If you own any real estate investment trusts (REITs), make sure you forward this article along to your tax advisor!

Historically, REIT distributions have been considered nonqualified dividends by the IRS. This means they usually get taxed at your regular income tax rate.

However, REIT investors now benefit from the same tax break that “pass through” businesses receive. As a general rule, REIT investors are now allowed to deduct 20% of their REIT dividend income.

(This tax update is adapted from our new book How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact. You can grab your copy here.)

Before we dive deeper into the REIT equity pool, let me give the usual disclaimer that I am not a tax professional myself. (I do, however, spend a healthy amount of time in my CPA’s office keeping him and his staff hustling to crunch the numbers on my various business interests.)

Now, back to REITs. For whatever reason, income investors don’t buy enough of them, in my opinion. Perhaps it’s because these stocks get lumped into one asset class (like utilities, or municipal bonds.)

But REITs run the gamut, from retail landlords (which have been getting crushed) to self-storage REITs (which benefit from Americans accumulating more and more “stuff” and having to put it somewhere).

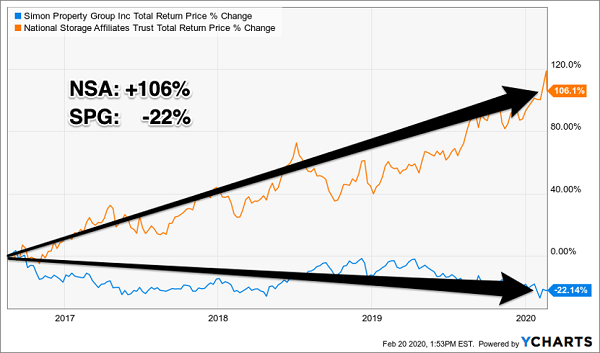

For example, let’s take one of the best retail REITs, Simon Property Group (SPG), and compare it with my favorite self-storage REIT, National Storage Affiliates Trust (NSA). Both are best of breed in their respective industries. However, one breed is becoming increasingly extinct!

I’ve never recommended SPG because, in recent years, I’ve been concerned that Amazon.com (AMZN) was simply going to eat its tenants’ lunch. After all, Amazon packages arrive at our doorstep daily, and each purchase we make on Amazon is one less drive we make to a local store (one that, potentially, has a rent payment due to Simon.)

On the other hand, National Storage runs facilities and rents out space in the fastest growing markets in the US. When we initially bought the stock for our Hidden Yields portfolio in August 2016, the locations that housed the vast majority of its facilities (92% of them!) were projected to grow 45% faster than the national average.

The rising tide lifted NSA’s payout and stock price. Meanwhile the Amazon cloud put a lid on SPG. SPG was the same “investment vehicle” as NSA in theory, with polar opposite returns in practice!

2 REITs with Nothing in Common

Financial websites say that NSA yields 3.5% today, but it’s going to pay even more over the next 12 months. The stock raises its dividend every couple of quarters (usually twice a year). Which means we can safely pencil in at least 3.7% from NSA in dividends in the year ahead.

(And given the choice between the 3.7% from NSA or another non-REIT, we’ll likely take the REIT and the tax break.)

What if we need more current income? After all, we could pile a million bucks for $37,000 or so in an annual dividend salary. That’s not bad, but there are REITs that pay even more.

For investors who need a pay raise today, consider a mortgage REIT like Blackstone Mortgage Trust (BXMT). Business-wise, it has nothing in common with SPG or NSA. But its REIT structure, like SPG and NSA, means the firm:

- Receives its own tax break from Uncle Sam, provided that

- It dishes most of its profits to us in the form of payouts.

The firm sports a $0.62 per share quarterly dividend (good for $2.48 per year) that is well-covered by earnings. This equates to a generous 6.2% current yield at today’s prices.

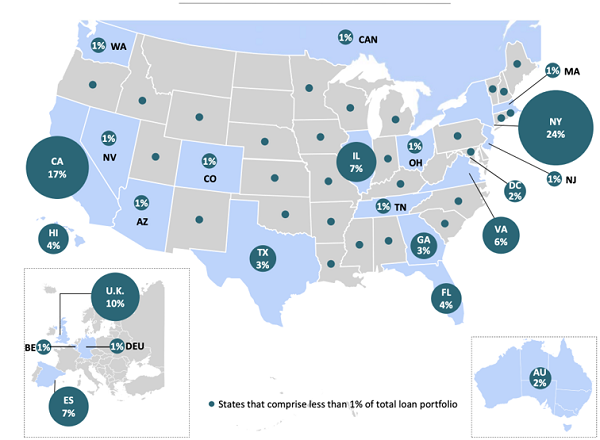

Parent company Blackstone Real Estate’s access to deal flow has helped BXMT build this impressive and geographically diversified commercial loan portfolio in just over six years:

The Sun Rarely Sets on BXMT’s Budding Commercial Empire

Another benefit of BXMT having access to (read: sharing) Blackstone’s management team is the know-how and expertise to write a smart deal.

Its weighted average loan-to-value (LTV) ratio is a conservative 62%—which means it has a big 38% equity cushion against real estate price declines. (Contrast this with your average home buyer who has perhaps 5% to 10%—or rarely an old school 20%—equity cushion via his or her down payment.)

BXMT’s oldest existing loans are 6+ years and, impressively, there has not been a bad one yet!

A perfect 100% of BXMT’s loans are being paid on time.

Again, on paper, BXMT is the same “type of stock” as SPG. Both are REITs, a classification that should make your CPA smile. However, once again, that’s where the similarities end.

If you’re a Contrarian Income Report subscriber, you’ll fondly remember when we added BXMT to our portfolio three years ago. We didn’t do it for the tax benefits—we did it for the dividends, and stayed for the price appreciation:

2 More REITs with Nothing in Common

How long REIT dividends will enjoy their favored status? It’s anybody’s guess. But while their payouts are in favor, make sure that the person who files your taxes (whether it’s you, or a professional you hire) knows about the 20% kicker.

Buy REITs right and you have near-perfect income investments. Not only are they tax advantaged for us as well as the firm itself, but these dividend machines are really the new blue chips for income investors.

But are they pullback-proof payouts? Yes, some are. In fact I’ve got my eye on 5 stocks that sail through epic market meltdowns like the one we saw on Monday.

And these high yield tanks pay up to 9.8%! If you’re after big, safe dividends then these are the stocks for you. Click here and I’ll share my 5 favorite meltdown-proof dividends with you right now.

Recent Comments