That dip didn’t last long, did it?

The S&P 500 is back around 2,800, the Dow is back around 26,000, and stocks – which frankly were never really “cheap” even in the December doldrums – are back to being hilariously overpriced. And that’s a problem on two fronts.

- It makes finding values – an important aspect in collecting big total returns – exceedingly difficult.

- The more richly stocks are priced, the harder they can fall, making dividend landmines more plentiful in the current environment.

How bad is it out there?

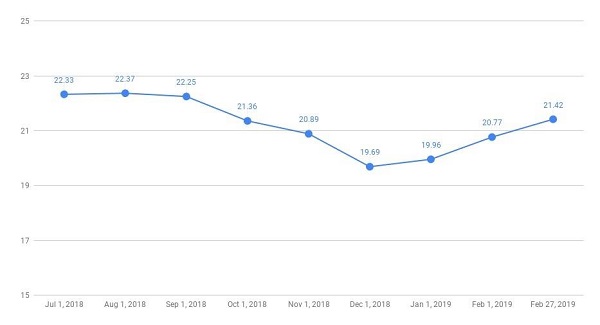

Here’s a look at the short-term, which shows valuations are clearly back to their pre-dip “normal.”

Data Source: Multpl.com.

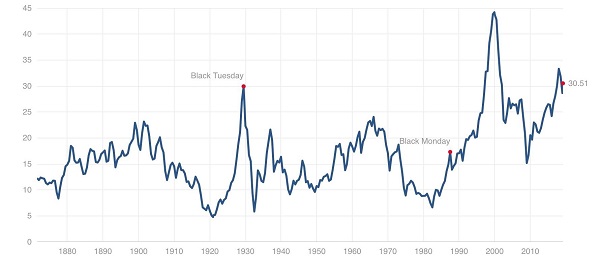

If that’s not worrisome enough, here’s a look at the Shiller P/E ratio, which takes into account inflation-adjusted earnings from the previous 10 years. Stocks have only been this expensive or more twice in history … and that preceded two massive bear markets.

Source: Multpl.com

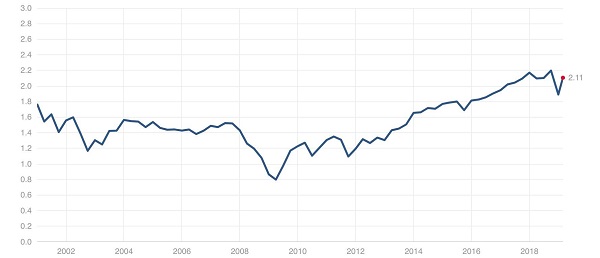

And if you think it’s just some trick of earnings, it’s not – stocks are overpriced on a price-to-sales basis, too, trading at more than double revenues.

Source: Multpl.com

You want to buy stocks when they’re cheap because that adds to their capital-appreciation potential and tends to correspond with a larger-than-average yield – a “double bonus,” if you will.

The opposite is true if you buy stocks when they’re costly. Not only do you have more downside potential, but typically you’re buying in at a much smaller yield than typical.

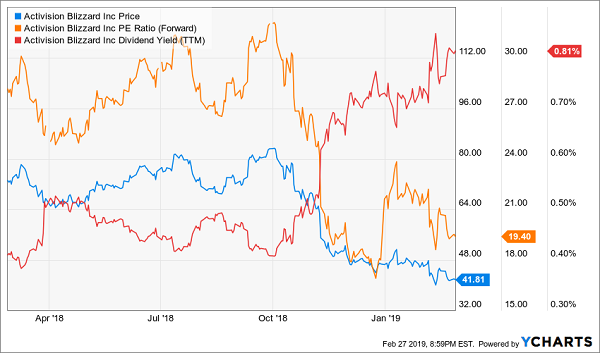

We can see this relationship in Activision Blizzard (ATVI) – not a prolific yielder, but a serial dividend raiser that has delivered serious upside in recent years. That is, until late last year when the markets dropped, and investors could no longer justify the fat premium on ATVI shares …

Game Over

I want you to watch out for the following four stocks, but for two separate reasons. In a couple of cases, these are troubled stocks that are just asking for a reason to get knocked into the abyss. But two of these stocks are actually growth-and-income plays that have simply become too expensive of late … and could use a broad-market gut-punch to drag them back down to more buyable levels.

Intuit (INTU)

Dividend Yield: 0.75%

Tax software isn’t the most scintillating business in the world as far as narratives go. But Intuit (INTU) – the company behind TurboTax and QuickBooks – has turned do-it-yourself accounting into simply sizzling returns over the past decade.

