Today we’re going to talk about a subject that might seem a little outside the dividend plays we normally discuss.

But as you’ll see, this topic—a big shift in how Americans feel—is the main reason why some of our favorite high-yielding closed-end funds (CEFs) are woefully underpriced, like one equity-focused 9%-yielder with an incredible track record.

Let’s start with that unlikely topic: Happiness. It matters because, as we’ll see, how happy Americans are ties directly into investing behavior in very predictable ways.

Source: CEF Insider

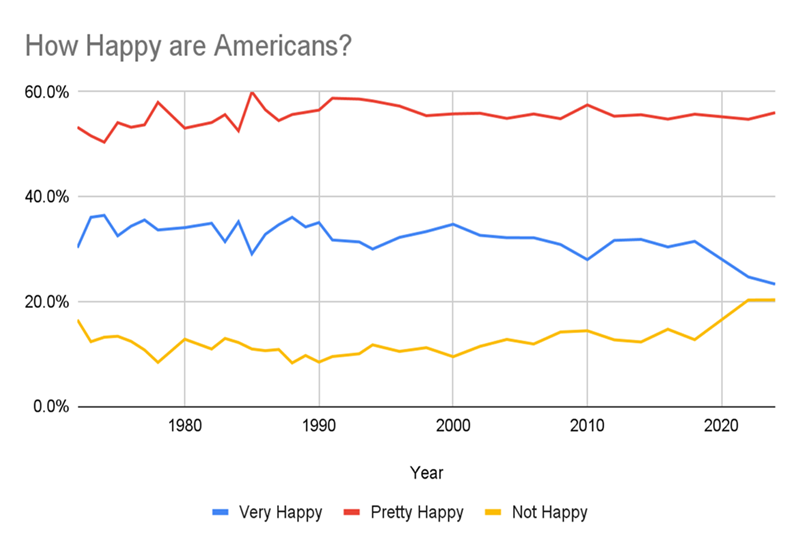

This chart shows the results of the General Social Survey, from the University of Chicago’s National Opinion Research Center. It’s one of the oldest studies of Americans’ views on different social, political and cultural issues.

When asked “How happy are you?” the majority feel pretty happy. That’s been true since the survey started asking this question in 1972.

But look at the yellow line, showing how many Americans are not happy. It reached a new high in 2022 and is stuck there. Similarly, the percentage who are “very happy” has fallen to a new low and is trending further down.

If these trends continue, the percentage who say they’re unhappy will climb above those who are very happy for the first time in history. That’s a big psychological shift, and markets haven’t caught on to it yet.

Consumers Get the Blues

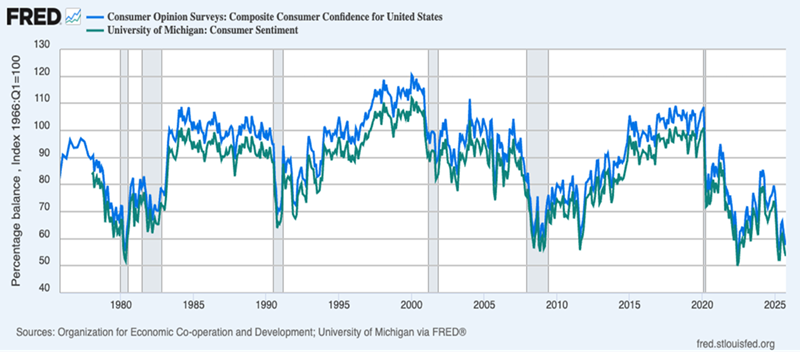

Now let’s get into why this trend is a financial risk. This chart is our first stop.

Here we have two measures of consumer confidence, one from the University of Michigan (in green) and one from the OECD (in blue). As you can see, these tend to drop during recessions (the gray sections above) and rise after, which makes sense.

There are exceptions, like in 1992 and in 2011, when consumer confidence cratered following the recessions that preceded them. Back then, consumers clearly worried that recent bad times would return.

But we’re now five years out from the last recession, and consumer confidence is stuck below where it was even during the pandemic! In other words, people feel worse about the economy now than they did when they were literally in quarantine.

That’s strange, and it demands a closer look because, at least economically, it makes no sense. Unemployment is much lower than it was during the pandemic and remains historically low. Incomes and wealth are rising, breaking trends that lasted two generations, as we’ve recently discussed.

So we’re left with one conclusion: People are just more miserable than they used to be, and it’s causing them to respond more negatively to surveys than they used to.

This makes sense, since the pandemic’s aftermath sent inflation soaring and AI has boosted worries about many things, including job loss.

The Data Has Changed. Wall Street Hasn’t

This all matters because people who make major economic decisions rely on data like this. I know because I spent over a decade consulting with hedge funds and investment banks on how to create just these sorts of studies.

