A stock’s yield is only as good as its cash flow because, after all, a dividend is nothing more than a promise from a company.

CenturyLink (CTL) recently reminded us of this. Its promised $0.54 per share dividend exceeded its ability to pay. The firm’s payout ratio of 130% – the percentage of profits that it was paying as dividends – was an absurd overpromise that couldn’t last forever:

CenturyLink’s Payout Promise Was Always on Borrowed Time

CEO Jeffrey Storey insisted his team remained “committed to and confident in our ability to maintain the dividend.” I understood the commitment, but questioned the confidence–taking on debt to pay dividends is a losing game. But then again, what else is the guy going to say?!

As recently as February 8, I warned investors that CenturyLink was a high yield trap. It was inevitable that its lack of cash would topple any commitment and confidence. Sure enough, just six days later, Jeff and the boys made me look good by slashing their payout by a cool 54%.

The “all-knowing” market sniffed out some of Jeff’s BS beforehand, but not the full extent of it. CTL topped in late August and has spiraled downwards since. Shares are down 45% in just six months:

A 54% Dividend Cut = A 45% Price Cut (and Counting)

As we’ve discussed time and again, dividends are “magnets” that drag their share prices along. This is great when dividends are growing, but disastrous when they are slashed!

With CTL’s latest payout cut now in the rearview mirror, my publisher patted me on the back–and tasked me with finding eight more dividends likely to drop! Luckily for me, we have access to Blockforce Capital’s “DIVCON” system.

DIVCON is a an easy-to-understand 1-to-5 system, where DIVCON 5 implying the greatest chance of a dividend increase, and DIVCON 1 implying the best change of a payout cut.

The system looks at a company’s profits, cash flow, dividend histories, analyst sentiment and more to determine the overall health of its stock’s payout. These are many of the same investing metrics that I evaluate when analyzing stocks, so it should be no surprise that I often find myself nodding in agreement with DIVCON’s scores.

And DIVCON has plenty more red flags to plant today. Here are problem payouts you should be very skeptical of today.

Macy’s (M)

Dividend Yield: 5.9%

DIVCON Score: 2

While Macy’s (M) DIVCON score of 2 suggests the retailer is “likely to decrease/cut their dividends in the next 12 months,” I think the timeline is a bit longer than that. At the moment, Macy’s is paying out only 36% of its adjusted profits as earnings, and it generates enough free cash to pay its dividends more than twice over

That’s the nicest thing I can say about this dinosaur.

Macy’s operations are in terminal decline. Back in 2016, roughly 100 of the retailer’s locations were performing so poorly that the company said it would just shut their doors as their leases expired rather than spend the money to turn things around.

Shares have plunged roughly two-thirds from their 2015 peak as revenues have waned and profits have waffled. And it’s not going to get better. A quick look at what the analysts see going forward:

| Year | Revs | Adjusted EPS |

| 2018 | $25.97 billion | $4.18 |

| 2019(e) | $25.98 billion | $3.11 |

| 2020(e) | $25.99 billion | $2.95 |

Those numbers are troubling in so many ways:

- Wall Street’s typically optimistic-leaning analysts think that Macy’s is going to improve its sales by a rounding error for the next two years.

- These same analysts think that Macy’s is going to have an increasingly difficult time making a profit off those sales.

- Based on these projections, Macy’s payout ratio would jump from 36% to 51% without touching its dividend.

That dividend isn’t growing, either. The writing was on the wall in early 2017 when Macy’s failed to announce its usual increase; its quarterly dole has been stuck at 37.75 cents for three years now. If Macy’s does adjust its dividend, DIVCON’s analysts suggests it would be to cut or eliminate it.

International Game Technology (IGT)

Dividend Yield: 5.8%

DIVCON Score: 1

When you think of casino stocks, you think of the glitzy, glamorous resort companies: MGM Resorts (MGM), Las Vegas Sands (LVS) and Wynn Resorts (WYNN).

International Game Technology (IGT) is what you find when you pop open the hood.

IGT is a multinational gaming company that produces video slot games such as Wheel of Fortune Cash Link and Fuzzy’s Fortune. But more importantly, they also have developed various systems for sports betting, lottery, even casino rewards. If you’ve been in a casino, there’s a decent chance that IGT has in some way shaped your experience.

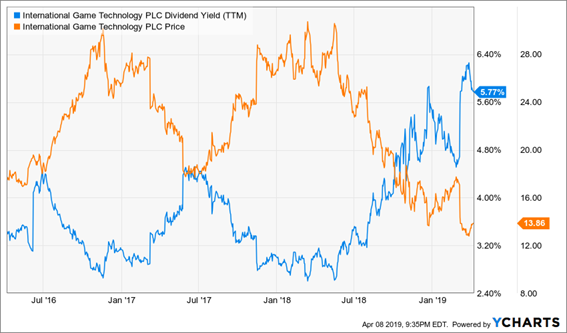

Despite its breadth of products and global reach, IGT has hit a plateau. Revenues declined in 2018 for the second consecutive year, and the company has posted losses in three of the past four years. The company’s 20-cent-per-share quarterly dividend has remained flat since 2015, and has been fully funded by profits just one year during that time. Negative free cash flow is a regular occurrence.

