“Hey Brett – is it time for us to sell MPW?”

Nothing makes subscribers more anxious to bank gains like a 105% winner! That’s what Medical Properties Trust (MPW) has delivered to us since we bought it in November 2015. Funny thing is, I’ve been getting questions about selling the stock since it was a mere double-digit gain for us. It’s a good thing we let this winner run!

Why We Let Our Winners Run

It’s especially important to let winners run when they are growing their dividend consistently. There’s rarely any reason to actually sell a stock if the company is consistently growing its profits and dishing them to shareholders.

Remember, there are three ways a stock can pay us:

- With a dividend today,

- By repurchasing its own shares (to make each remaining one intrinsically more valuable, because buybacks increase earnings per share), and/or

- By boosting its payout tomorrow so that its stock price follows its dividend higher.

My Hidden Yields formula is dedicated to the third – and most lucrative – strategy. It’s helped us to 14.2% annualized returns since our August 2015 inception. Our 105% gains on MPW show how effective this strategy can be when applied to a stock that already pays a lot!

Back to our initial question, is it time to sell? Let’s walk through my five “profit booking” signals for a perennial payout hiker.

Time to Sell Signal #1: Slowing Dividend Growth

If a dividend grower isn’t growing its payout fast enough, then it might be time to move on. Slowing dividend growth, remember, can be an ominous sign – namely that the firm doesn’t have the money!

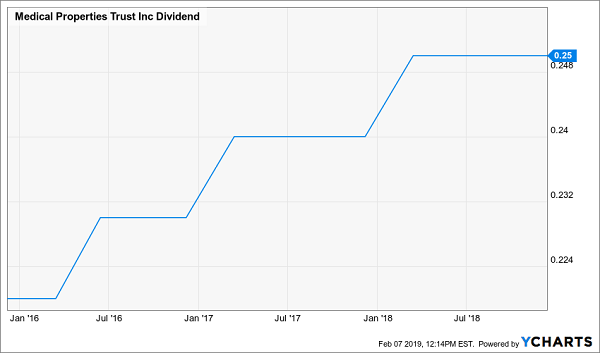

That hasn’t been a problem for MPW. It raises its dividend (4% to 5% hikes) every year. Plus, we’re due for another raise next month.

Due for a Dividend Raise Next Month

Plus, the company just announced that it’s going to be aggressive on the acquisition front in 2019. Historically Medical Properties has been a smart acquirer as its purchases have resulted in more cash flows and dividends for shareholders. The payout outlook is very good.

Time to Sell Signal #2: Yield Plus Dividend Growth is Too Low

MPW, as a real estate investment trust (REIT), uses dividends (and raises) in lieu of share repurchases to reward shareholders. This means our expected return from the stock can be simply calculated as:

Total Return = Current Yield + Expected Dividend Growth

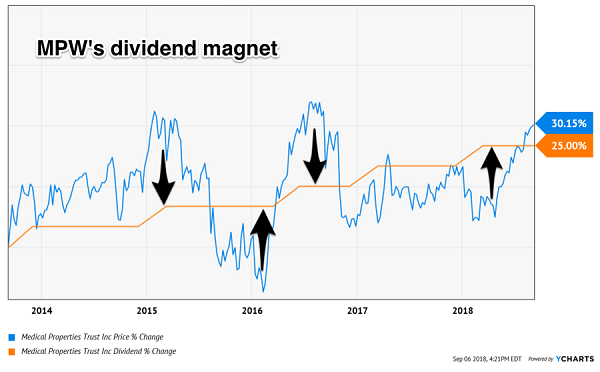

MPW pays 5.6% as I write, but a raise is on the way, which means it’ll likely pay 6% or more in the year ahead. Plus, over the next twelve months, investors will be drawn to the stock’s higher dividend. The higher payout will act like a “magnet” that will pull its share price along with it:

The Power of a Dividend Magnet

The chart shows that the stock price may over or undershoot the dividend growth, but over time it sticks with it. This magnetic payout growth plus current yield sets up the stock for 10% to 11% returns in the years ahead.

Time to Sell Signal #3: Dividend Coverage is Dicey

Dividends are great. Payout raises are even better. But they’re only meaningful when “well covered” by meaningful cash flows. That means the company generates more than enough cash to meet the dividend, reducing the risk it will be cut. So let’s consider FFO (funds from operations), which represents the amount of cash a REIT actually generates. It’s where our dividend originates.

I generally look for a dividend-to-FFO payout ratio below 80% for a REIT. (Remember, REITs are required to pay most of their earnings back to shareholders as dividends, so their payout ratios are typically higher than other stocks.)

MPW pays $1.00 per share per year in dividends today. Let’s go ahead and assume the company’s typical raise, which will take the payout to $1.04 in 2019. That will be well covered by the $1.42 to $1.46 per share in FFO the firm is projecting (which translates to a payout ratio between 71% and 73%). No problem here – far from it!

