“Time out.” I yelled it with a hint of disgust. I didn’t even have to make eye contact with my assistant coach—we were on the same page.

We’d just watched the second air-ball three-pointer of the second half.

“Get in there for Reese.”

Reese shrugged and jogged off the court. I grabbed him lovingly by the shoulders. “Hey buddy — do you know why you’re out?”

He nodded slowly. “Because…I…shot… a…three…pointer.”

“And what did I just say in the huddle?”

“…To…not…shoot…three…pointers.”

I patted him on the shoulder. Reese was back in the game in two minutes. But I had to make the point.

We are not three-point shooters at age eleven. They are prayers, not shots.

Heck, we’re lucky to make our layups more than half the time. Hence our goal. Move the ball, work for close shots that at least have a chance at going in.

If this works for eleven-year-old hoopers, why are sixty- and seventy-year-old investors hoisting investment shots with no hope of landing?

We careful contrarians will take the generous “layup” yields all day long. The toll bridges that pay us 6.1% to 14.8% regardless of whether oil is at $50 or $100—those are our layups.

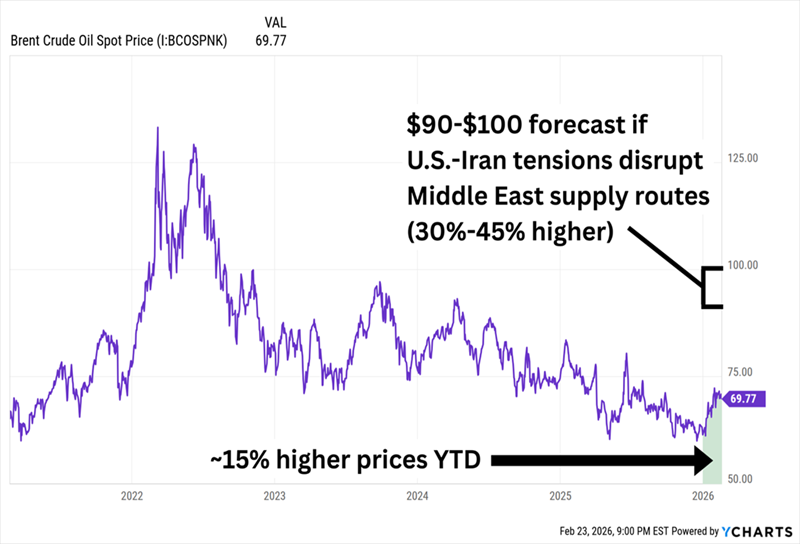

Oil is red-hot right now. Crude prices have been pointed north all year—a droopy dollar, OPEC+ production cuts, America’s military action in Venezuela. And the potential for conflict with Iran could spark a lot more upside from here.

Oil Could Gain Twice as Much If U.S.-Iran Boils Over

Which is exactly why everyone wants to shoot the three.

Sure, we could chase the Iran trade. Nordic American Tankers (NAT) has jumped 40%+ this year on spiking shipping rates alone. It pays a substantial dividend, too. But that payout is variable. It moves around so much that we can’t plan a retirement around it.

And shares could crash right back to earth if the Middle East situation cools off.

That’s a three-pointer with retirement money. I’d rather bank easy layups.

So let’s look at the pipeline “toll takers”—companies that get paid simply for oil and gas flowing through their infrastructure. They don’t care what a barrel costs. They just collect the fee. We’ll start with two of the bluest blue chips in the space.