The only reason the yield keeps going up is because the stock keeps sinking. IGT shares plunged 12% in a single day this March after the company posted adjusted earnings of 24 cents per share that were well short of expectations for 33 cents.

That was the company’s sixth quarterly miss in two years.

DIVCON gives IGT its lowest score, and it’s well-deserved. Profits and cash are sparse, and management can’t even manage analyst expectations. Don’t keep sinking your dollars into this money hole.

Don’t Be Lured In by IGT’s Inflated Yield

Kraft Heinz (KHC)

Dividend Yield: 4.8%

DIVCON Score: 1

In February 2019, Kraft Heinz (KHC)–the consumer staples Frankenstein backed by Warren Buffett’s Berkshire Hathaway (BRK.B) and 3G Capital–said it would pay a 40-cent quarterly dividend.

The problem? That was 36% less than it paid the prior quarter.

Kraft’s Dividend Cut: A Symptom, Not the Sickness

Several investors and pundits were stunned, but not my readers. That’s because I had been warning about Kraft’s deterioration for a while, including articles in October and June 2018. (KHC is off 45% since that June call.)

DIVCON wasn’t fooled either, giving Kraft a score of 2 that implied a dividend cut was likely. But despite easing up on its cash obligation, the dividend-scoring system thinks KHC still is in danger of more cuts, and in fact has downgraded it to a 1 as of the end of March.

While Kraft’s new payout is more manageable, profitability continues to be an issue, with analysts expecting a 21% drop in earnings this year to $2.80 per share. And don’t forget: the company’s disastrous Q4 earnings and dividend cut also revealed that the company was being investigated by the SEC over its accounting and procurement policies. Even if nothing material comes from it, Kraft clearly needs to get its house in order.

Earn 28% Returns Every Year From America’s Safest Stocks

The problem with so many high yielders like Macy’s (M) and Kraft (KHC) is that they’re the end result of a stock-price beating. Typically, if you want truly safe dividends, you need to buy up overcrowded blue chips with much more modest payouts.

But what if I told you that you could have the best of both worlds: high yield and low risk?

You’d probably call me crazy. And you’d think I was crazier still once I told you that I’ve recently discovered a way to make low-paying and even non-paying blue chips such as Alphabet (GOOGL) and Facebook (FB) pay out giant distributions. In fact, this system can take 0% dividends and turn them into annual total returns of nearly 30%!

This system can take Wall Street’s most growth-first and income-last blue chips and turn them into “double threat” holdings that put traditional dividend stocks like Procter & Gamble (PG) and Coca-Cola (KO) to shame. Imagine using stocks such as Visa (sub-1% dividend) and Alphabet (not a penny in dividends!) to not only leg out double-digit upsides, but collect 8%-plus dividends to boot!

That’s the income-generating genius behind my new discovery: “Dividend Conversion Machines.”

These Dividend Conversion Machines have specialized businesses that allow them to wring high-single-digit dividends from some of the most skinflint companies in America. One of these “DCMs” takes Visa’s 0.6% payouts and magnifies it to 9.2%. Another DCM takes Google’s 0% and produces a 9.4% yield out of thin air.

This isn’t a complex options strategy. It’s not high-risk derivatives. It’s not the “next Bitcoin.” This is a stunningly safe strategy that’s essentially the same as buying traditional American blue-chip stocks. In fact, I’ll show you the strategy right now. Here are the four simple steps you’ll take:

- Launch your web browser.

- Go to your trading account.

- Instead of entering a buy order for, say, Disney by entering the stock’s “DIS” symbol, enter the 3-letter code for one of my 4 Dividend Conversion Machines instead.

- Instead of getting Disney’s 1.6% dividend, start collecting an 8%+ income stream!

That’s it! That’s all you need to do!

Best of all, these four dividend plays have one final trick up their sleeve that makes them perfect for retirement portfolios: They pay out their dividends monthly. So if you’re in retirement, you can easily plan your bills around your income payouts. Even if you’re not, you still win, because monthly dividends compound quicker than quarterly payouts, helping you grow your account even faster!

Let me show you how to reap 28% in annual returns from miserly blue chips today. Click here and I’ll introduce you to these four “Dividend Conversion Machines,” including names, tickers, buy prices and full analyses – AND throw in three other income-generating bonus reports – all for absolutely NO COST to you.

Recent Comments