Intuit (INTU) Is Nearing a 10-Year 10-Bagger!

There’s no smoke ‘n’ mirrors here. These are legitimate gains produced by solid, steady business growth over the years. Consider this:

The company now boasts 3.9 million QuickBooks Online subscribers – with nearly 1 million of those coming internationally – in its fiscal second quarter ended Jan. 31, up 38% year-over-year. The company’s QuickBooks Capital business-loans division also boasts roughly $277 million in cumulative loans since it launched a little more than a year ago.

And Intuit still sees pretty robust growth going forward, including 8%-10% revenue growth for fiscal 2019, and adjusted profit growth of 11%-12%.

Indeed, I’ve been bullish on this stock previously, saying, “This is another prolific dividend grower that has more than doubled its quarterly dole in five years. And its DIVCON rating of 5 implies that INTU is well-armed enough to continue the upward march.” Intuit’s shares are up more than 27% since that call.

But the stock needs a breather. INTU now trades at more than 50 times trailing earnings and nearly 40 times analysts’ projections for current-year profits – both on the extremely high end of its historical valuations. And while Intuit has never been a particularly lofty yielder despite its rapid pace of payout growth, its current yield of 0.7% is awfully lean.

Good company, bad price. Stocks like this almost give us a reason to root for a quick, violent pullback so we can jump into quality companies like this at a more palatable valuation.

Covanta Holdings (CVA)

Dividend Yield: 5.9%

Covanta (CVA) technically is a “waste management” company, and that would typically check the “stable, reliable revenues” box in your mind. After all, good economy or bad, everyone needs to get rid of their trash.

But that’s not Covanta’s full story.

The company also generates electricity from waste, across several countries, including the U.S., U.K. and Japan, making it an alternative-energy play – an attractive option in an investing environment that increasingly values ESG.

The problem is, while the company has grown its geographical reach and its top line, it’s long had profitability and free-cash-flow issues. As a result, management is stuck between a rock and a hard place – it keeps pledging its commitment to the payout, but it hasn’t been able to budge it from 25 cents quarterly since mid-2014.

Case in point? Right now, the highest estimate for 2019 profits is a mere 30 cents per share, versus a full $1 pledged to investors. Things technically look better on a cash-flow basis, but not peachy – even if the company meets the midpoint of its own 2019 FCF guidance, it’ll come up short of what it must pay out in distributions.

That’s bad enough. Paying 57 times the most optimistic estimate for 2019 earnings, or more than 200 times the consensus analyst estimate, for it? Yikes.

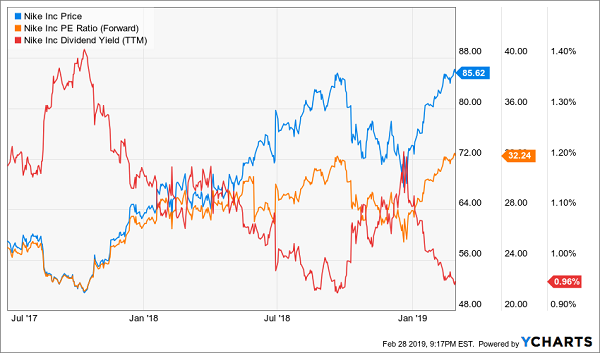

Nike (NKE)

Dividend Yield: 1.0%

In late 2015, investors saw something they hadn’t seen in many years:

Nike (NKE) was tripping over its own shoelaces.

For a period of nearly two years, Nike lost nearly a quarter of its value, including a 2016 in which its 18% loss made it the worst stock of the Dow. Rival Adidas (ADDYY) made inroads against both the American sports-apparel giant and relative upstart Under Armour (UAA), which also jabbed at Nike by becoming more aggressive in seeking out athlete endorsements, sometimes leading to bidding wars.

But Nike has found its stride yet again, ramping up considerably through most of 2018 before pulling back with the rest of the market in Q4, then putting together a 15% year-to-date rally to put it at fresh all-time highs.

Nike’s brand has become resurgent, often topping the list of favored athletic-apparel brands among men and women alike in the 18-to-34 demographic. The company’s support of Colin Kaepernick and placement of the controversial football player in its ads, while sparking immediate concern, proved to be a boon to sales. Revenues blew through expectations in fiscal Q2, during which that ad was released. Meanwhile, Oppenheimer analyst Brian Nagel considers the retailer a “top pick” and thinks it can crack the $100 mark in the next 12 months thanks to its strong operating performance and potential to keep boosting margins.

Again, this all just comes down to price. Much of Nike’s gains are coming on margin expansion, and its all-time-high prices have lifted NKE to multiyear-high valuations. Meanwhile, the yield has shrunk to a mere 1%.

