Oh, the joys of home ownership. We found a moldy corner last week. And not a little spot, either.

A full farm thriving behind a brigade of stuffed animals wedged against the wall. (The stuffies block the airflow, providing cover for this ecosystem.)

Now Waiting Their Turn in the Laundry Line

“I see this every day in the homes down here,” the abatement guy explained his frequent trip to my old-home neighborhood. “Usually behind furniture jammed against the wall.”

Well, it’s the cost of doing business. The home has character. We like living downtown—makes us still feel kinda cool, sharing sidewalks with the neighborhood “kids” (anyone under 35) who live without stuffed animals upstairs.

The mold setback was a temporary one. The abatement guys are working today and the stuffies are sanitizing in the laundry.

Now, here’s what we did not do. We didn’t sell the house!

The house is still standing. Still appreciating in value. And still ours. We dealt with the setback. Which is exactly what one of our Contrarian Income Report subscribers has been doing with his portfolio for 138 straight weeks.

Roy M. from New Jersey wrote in recently with a report that made my whole week. Roy has an IRA that is exclusively CIR. Every single position, equally weighted. No picking favorites, no second-guessing your editor, no overthinking it. His reasoning?

“I like CIR but I don’t have the expertise to pick and choose from an already recommended list. Why would I pay for a site in which I still have to decide which ones are best? Why don’t I just buy ’em all equally?”

Love this!

Roy is a retired engineer, and engineers solve problems with systems rather than gut feelings. His system is beautifully “boring” (a compliment in our world). He keeps a rolling 10% cash position and lets dividends flow to cash rather than reinvesting them. When we add a new pick, he buys it. When I sell something, he sells it.

He even has a daily 30-second routine: pull up the CIR portfolio, count the 25 positions, flip to closed positions, and make sure the last one removed is still the last one removed. And when a new issue drops? He hits CTRL-F, types “action,” and executes whatever comes up. (Roy describes himself as a “lazy reader with a touch of dyslexia, LOL.” I’d call him the most efficient investor we’ve got!)

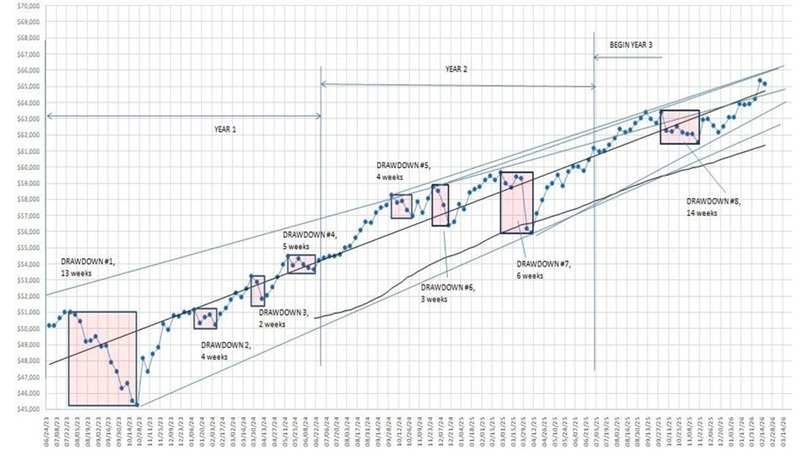

The results speak for themselves. Roy started with $50,172 in June 2023. His portfolio now sits at $65,163. That’s roughly 11% annualized returns with no new money added and no withdrawals taken. Not bad for a “lazy” strategy!

But here’s what I really love. Roy has tracked every single drawdown (temporary decline) over those 138 weeks and compared it to the S&P 500. There have been 8 drawdowns total, and the data tells our story better than I ever could:

- On average, when the S&P dipped about 6%, Roy’s CIR portfolio only fell about 4%.

- In one nasty stretch, the S&P cratered 18% while Roy’s portfolio dipped just 6%!

- Only once did CIR drop more than the broader market, and it was by barely a percentage point. This is excellent because the shallower the drawdowns, the more our portfolio compounds higher.

Roy’s 11% CIR Portfolio

Remember, Roy is a retiree on a fixed income. He doesn’t want drama. He wants to sleep at night and know his money is working. That’s exactly what he’s getting!

This is the whole idea behind what we call the “No Withdrawal” approach to retirement. We build a portfolio that throws off enough cash in dividends so that we never have to sell a single share.

Roy’s 25 CIR positions currently yield 8.3% on average. On a million-dollar portfolio, that’s $83,000 per year in dividend cash flowing straight to your account, paid monthly and quarterly. On a $500K stake like Roy’s? A cool $41,500 per year. Without touching principal!

Plus, Roy’s principal isn’t just intact. It’s actually up. He’s collecting the income and the appreciation—that’s the beauty of a dividend-heavy portfolio. The cash keeps coming whether the market is up, down, or sideways.

And when those drawdowns come (they’re normal, not unusual), CIR members do way better than vanilla investors riding the S&P rollercoaster. We are spared the 18% plunge. We simply ride a 6% dip while our dividends keep depositing!

It’s like my house. Mold showed up (“drawdown”), we didn’t sell the entire place (panic and lose money). I know it sounds silly—who sells their house over a moldy corner?—but that’s exactly what many “investors” do when the market dips 6%!

Roy? He plays it right. Eight drawdowns, eight recoveries, and 11% yearly gains. Keep on truckin’ indeed, Roy!

Roy’s results aren’t magic. They’re the product of a diversified, high-yield portfolio built to pay you in cash, not one that depends on stock prices going up, prayers being answered, and principal drained.

I call it the “No Withdrawal” Portfolio. It’s designed to generate 8%+ yields so you can live on dividends alone, without ever touching your precious shares. Need a miracle to retire? Nah. A “No Withdrawal” Portfolio will do just fine!

Want my free report that shows you exactly how it works, including my favorite monthly payers yielding up to 14.9%? Of course you do! Click here to get your free copy of “How to Live Off $500,000… Practically Forever.”

Recent Comments