As contrarians, we love it when a solid dividend grower drops on headline-driven fear.

And I see the recent decline in shares of Visa (V)—a Hidden Yields holding that hikes its payout double-digits yearly—as our next opportunity to cash in as the mainstream crowd frets.

You probably know that the stock fell on President Trump’s talk of limiting credit-card interest rates to 10% for one year. Investors, in typical “knee jerk” fashion, swiftly sold off this reliable payment toll booth.

That’s too bad for them—but it’s great for us. We now have a chance to buy a stout dividend grower at a bargain.

Visa’s Misunderstood Business Model

Investors often confuse Visa with a bank or other lender, but it’s not: Visa—and “duopoly” partner Mastercard (MA)—do not make loans to cardholders.

Instead, the company operates the payment “plumbing”: Visa’s network is active in 220 countries and processed 329 billion transactions in the year ended September 30.

That’s why we recommend the stock in Hidden Yields: It collects a “toll” on each of those 329 billion (and growing) swipes, taps and clicks. It’s a resilient business if there ever was one. That alone helps hedge it from any fight over card rates.

Visa Is Already a Bargain

Rate-cap talk aside, this stock is already cheap by two key measures.

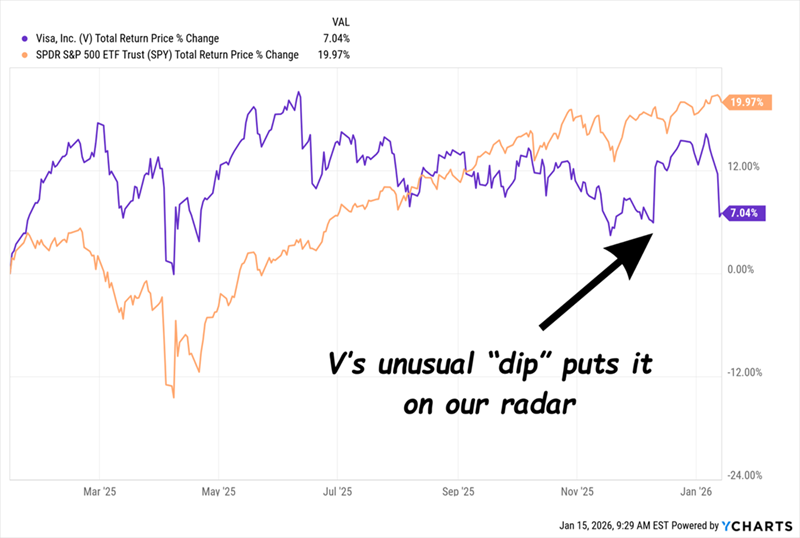

Bargain Signal #1: Visa Lags the Market

As you can see in purple above, Visa stock has lagged the S&P 500 in the past year, up just over 7%, compared to the market’s 20%. That’s unusual for a stock that’s outperformed the S&P 500 over the last decade.

This recent lag alone will make V stand out to investors—particularly those looking to rotate out of pricey tech stocks.

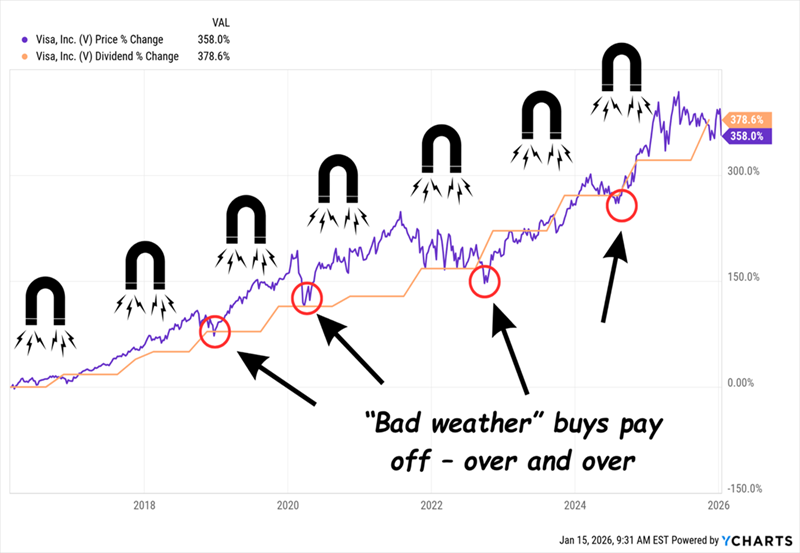

Then there’s the fact that the company’s share price is lagging its (surging!) dividend:

Bargain Signal #2: Visa Lags Its Payout Growth

The “Dividend Magnet” effect is clear here. Those big hikes—the last one, paid December 1, was 13.6%—are why Visa’s current yield is always around 0.5%. Every time management hikes the payout, investors bid up the stock in response.

You can also see that anyone who bought “bad weather moments” like this (times when Visa’s share price fell behind its dividend growth, in other words) did very well indeed.

And this stock still has plenty of upside, starting with American consumers.

Despite the gloomy headlines, they’re still spending. In November, retail sales jumped 0.6%, topping expectations. And even though it’s down 25% from a year ago, the University of Michigan’s consumer-sentiment indicator rose for the second straight month in January.

Both point to more transactions, and more “tolls,” for Visa in 2026.

“Stablecoins” the Next Big Growth Driver

As we discussed last month, Visa is also setting up to profit from the growth of “stablecoins.” Unlike other cryptocurrencies, stablecoins are pegged to the US dollar.

That’s key because it makes them ideal for international transactions, as they get around pokey, high-fee wire transfers.

By moving into stablecoins, Visa is essentially building the bridge between traditional payments and regulated stablecoin settlements in USD.

In December, the company launched stablecoin settlement in the US—this is behind-the-scenes, bank-to-bank money movement (subject to Visa’s fee, of course!) that happens after you tap your card.

This business is growing quickly. As of November 30, Visa’s monthly stablecoin settlement volume had already reached a $3.5 billion annualized run rate. The “digital dollar” pipes are live in the US. Now that they work, volume can scale fast. The tolls are now being collected.

As more banks and fintech companies issue stablecoins, this number will only grow. Think of a stablecoin like a casino chip, except it’s digital. Inside the “casino” (the stablecoin network), it behaves like money. It’s fast, secure and easy to move. But you still have to get in (swap dollars for stablecoins) and get out (convert back to bank money) when you want to spend in the normal world.

Visa is positioning itself as the cashier’s cage. It’s the bridge that makes these digital dollars usable everywhere.

Management Knows This Stock Is Cheap

Fear of a recession has kept Visa stock capped in the last year, and the latest selloff has added to our opportunity.

Management knows this. In 2025, they dropped $18.2 billion into share buybacks, and they’ve repurchased 9% of the company’s float in the last five years. Buybacks enhance earnings per share (by extension supporting the share price) and boost the dividend, leaving fewer shares on which Visa has to pay out.

A “Fortress” Balance Sheet

Finally, even if Visa were a lender, its strong balance sheet, with $23.2 billion in cash and investments, just a tad shy of its $25.9-billion debt, gives it a strong cushion here.

So on a net-net basis, Visa is essentially debt-free. That gives it plenty of room to weather any storm and keep its dividends (and buybacks) growing. Let’s buy now, before the crowd figures out the true value of this payout-popping “toll booth.”

Visa’s “Dividend Magnet” Always Prevails. Here Are 5 More Winners

I think the chart above is clear: Those who buy Visa when the stock falls behind its dividend payout—as it is now—get an excellent shot at big “bounce-back” gains.

That’s not only true of Visa. I’ve seen this profitable “Dividend Magnet” pattern play out with other stocks over and over again.

The key is to buy dividend payers whose payouts are not only growing but accelerating. After all, the bigger the hike, the more other investors notice—and send those share prices skyrocketing.

We want to be in before that happens—and I’m going to help you do that.

Our play? Five stocks with the most powerful Dividend Magnets I’ve ever seen—and, critically, the financial strength to keep those payouts growing.

I’ll tell you more about all five of these off-the-radar dividend plays here—and give you a free report revealing their names and tickers. Make sure you get in now, before they announce their next big payout hike.

Recent Comments