There’s a group of stocks out there that most people think yield just 2%—or less.

But they’re way off. In reality, these “elite” payers yield 2X, 3X—and in the case of a stock we’ll talk about below, even nearly 4X that. I’m talking about a tidy 8.3% shareholder yield (remember that phrase) here.

This one has another advantage we love in a market like today’s, too: Its management team “buys the dips” in the share price for us. We don’t have to do anything at all!

Stocks like this are perfect for times like these, with the economy still ticking along nicely.

At the same time, we’re likely to see continued market choppiness as AI takes more industries to the woodshed.

But the major American insurance stock we’re going to dive into next doesn’t care. It’s already making money from AI. And as the tech boosts this company’s earnings and cash flows, I expect its 8.3% shareholder yield to climb higher still.

Aflac: A Dividend Stock at the Leading Edge of AI Disruption

We’ve discussed AI in the insurance industry before. The sector is ripe for AI disruption, as many of the things insurance companies do are good candidates for automation.

That’s not news to the management team at Aflac (AFL), which has automated 54% of its “wellness” claims—dental visits, eye care and the like. That’s a perfect job for AI because these customers don’t have to provide a raft of documents like, say, those filing disability or critical illness claims do.

The upshot for Aflac, a holding in the portfolio of my Hidden Yields service, is that it can reassign humans to more complex tasks, cut costs (including, yes, spending on new hires) and keep customers happy by processing claims faster.

What’s more, insurance is not likely to be disrupted the way, say, software stocks have been. After all, while you can use AI to “vibecode” your own app, you can’t use it to whip up your own insurance policy!

Which brings me to that 8.3% shareholder yield.

Shareholder Yield Beats Dividend Yield in Every Way

A dividend stock like Aflac has three ways to pay us:

- Its current payout: This is the dividend we get immediately after we buy.

- Dividend growth, which raises the yield on our original buy and acts like a “magnet” on the share price, with the rising payout pulling the share price up.

- Share buybacks, which cut the number of shares outstanding, juicing earnings per share and other per-share metrics.

Buybacks get a bad rap, but they shouldn’t, because when they’re done right (i.e., when the stock is cheap), they can juice our returns. This is another problem with the current yield—it tells us nothing about this buyback effect.

This is where shareholder yield, which includes buybacks and dividends, shines.

An 8.3% Shareholder Yield Is Aflac’s Best-Kept Secret

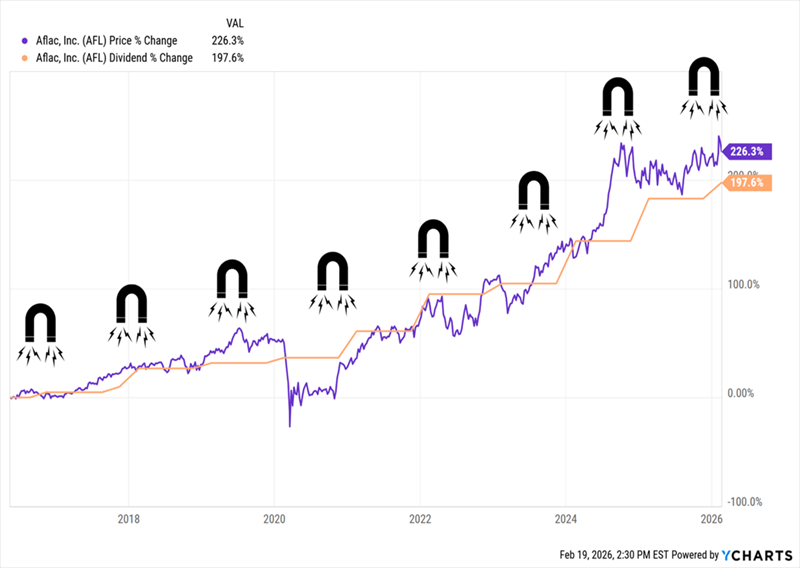

Over the last decade, Aflac has nearly tripled its dividend. That soaring payout has acted like a magnet, yanking the share price up as it’s soared:

Aflac’s “Dividend Magnet” Goes to Full Power

Because of that payout growth, investors who bought Aflac a decade ago are actually yielding 8.1% on their original buy now.

And that’s just the start of the company’s shareholder-return story.