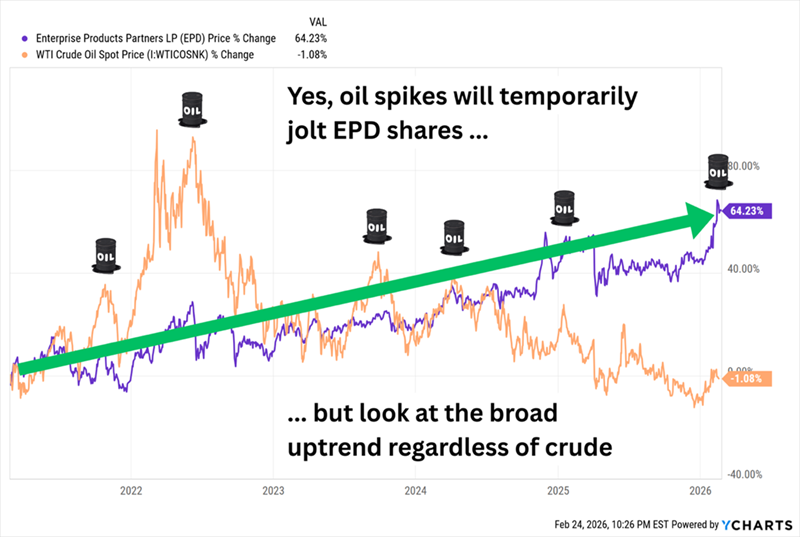

Enterprise Products Partners LP (EPD, 6.1% distribution yield) has 50,000+ miles of pipeline, more than 300 million barrels of liquids storage capacity, 26 fractionation facilities, and 20 deepwater docks. And while it’s not technically an “official” Dividend Aristocrat (because it doesn’t belong to the S&P 500), it boasts 27 consecutive annual distribution hikes. And at a 6%-plus yield, it’s one of the most generous members of the distribution gentry.

Do rising oil prices help the likes of EPD? Sometimes. Toll takers don’t exist in a bubble, and pipelines (including EPD) have joined the energy sector’s 2026 surge. But Enterprise Products clearly doesn’t need an oil bull run to keep you happy.

EPD Has Delivered Mostly Smooth Gains Amid Choppy Declines in Oil

Plus, EPD is just a few weeks removed from a Street-beating Q4 report in which it reported record natural gas processing inlet volumes, NGL fractionate volumes, and total pipeline volumes, and it delivered record adjusted cash flow from operations for full-year 2025.

Why I like it now: EPD has been extremely active. It recently converted its Seminole pipeline back to crude oil service (freeing it up now that the new Bahia NGL pipeline is handling liquids transport from the Permian), and said that its August 2025 acquisition of Occidental Petroleum (OXY) assets is throwing off “additional ‘bolt on’ growth projects.”

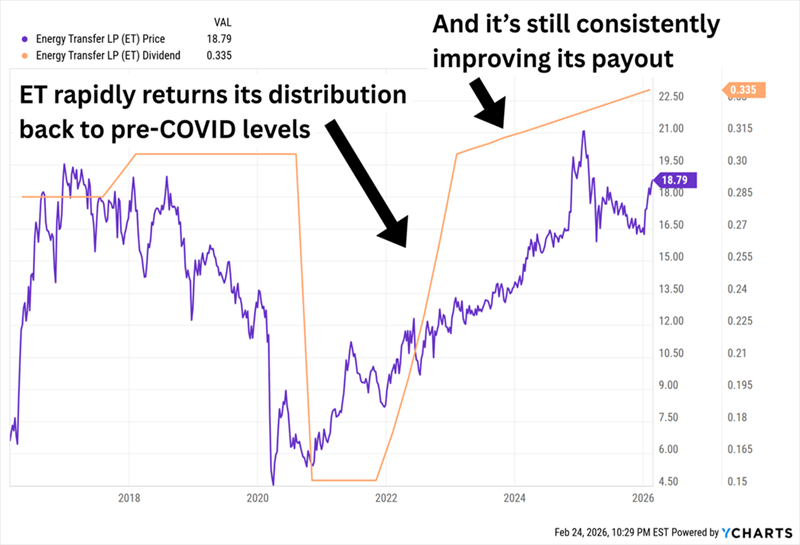

Then there’s Energy Transfer LP (ET, 7.1% distribution yield), another huge energy infrastructure player. ET features roughly 140,000 miles of pipelines transporting natural gas (~107,000 miles), crude oil (~18,000 miles), NGLs (~5,700 miles) and refined products (~3,760 miles). Its assets also include more than 70 nat-gas processing and treating facilities, 73 million barrels of oil storage capacity, 35 active refined products marketing terminals with 8 million barrels of storage capacity, stakes in other operations, and a developing large-scale LNG export facility in Louisiana.