Time to Sell Signal #4: Business is Fine Today, But Maybe Not Tomorrow

Consider the retail store reporting good earnings at the moment but likely to be swallowed up by Jeff Bezos and Amazon.com (AMZN) tomorrow. This is the mistake many value investors are making today. They’re picking up spare storefront change on the train tracks.

We have no such concerns with Medical Properties, the only publicly traded company that invests solely in hospitals. When Chairman, President and CEO Ed Aldag founded the company in 2003, hospitals didn’t have traditional mortgages available to them. And traditional loan packages would force them to lock up all of their asset value as collateral.

Thanks to Ed’s vision, hospitals now have access to favorable funding and Ed’s firm owns a valuable market niche. After all, what could be more Amazon-proof and recession-proof than hospitals?

Time to Sell Signal #5: Low “Relative” Yield

This is the only test that MPW doesn’t currently pass with flying colors, and is the reason why the stock is a “Hold” (rather than a “Buy”) in our Contrarian Income Report portfolio. It’s the curse of 105% returns!

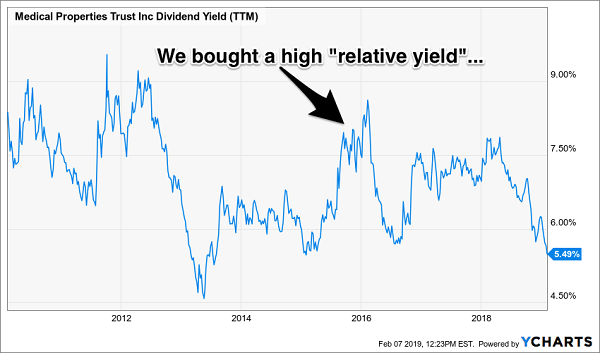

I prefer to buy dividend growers when their relative yields are high. If you’re familiar with the Dogs of the Dow strategy, this is a way to apply it to an individual stock. Simply look at the yield, and buy the stock when your dollar buys more dividend than usual.

In MPW’s case, its current yield is on the low end of its norm from the last nine years (versus the high relative yield we enjoyed when we purchased the stock):

Strive to Buy High Relative Yields…

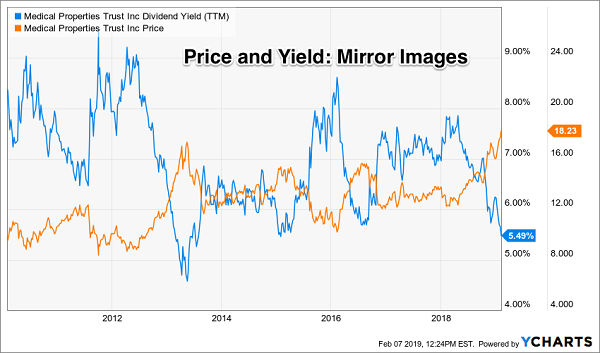

This worked out so well for us because the high yield was indeed a “buy sign” that the price was simply too low:

… Because High Yields Often Mean Low Prices!

Thanks to the generous initial yield we bought, and the subsequent dividend raises we enjoyed, the “yield on cost” of our MPW shares is 9% and climbing. We bought at $11.13 and shares now pay $1 per year (and likely more in the twelve months ahead.) Now that’s how you beat the broader stock market with low-risk high-paying dividend stocks. (Imagine how much higher that yield could be in just a few years!)

However, as I mentioned, MPW isn’t quite the slam-dunk for new money today that it was in November 2015. Fortunately a few other stocks are – a dozen to be specific!

Coming This Friday: 12 Dividend Payers with 100% Upside

How much money should you allocate to pursuing dividend stocks that will double your money?

As you can see, as much as possible. This dividend growth strategy is such a “slam dunk” for investing returns that there’s no reason to collect more current yields than you need right now. There are three big benefits to buying dividend payers that are likely to double your money.

Benefit 1. You invest a set amount of money into one of these “hidden yield” stocks and immediately start getting regular returns on the order of 3%, 4%, or maybe more.

That alone is better than you can get from just about any other conservative investment right now.

Benefit 2. Over time, your dividend payments go up so you’re eventually earning 8%, 9%, or 10% a year on your original investment.

That should not only keep pace with inflation or rising interest rates, but also it should stay ahead of them.

Benefit 3. As your income is rising, other investors are also bidding up the price of your shares to keep pace with the increasing yields.

This combination of rising dividends and capital appreciation is what gives you the potential to earn 14% or more annually on average with almost no effort or active investing at all.

Which future “dividend doubles” should you buy today? Well, you know me – I’ve got not one, not two but 12 best buys in this Friday’s issue that should safely double your money in the months and years ahead.

Remember, this dividend growth strategy has produced steady 14.2% annualized returns for my Hidden Yields subscribers since inception. In three-plus years we’ve cruised past the broader market.

If you achieve returns of 14.2% annually, you’ll double your money in five years. So if you haven’t been following this strategy, why not? The best time to get started is right now – before the dividend payers I mentioned begin to move. Click here and I’ll share these 12 stock names, tickers and buy prices with you on Friday morning.

Recent Comments