Real estate investment trusts (REITs) tend to shine when there is a lid on interest rates. And that rate top is secure, for reasons we’ll review shortly.

Net lease REITs, in particular, are compelling here. They are the boring landlords of the real economy. (Yawn? Love that reaction from vanilla income investors!)

The net lease landlords own the pharmacies down the street, the big-box retailers at the busy intersections, and the warehouses and distribution hubs we pass on the highway. These REITs sit back and collect rent checks while the tenants pay their own way.

Here’s how the business model works:

- The REIT buys the property and builds (or renovates) the facility to rent out.

- A net lease is signed, where the tenant pays the property bills (taxes, insurance and maintenance).

- The landlord collects rent–and doesn’t get stuck writing checks (or even taking a phone call) when the roof leaks!

- The net-lease REIT builds a portfolio of these leases, collects income and sends most of the rent back to us as dividends.

It’s the “mafioso” model of real estate. The customer pays expenses, the REIT collects and we get paid.

Of course we careful contrarians love upside in addition to our payouts. Today we have an attractive setup for price appreciation in REITworld.

As the Fed cuts rates, the dividends that REITs pay become increasingly attractive to income investors. Money markets don’t pay 5% any longer. Neither do many bond funds. But REITs pay…

And rates are likely to continue lower due to the rollout of AI across the economy. Automation is capping wage growth. Customer support, for example, is well on its way to being automated. Next up we’ll see bookkeeping, compliance and even legal work increasingly handled by machines. Softer inflation gives the Fed room to cut more than Wall Street expects.

This is a big tailwind for dividend payers. And while this lower-rate process plays out, REITs will become increasingly popular.

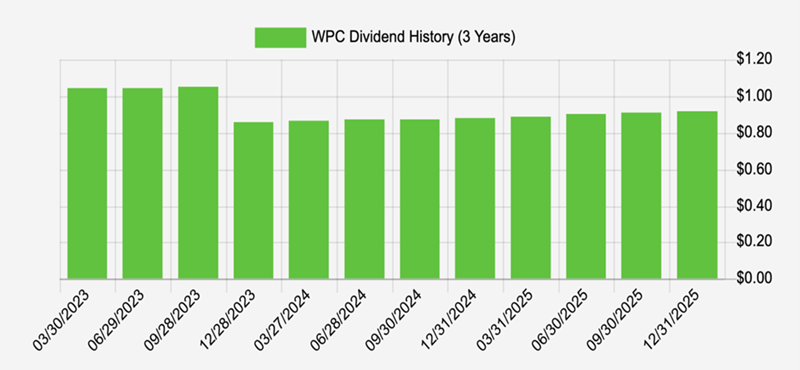

This wind is pushing the sails of W.P. Carey (WPC), a dog-house REIT the market is starting to forgive. In late 2023, management did the one thing income investors hate: they reset the quarterly dividend to $0.86. Vanilla investors saw one word—“cut”—and hit sell.

But that headline missed the real move. WPC wasn’t really trimming a payout. It was shipping out its biggest headache: office exposure.

WPC spun off 59 office properties into a separate REIT—Net Lease Office Properties (NLOP). Shareholders received 1 share of NLOP for every 15 shares of WPC. A clean break that put office risk in its own box and brought WPC back to its core of industrial, warehouse and essential retail net leases.

NLOP was a creative way to beat the bear market in office space. It wasn’t run like a “forever dividend” stock. NLOP packaged and sold its office assets methodically, sending cash back as properties were monetized.

And in the last few months, NLOP did exactly that—declaring special cash distributions of $4.10, $5.10 and $6.75 per share (paid in December, January and February). That’s nearly $16 per NLOP share in a short window. On the original spin ratio, that’s about a buck per WPC share in real cash that vanilla investors ignored while they sulked about the “cut.”

WPC’s rent checks aren’t static—over 99% come with contractual increases. These rent escalators are simply annual lease increases that are baked into contracts.

Meanwhile, the original WPC is back in growth mode. In 2025, it closed a record $2.1 billion of investments at an estimated 9.2% average yield as rent escalators kick in. That’s exactly how to set up a net-lease REIT for a rate-cut cycle: lock in high yields today, then enhance returns by borrowing at lower rates.

With a 97% occupancy rate and an office-free portfolio, WPC is quietly cooking while the market is still stuck on 2023.

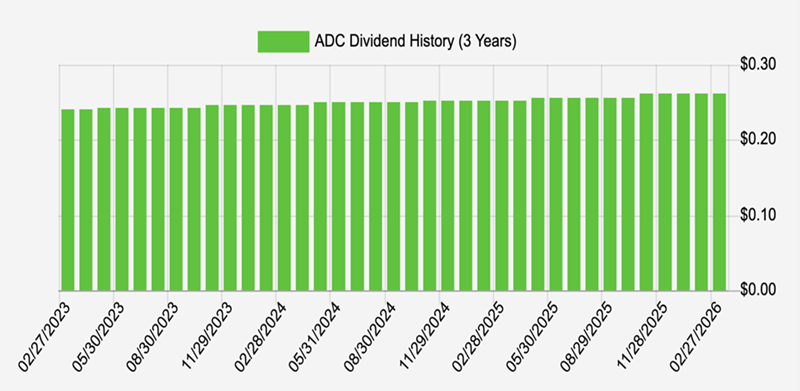

Some net lease REITs even pay monthly. You probably know Realty Income (O), “The Monthly Dividend Company.” Well, 4.2% fortress Agree Realty (ADC) also pays monthly, and it has a reputation for a sharper portfolio of high-quality tenants, newer properties and a more conservative balance sheet than Realty Income.

ADC’s portfolio is built around investment-grade, necessity-based retailers like Walmart, Home Depot, Tractor Supply. These are recession-proof and, frankly, Amazon-proof. People still need groceries, hardware, and “fix it yourself” supplies even when the economy gets shaky.

But Agree’s secret weapon is one most investors don’t understand:

ground leases. A ground lease is still a lease contract, but Agree owns the land and the tenant owns (and maintains) the building.

In many cases the building is net-leased too—meaning the tenant pays the expenses—so Agree just collects rent on the dirt. If you want low-drama real estate cash flow, it’s hard to beat owning the high-traffic corner “dirt” while someone else worries about the roof.

And this soil strategy is growing quickly. As of year-end 2025, Agree’s ground leases grew to about $75 million of annualized base rent, representing over 10% of the REIT’s annualized base rent.

This is meaningful safety. Dirt doesn’t get disrupted by e-commerce.

Agree has also been buying aggressively. In 2025, they acquired 305 retail net-lease properties for about $1.44 billion, at a weighted-average cap rate around 7.2%, with an average remaining lease term of about 11.5 years.

Management expects to invest $1.5 billion in 2026, continuing its game of “Net-Lease Monopoly.” Agree is stacking long leases and quality tenants, compounding its rent checks into a bigger board.

These two dividends, at 5.2% and 4.2% respectively, are modest by our (lofty) standards. But the total-return setup is attractive. Money market yields are falling. With cash sliding from 5% towards 3% as the Fed cuts, income investors are rotating out of cash and back into dividend payers. That’s when net-lease REITs not only pay but also tend to rise in price.

While I like the fact that Agree pays monthly, its 4.2% yield is simply too low to qualify as a monthly dividend superstar. I reserve that honor for stocks and funds paying 11% annually—like these three.

Recent Comments