIF)—and alongside the transaction paid a small 20-cent-per-share special dividend. MFIC already yields a generous 10.8%; the special added another 1.4 points to a total of 12.2%.

MFIC is generally well-managed and has really come into its own over the past few years. It boasts a low percentage of non-accruals (briefly, debt overdue by 90 days or more that is no longer accruing interest), and it’s quickly moving out of lower-yielding assets it picked up from the merger. Also worth noting is a decent sale on shares at present, with MFIC trading at a 7% discount to net asset value (NAV).

BGS Foods (BGS)

Dividend Yield: 11.1%

Regular readers might remember BGS Foods (BGS), which was once a Dividend Swing Trader play. Importantly, it was never anything more than a swing trade for us because of its weak fundamentals. But because it’s a consumer staples name with a massive yield, I give it a once-over every few months to see if its situation has improved.

BGS Foods, by the way, owns plenty of grocery-store mainstays, including Crisco, Cream of Wheat, Ortega, Bear Creek—even a small line of Girl Scouts-branded seasoning blends.

Unfortunately, BGS is value-priced (at less than 10 times estimates) because the company’s fortunes continue to falter. The company recently cut its full-year views after a third-quarter earnings miss, and should finish 2024 with 30% and 6% declines in profits and revenues, respectively. The company divested the Green Giant shelf-stable product line in November 2023—a move that has weighed heavily on sales—though volumes flagged for other brands, too.

I’ve mentioned this before: BGS slashed its payout by 60% in 2022, a couple of years after we cut bait. But what’s troubling today is that the firm is expected to earn less this year (70 cents/share) and next (68 cents/share) than it’s projected to pay out in dividends (76 cents).

The company doesn’t have much financial flexibility, either.

BGS’s Long-Term Debt Is Nearly 4x Its Market Cap!

So, while BGS might be a staple, it hardly feels defensive.

Armour Residential (ARR)

Dividend Yield: 15.1%

We’ll find truly sky-high yields in mortgage real estate investment trusts (mREITs), where even a plain-vanilla industry ETFs yield north of 9%.

Armour Residential (ARR)—which primarily invests in mortgage-backed securities (MBSs) issued or guaranteed by U.S. government-sponsored entities such as Freddie Mac, Fannie Mae or Ginnie Mae—yields far more, at 15%!

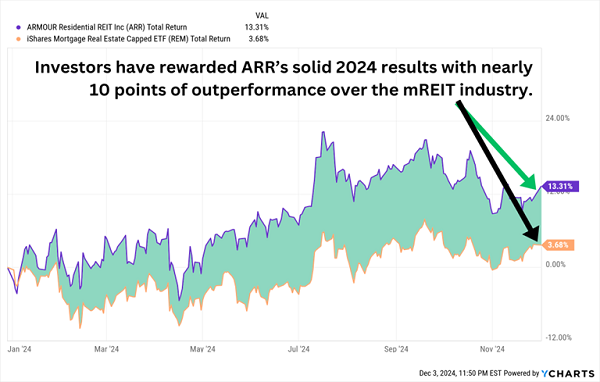

Right now, 96% of the portfolio is invested in 30-year fixed-rate pooled mortgages, and the remaining 4% is in agency commercial MBSs. So while declining interest rates are generally good news for ARR (like the rest of the industry), its reliance on agency business means ARR has very little credit risk.

Armour Is Taking Advantage of a Better Environment for mREITs

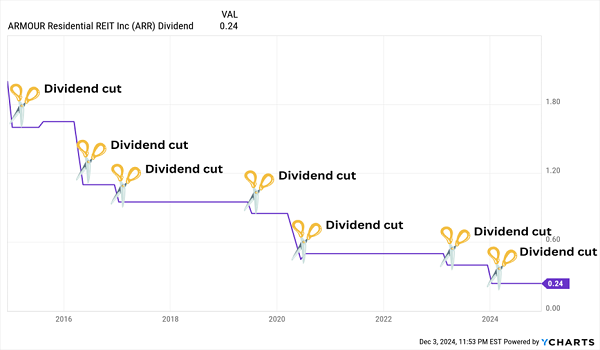

However, any prospective investors will have to overcome a significant mental hurdle: namely, Armour’s horrific dividend track record.

Armour Cuts and Cuts and Cuts Its Payout

It feels nearly impossible to trust Armour. But the company is trying to show some signs of life. ARR has strung together several quarterly core EPS beats, and significant core earnings growth is expected over the next couple of years—enough so that a hike to Armour’s monthly dividend might not be out of the question. Meanwhile, ARR shares trade for 92% of book value and less than 5x core EPS estimates.

Retire on Just $500K With the Dividend “A-Team”

Armour is a tempting dividend swing play given its world-class yield and potential for continued upside.

But from a retirement standpoint, we can’t risk the uncertainty of a company that has burned income investors a half-dozen times or so over the past decade alone!

Yes, if we want to retire on dividends alone, we need high yields—I try to target a portfolio average of 8%, which can generate $40,000 a year on just $500,000 (less than half of what experts say you need to retire)!

But we also need stable, secure payouts that won’t be whittled away every year or two by managers that can’t meet their numbers.

That’s why I only target the highest-quality payouts in my “No Withdrawal” Retirement Portfolio!

My “No Withdrawal” portfolio can do what your typical blue-chips-and-basic-bonds retirement portfolio can’t: Allow you to retire on dividend and interest income alone, without ever having to touch a penny of your nest egg.

It might sound like hype, but it stands up to simple math. I’ll even show you my work:

- Take a $500,000 nest egg.

- Put it to work in a portfolio yielding 8%.

- You’ll earn a $40,000 “salary” of dividends and interest from your retirement account.

Tack on your Social Security payments, and you’re looking at a much friendlier retirement budget once you call it quits at work.

And if you have an even bigger pile of cash to plug into our “No Withdrawal” Retirement Portfolio? Well, even just the thought brings a smile to my face—and I bet you’re wearing one, too.

Let me show you the stealth payout plays that Wall Street overlooks—names that do yield the 7%, 8%, 10% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends!

Recent Comments