Why I like it now: In three words? The AI boom. I mentioned in September that “ET said it had fielded requests to connect to more than 60 power plants in 14 states for new connections, and requests to connect to roughly 200 data centers in 15 states across the ET footprint.” Progress continues. Two months later, it signed a 20-year agreement with utility Entergy’s (ETR) Louisiana subsidiary. In January, ET began natural-gas deliveries to the first of three Oracle (ORCL) data centers.

And while ET might not be in Aristocrat territory, it has been persistently raising its distribution on a quarterly basis since 2021. How’s that for reliability?

ET Keeps Upward Pressure on the Payout, One Quarter After Another

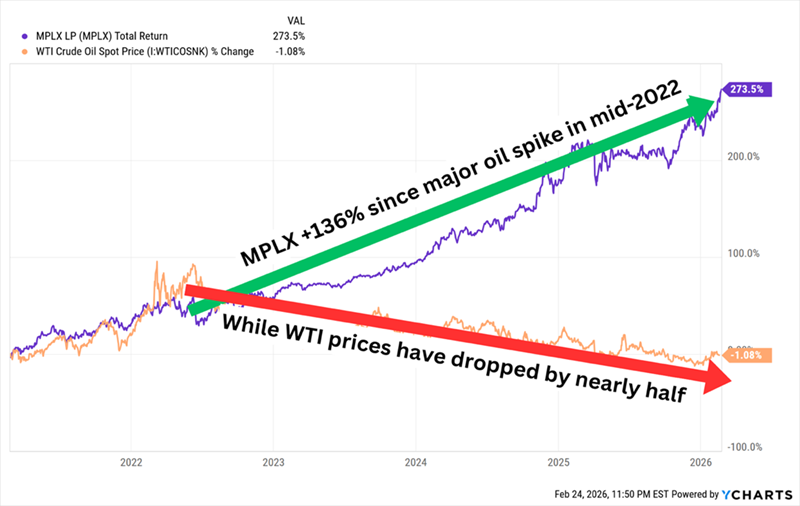

MPLX LP (MPLX, 7.3% distribution yield) was created in 2012 to hold Marathon Petroleum’s (MPC) myriad midstream assets. MPLX operates across two divisions—Crude Oil and Products Logistics, and Natural Gas and NGL Services—but those divisions encompass pipelines, refineries, NGL gathering systems and processing complexes, NGL fractionalization facilities, storage caverns, tank farms, motor vessels and barges, and other joint MPC/MPLX assets.

The annual distribution has grown every year since the company was spun off, and it has improved by double digits every year since the COVID dip.

Why I like it now: Several MPLX growth projects are expected to come online this year, including the Blackcomb and Bay Runner pipelines and the Harmon Creek III processing plant. But MPLX is such an operational squid—with tentacles in virtually everything—that no single catalyst will cause it to suddenly spike. Instead, MPLX consistently hits singles and doubles, which is enough to run up the score no matter what oil is doing. (Remember our layups?)

