Stocks or bonds? With the market off to an inauspicious December start, you may be thinking about shuffling some money from equities into income.

But rich guys and gals know better than to choose. They blend the best of both worlds to collect interest and enjoy share price upside! And we can too.

Their secret tickers? Convertible bonds. (Before the holidays you may be tempted to add some convertibles to your portfolio simply so that you can brag about them to friends and family!)

Convertible bonds, like the preferred shares we have discussed recently, pay regular interest. In this way, they act like bonds. You buy them and “lock in” regular coupon payments.

But convertibles are also like stock options in that they can be “converted” from a bond to a share of stock by the holder. So you can think of them as bonds with some stock-like upside.

Switching from creditor to shareholder can be a lucrative move. But buying convertibles does require individual research–and heartburn. Take Tesla’s (TSLA) debt that holders can “convert” March 2021 into Tesla stock for a $359.86 conversion price. Today that’d be an underwater trade for bondholders, with the stock price about $25 lower. This means investors are likely to continue holding Tesla bonds rather than pay $25 per share out of pocket to own the stock:

These Bond Holders Have Heartburn

This sounds fine until we consider that convertibles already pay less interest than regular bonds because of their additional lottery ticket potential. (Tesla’s convertible bonds only yield 1% or 2%.)

When we settle for 2% or less, we need upside–and we’re not amused when Elon Musk’s “antics” send his company’s share price lower. I’d rather save us the research, headaches and heartburn by “outsourcing” our convertible bond portfolios to industry experts. As usual, we’ll look to closed-end funds here for three reasons.

First, we can find CEFs that pay more than individual convertibles we’d be able to buy. Fund managers get the first phone call on these types of deals. Plus, they have access to cheap money that lets them leverage their returns relatively safely. We’re going to discuss an excellent convertible-focused CEF fund yielding 5.9% in a moment.

Second, CEFs can (and often do) trade for discounts to their net asset values (or NAVs—the street value of the convertible bonds they hold). Thanks to current pessimism in CEF-land, the fund I’m going to highlight trades for just 96.5 cents on the dollar.

Third, we can hire convertible bond manager Thomas Dinsmore to work for us for free. He usually charges a 1.1% management fee, but thanks to this 3.5% discount, his remuneration is “comped.”

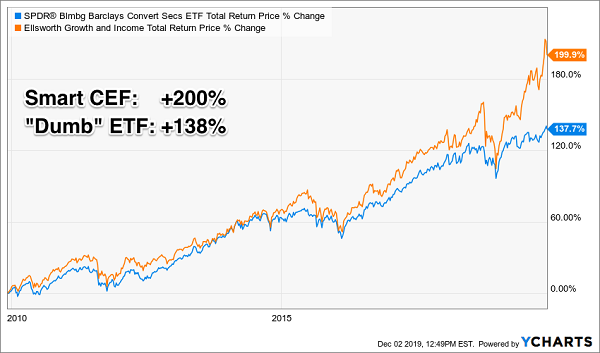

While few know about this obscure fund, more aspiring country clubbers know CWB. The SPDR Barclays Capital Convertible Bond ETF (CWB) is the most popular mainstream (read: widely marketed) vehicle to purchase convertibles. It lets investors brag that they own a basket of convertible bonds. But if their friends are impressed, their accountants are most decidedly not.

CWB has, on the surface, been fine. It’s generated 138% total returns over the last ten years. That’s not bad for a “dumb” rules-based formula. But convertibles are nuanced income investments that should be handpicked. When they are (via a CEF), their edge adds up over time:

Putting CWB’s +138% Gains in Perspective

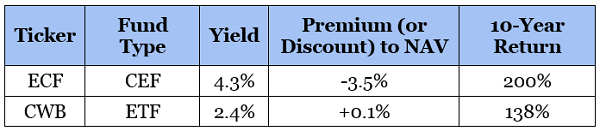

Our “pure play” convertible bond fund in CEF-land is the Ellsworth Growth and Income Fund (ECF). It pays 4.3% today (versus CWB’s 2.4% yield) and trades at a generous discount to its NAV (versus a slight premium for CWB):

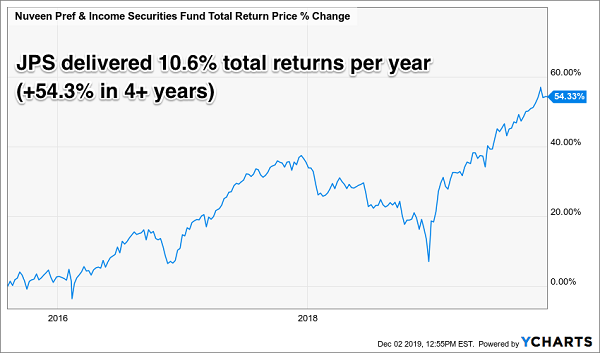

For you Contrarian Income Report subscribers, this discussion on convertibles may ring a bell. Our asset manager Nuveen recently expanded its Preferred & Income Securities Fund’s (JPS) mandate. Along with preferred securities, the fund began buying hybrids such as convertible securities. (Again, this is a fancy way of saying the fund started purchasing debt that has options to convert to equity.)

I advised subscribers to not to worry about JPS’ mandate change because we trust the management team and we’re not scared of convertibles. This turned out to be a great “buy and hold” by us income investors because JPS has delivered 10.6% total returns per year (including dividends):

JPS: A Perfect Retirement Investment

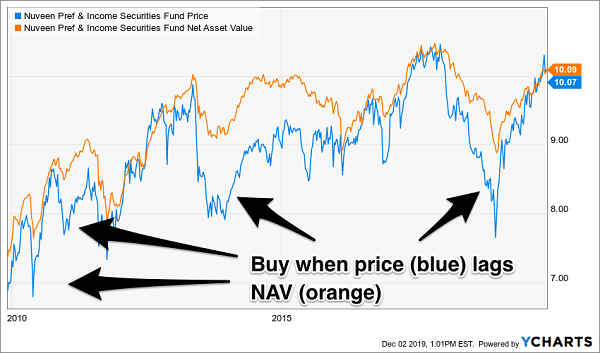

There are better times to buy JPS than others. I prefer to cherry-pick our entries and purchase the fund when its price lags its NAV. Newbies to CEFs might think this is a rare occurrence (especially since the fund usually yields 7%+) but every few years, for whatever reason, the fund falls a bit out of favor and we have a nice opportunity to add to our position:

A Good Fund, Frequently at a Big Bargain

Same goes with ECF. It’s frequently traded at 10%, 15% and even (briefly) 20% discounts over the past decade. Which means you can buy this fund for as little as 80 cents on the dollar—if you’re patient, and paying attention to your Contrarian Income Reports!

And we contrarians are patient if nothing else! There’s no reason not to be when we have PERFECT income investments flashing buy signals today. I’m talking about dividend machines ready to pay you 6%, 7% and even 8% per year in dividends alone while giving you an additional 10% to 15% in price upside.

If a fat dividend with 18% to 23% total return potential per year isn’t perfect, I’m not sure what is!

Give me just four more minutes of your day, and I’ll walk you through the rest of my perfect income formula. You’re already halfway there, thanks to your successful completion of my “CEFs 101” lesson. Click here and we’ll turn your 2% payers into 8% dividends with growth to boot.

Recent Comments