Nike (NKE) Is as Overpriced as Its Basketball Shoes

This company is an American powerhouse, and one heckuva dividend-growth play too, with the payout rocketing almost 90% over the past half-decade. It’s just too, too expensive right now.

Wait for gravity do its thing first.

VEREIT (VER)

Dividend Yield: 6.9%

VEREIT (VER) is one of the largest single-tenant commercial real estate investment trusts (REITs) in the country, boasting roughly 4,000 properties across 49 states, Canada and Puerto Rico. These properties are leased out by 661 tenants spanning retail (42%), restaurants (21%), offices (19%) and industrial space (18%). That kind of diversity should in theory help a great deal – when one area is down, other types of properties can keep the portfolio propped up.

That’s the theory, anyway.

But first, a refresher: VEREIT is actually the old American Realty Capital, whose stock was obliterated thanks to an accounting scandal. The fallout was so bad that the REIT went with a full-scorched-earth strategy, ditching its CFO and even rebranding with a new name.

The good news? VEREIT has played by the rules since adopting the new moniker in 2015. The bad news? Operational and stock performance alike haven’t set the world on fire.

VER shares are only a few basis points better than breakeven for the past three years, and while it’s up about 23% on a total-return basis (thank you, dividends!), that’s still less than half what the S&P 500 would’ve given you over that same time period.

Most recently, VEREIT delivered a net loss of about $92 million for 2018, let its debt tick up slightly higher to $6.1 billion, and saw its adjusted funds from operations shrink from 74 cents per share to 71.9 cents. Moreover, the company still has a 5%-plus exposure to struggling, sub-investment-grade Red Lobster, which doesn’t give me the warm fuzzies.

So while the company’s shares aren’t grossly overvalued at 11 times adjusted funds from operations (FFO, a key profitability metric for REITs), they are awfully expensive for a company that has offered mostly downside for years and hasn’t touched its dividend since its 2015 “reinvention.”

How to Earn 12% Annual Returns For Life!

I know it seems crazy to think about a difference of a few dollars in a stock price when you’re planning for 20, 30 years down the road. But ignoring valuations on your dividend holdings can bite you in the butt twice – by clipping your income (lower starting yield) and your potential capital gains.

You need every edge you can get if you’re going to generate enough cash in dividends to sustain you through retirement. Which is why I refuse to overpay for any of the stocks in my “12% for Life” portfolio.

I know – 12% sounds like a crazy target given that the market averages between 7%-8% in annual gains, and given that even most professional money managers have a hard time besting the S&P 500.

You can’t just throw darts at a list of Dow Jones stocks and hope for the best. I’ve been buried in research and management interviews for months trying to identify stocks that can deliver these three vital traits:

- High current yield

- Dividend growth track

- Explosive capital gains potential

As a result, every single stock in this portfolio is poised to generate at least 12% in safe, annual returns.

I’ve weeded out dozens of potential yield traps and companies whose supposed “mega-trends” are actually just one or two years from dying out. What remains is an all-star roster of picks that will deliver the double-digit annual returns you need to retire worry-free after decades of busting your hump.

My “12% for Life” portfolio is not your garden-variety dividend portfolio. There’s no Coke (KO), there’s no Kraft (KHC), there are no sleepy blue chips with ho-hum yields. Instead, you’ll find picks like:

- One stock that’s already boosted its dividend payments more than 800% over the past four years, and has at least another decade of double-digit growth left in the tank!

- Another is a “double threat” income-and-growth play that rose more than 252% the last time it was anywhere near as cheap as it is right now!

- And we have a 8.2% payer that raises its dividend more than once a year, and will double its payout by 2021 at its current pace!

This portfolio delivers everything: capital gains, nest egg protection and three times more income than most retirement experts say you need! Even if it “merely” hits its target of 12% returns annually, you’ll double your portfolio’s worth in just six years! Plus, it’s built to be more durable against market downturns like 2008-09, which wrecked scores of retirement accounts across America.

It’s easy to see how this portfolio will give you the retirement you’ve planned for all these years. The dividend income alone will tackle your monthly bills, while the growth will leave enough left over for all the extras – the vacation home, the kitchen remodel, the second honeymoon to Bali.

All the while, you’ll be able to grow your nest egg, which acts as extra protection against life’s ugly surprises.

Let me teach you how to earn 12% for life. Click here and I’ll GIVE you three special reports to double your nest egg. You’ll receive the names, tickers, buy prices and full analysis for seven stocks with wealth-building potential – completely FREE!

Recent Comments