This Is One of the Best 5-Year Charts in the MLP Industry

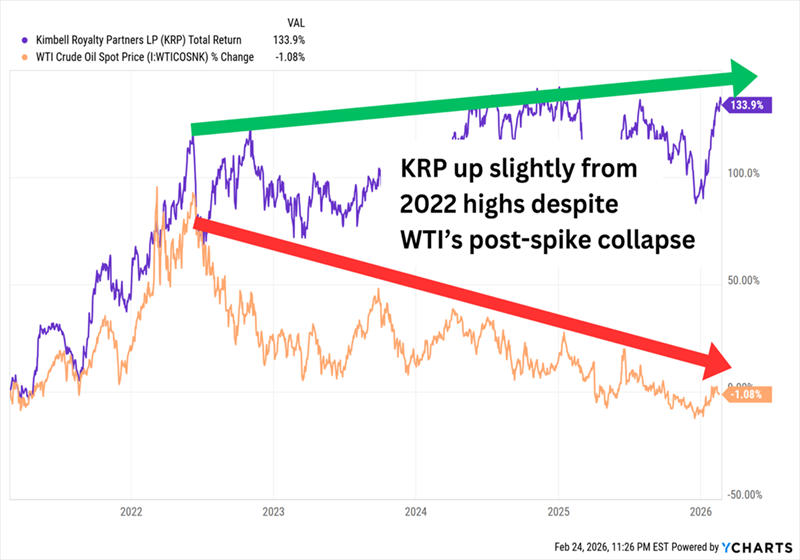

Despite what the name might otherwise indicate, Kimbell Royalty Partners LP (KRP, 11.3% dividend yield) isn’t taxed like a traditional MLP — and it’s not a royalty trust, either. But it does buy and own royalty interests in oil and natural gas. It’s an unorthodox business model in which it leases its 17 million-plus acres across 28 states — including formations such as the Permian, Eagle Ford and Bakken — to energy producers, who pay both an upfront “lease bonus” as well as a continuing royalty interest.

Why I like it now: KRP is a more direct play on energy prices than the toll takers; lower commodity prices decrease the royalties Kimbell collects (plus they can prompt producers to pull back on operations, reducing output and further impacting KRP’s profits), while higher commodity prices improve the royalties Kimbell receives. And production is expected to grow marginally this year. That said, KRP is also less volatile than the E&P industry and yields several times more than the sector average — and thus is less likely to come crashing down the way plain-vanilla energy stocks likely will if oil mellows out.

KRP Can Survive Oil Weakness, But Higher Crude Really Helps

Mach Natural Resources LP (MNR, 14.8% distribution yield) is a young MLP that formed in November 2017 and went public in late 2023. Its primary operations are in the Anadarko Basin, and it has additional assets in the Green River, San Juan and Permian basins. This is as much a natural gas play as it is oil (nat gas represents just more than half of its production). It’s also an efficient operator and has a good track record of buying assets at low valuations.

Why I like it now: MNR is very much a case where its strong operations haven’t yet been reflected in its valuation. Shares are breakeven since its IPO, whereas the MLP benchmark is up more than 40%. But it’s cheap. A common MLP valuation is EV (enterprise value)/EBITDAX (earnings before interest, taxes, depreciation, amortization and exploration expense), and MNR’s 4.2x valuation is well under the MLP average. Just be warned: This is an extremely variable distribution (based on cash available after a 50% reinvestment rate).

It’s Hard to Plan Anything Around These Paydays

This Is How We Can Live Off $500,000 … Practically Forever

These mammoth “toll taker” yields do have one mammoth drawback: They all (with the exception of KRP) don’t pay dividends — they pay distributions — which means you have to deal with different tax treatment and the dreaded K-1 form.

The additional IRS complexity would almost be worth it … if we didn’t have much better options at our disposal.

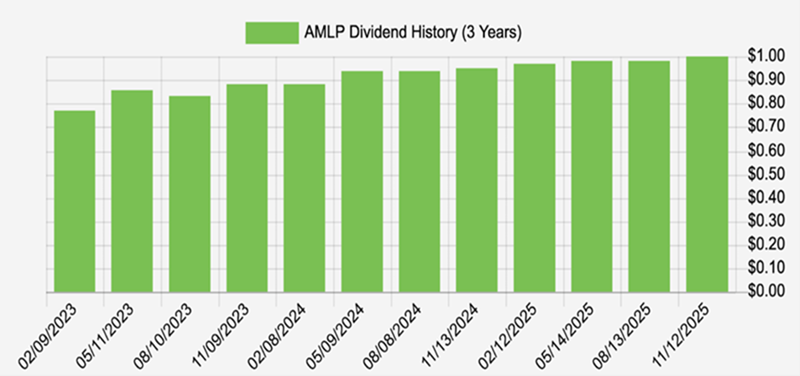

My preferred way to play energy is the Alerian MLP ETF (AMLP), which owns a basket of midstream MLPs (including some of the names above), pays us nearly 8%, and comes with a massive paperwork advantage. AMLP is structured as a C-corp fund, so you receive a plain old 1099 and file your taxes like normal.

AMLP also hikes its payout prodigiously:

AMLP Raises Its Divvie Regularly

This is how we live off $500,000 … practically forever. By buying elite 8% dividends that are favored by the current administration.

Of course, there’s no need to dump a full $500K portfolio into AMLP alone. Diversify! Let’s start with these 3 incredible monthly payers dishing out dividends up to 14.9%.

Recent Comments