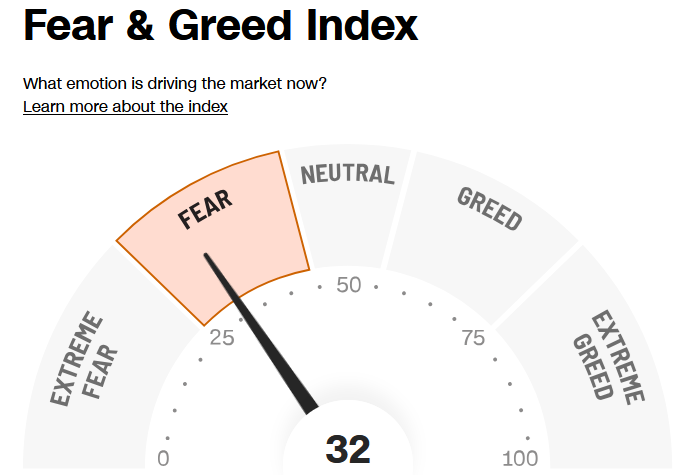

This ties into our income (and portfolio value) in two ways. First, a lot of survey-driven research is less reliable than it used to be—including the oft-cited CNN Fear & Greed Index.

Source: CNN.com

For a while now, it’s been saying that investors are fearful. But if so, why have stocks climbed to near all-time highs? This index clearly needs adjusting, because what counts as “fear” is now a lower number than it used to be.

As a result of this shift, negative attitudes are no longer useful indicators of when a selloff will start.

Of course, this also means that when the market sells off because everyone’s worried that attitudes are souring, we contrarians get a chance to profit. Consider how the market tanked in 2022 because most investors expected a recession, but then no recession came. Or how tariff worries sent markets into freefall in April, but nothing major has happened since.

Selling because the market is getting fearful doesn’t work anymore, but buying when the market has whipped itself into a frenzy does.

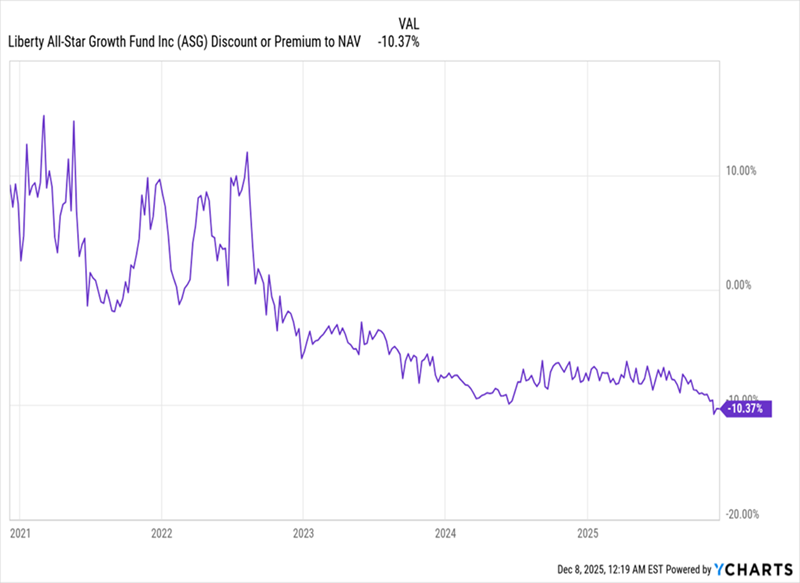

ASG: The Poster Child for Our New Pessimistic Era

We see this playing out with CEFs, where discounts to net asset value (NAV) are deeper because risk-averse investors, who tend to be most interested in CEFs, pull back when sentiment sours. A broad drop in happiness, then, can make them more cautious, sending CEF discounts to deeper levels than the fundamentals justify.

As a result, the Liberty All-Star Growth Fund (ASG) has seen its discount drop below 10% in 2025, far below the last decade’s average of a 2.2% discount. That’s despite the fact that ASG has earned a 10.2% annualized return in that time and yields 9% today.

It’s a CEF Insider holding I talk about a lot because, despite the “growth” in its name, it pays us that 9% dividend (which does move around a bit, as it’s tied to the fund’s NAV). ASG also holds a nice mix of large- and mid-cap stocks. Top holdings range from Apple (AAPL) to New York State retailer Ollie’s Bargain Outlet Holdings (OLLI).

Eventually, history suggests that CEF investors will realize we live in a new era where sentiment is lower than it used to be, simply because these are more pessimistic times.

At that point, they’ll likely see that these discounts have gotten too wide and bid them up. If we buy ASG today, we’d be nicely positioned to beat them to the punch—and collect that rich dividend while we wait for this to happen.

5 Funds. 60 Dividend Checks a Year. A 9.2% Yield. Now Is the Time to Strike

The line above says it all. When you pick up the 5 funds I’m urging all investors to buy in this moody market, you lock in an average yield of 9.3%. What’s more, these 5 funds’ dividends come your way every month.

That adds up to 60 dividend checks every single year.

It sure beats stocks, which pay quarterly and yield a pathetic 1%. It crushes Treasuries, too. And with today’s overly gloomy sentiment, these 5 monthly payers are deep in the bargain bin.

Grab them now and you could collect your first payout within weeks.

Recent Comments