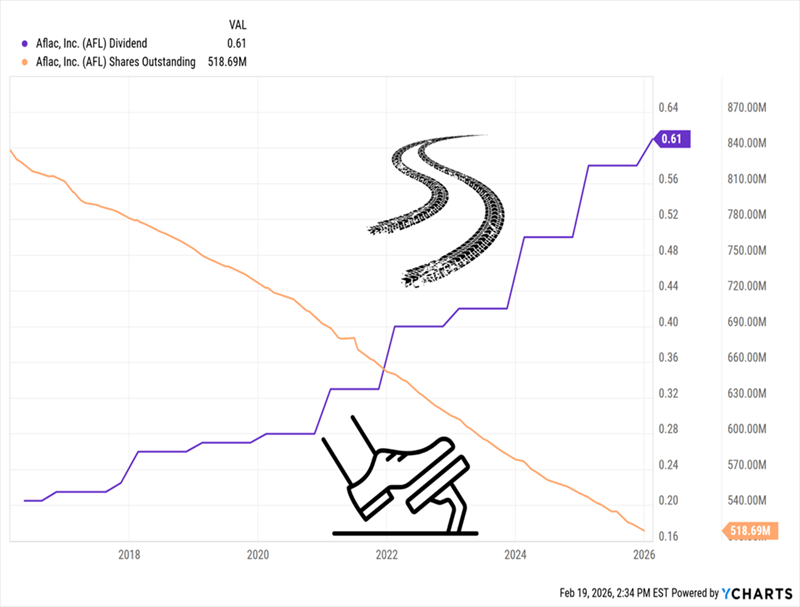

Let’s move on to buybacks: Over the last decade, Aflac has taken 38% of its shares off the market, making all of the company’s per-share metrics (most importantly earnings per share) look better. And earnings per share drive share prices over time.

In addition, those buybacks fuel dividend growth, as they leave Aflac with fewer stocks in which it has to pay out. It’s no coincidence that Aflac’s dividend growth (in purple below) has taken off as its share count (in orange) has dropped:

Buybacks Ignite Aflac’s Share Price

Let’s zoom in on the last year for a moment. In the chart below, you can clearly see that management has tempered its buybacks when the share price has strengthened (as in the summer of 2025), then accelerated them on dips.

Management Buys the Dip for Us

That’s the kind of smart buyback management we love—and it’s a lot different from what many companies do: robotically buy back the same amount of stock whether it’s cheap or dear.

Which brings me back to shareholder yield, which combines all three shareholder rewards: current dividend, payout growth and buybacks. To calculate it, take the amount spent on buybacks and dividends in the last 12 months, deduct share issuances then divide that into the company’s market cap.

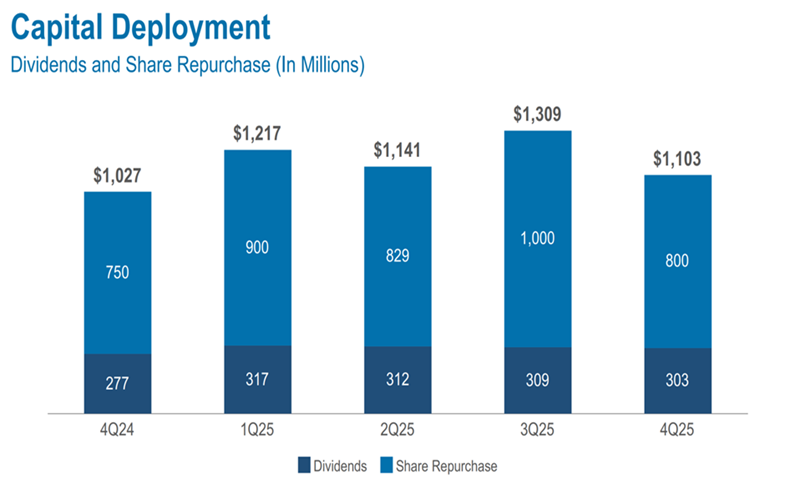

Aflac makes this easy for us: In its fourth-quarter earnings presentation, it broke this all down nicely:

Source: Aflac fourth quarter 2025 update

Here we see that in 2025, Aflac spent about $4.8 billion on dividends and buybacks, with a lean toward buybacks. (Which is okay by us, given the stock’s strong performance.)

With a $58-billion market cap (or the value of all outstanding shares) as of the end of 2025, we can say that Aflac has an 8.3% shareholder yield—again just a bit under four times the current dividend yield 2.2%.

Let me close with another fast mention of AI, because the tech ties back in here: As AI cuts Aflac’s costs and helps it tap new growth areas, I expect the company’s shareholder-friendly management team to share more of that wealth with us—and boost the firm’s shareholder yield as they do.

Start With Aflac—Then Build a Whole Portfolio of Big Shareholder Yields

Shareholder yield isn’t just another indicator to look at when picking dividend stocks. As we just saw with Aflac, it’s a whole new way of dividend investing.

Once you start applying it to other dividend stocks, you’ll be spotting big yields all over the place—and in plenty of stocks regular investors never bother to look at.

This strategy starts with a strong Dividend Magnet, like the one we saw with Aflac. As payouts rise, stock prices follow. Add in a smartly run buyback program and voila—you’ve got yourself a strong, and growing, shareholder yield.

To get you going, I’ve prepared a special Investor Bulletin that takes you inside my Dividend Magnet strategy and gives you a free Special Report revealing my top 5 dividend-growth stocks to buy now.

These 5 stocks are laser-focused on paying us through growing payouts, buybacks and smart business moves that put upward pressure on their share prices.

These 5 plays are cheap now—but I don’t expect that to last as their generous shareholder-reward plans get more attention. Click here to read more about them and get that free Special Report revealing their names and tickers.

Recent Comments