The stock market is currently caught up in its deepest slide since July. We contrarians are prepared to move quickly for deep-dip-buying opportunities.

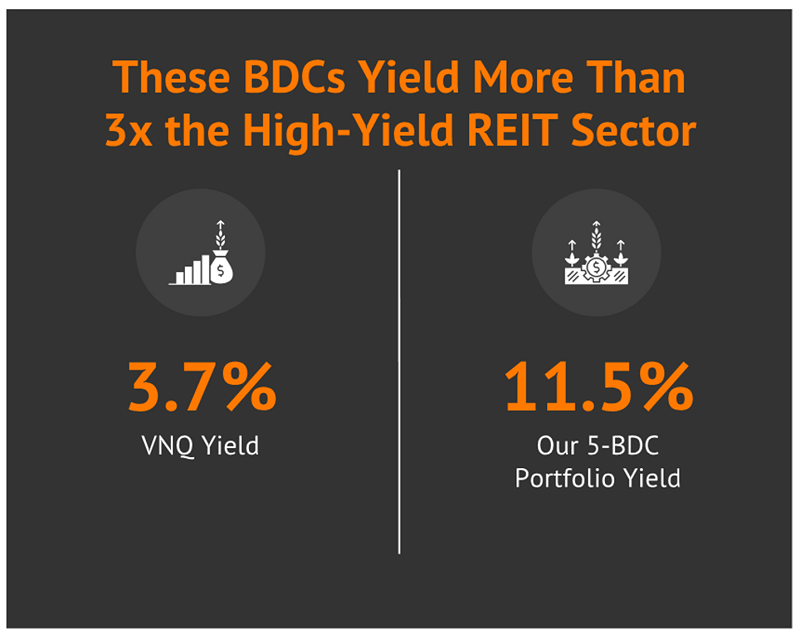

Right now, I’m paying close attention to already-high-paying corners of the market, where we can get 9.4% to 13.1% yields right this very minute. I’m talking about from the business development company (BDC) industry, where those sky-high yields aren’t rare—they’re the norm. In fact, right now, if we threw darts at a board of BDCs, we’d be likelier to hit a double-digit payout than one in the single digits.

But it’s not just the yields I love—it’s the access.

BDCs are an “average Joe’s backdoor” into the world of private equity and private credit.

Many small and midsize businesses would love to get funding from traditional banks. But those banks don’t want the risk—so they either refuse to lend to smaller companies, or charge interest rates that would make a loan shark blush.

That gap is commonly filled with private equity and credit—investment opportunities that the median investor simply doesn’t have the money to participate in.

However, with just $30 or $40, we can buy shares in publicly traded BDCs, which tend to invest in dozens or hundreds of private companies.

Said differently: We can invest like private equity for the price of a couple Chipotle burritos.

Right now, I want to look at five yielding up to 13.1% that have been acting extremely well so far in 2025. And if we just so happen to get a temporary dip in these BDCs on additional pain in the market, all the better.

FS KKR Capital (FSK)

Dividend Yield: 13.1%

FS KKR Capital (FSK) provides financing to 214 private middle-market companies spread across two dozen industries, including significant exposure to software and services, commercial and professional services, capital goods, and health care equipment and services.

While it prefers to deal in senior secured debt, it will also deal in subordinated debt, asset-based finance, preferred equity and plain ol’ equity. Of its debt investments, roughly 90% is floating-rate, though the 10% of fixed-rate debt should help it a little should the Fed begin cutting rates again.

Also, roughly 10% of FS KKR’s investments are tied up in Credit Opportunities Partners JV, a joint venture with South Carolina Retirement Systems Group Trust that invests capital across a range of investments.

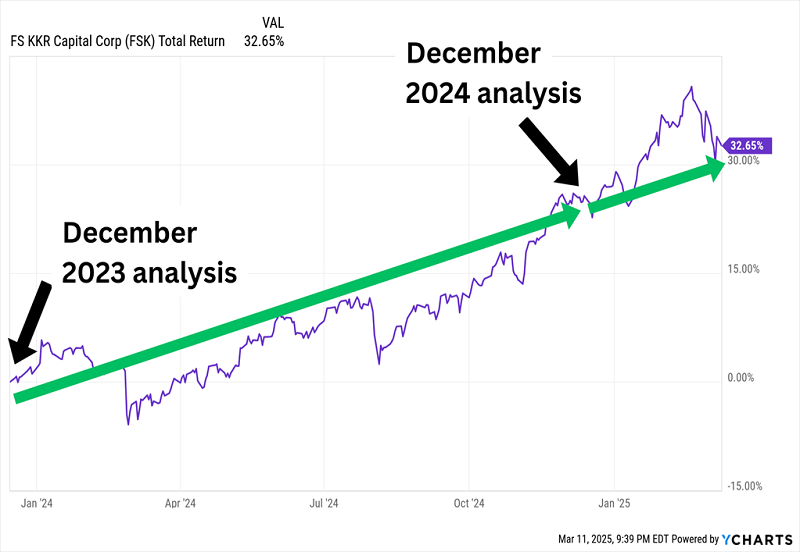

I’ve highlighted FS KKR a few times over the years. In December 2023, I said:

FSK hasn’t historically given investors much to cheer about, but there are several things to like. A double-digit yield, sure, but also a healthy, well-covered payout, a growing streak of bottom-line beats, and a comically deep 21% discount to NAV.

Then more recently, in December 2024, I noted that while FSK wasn’t attractive as it was in 2023, a still-deep 10% discount to NAV, declining non-accruals (loans that are delinquent for a prolonged period, usually 90 days), and decent dividend coverage were reasons to give it a closer look.

FSK: So Far, So Good!

The dividend still looks fine—FSK says it expects to pay $2.80 per share in dividends this year, split between its 64-cent quarterly regular dividend and supplementals. That would put it level with 2024 (backing out the two 5-cent specials it also paid last year).

However, non-accruals actually grew during its most recent quarter, to 2.2% at fair value from 1.7% in the quarter prior. While FSK wrote off Miami Beach Medical Group, two companies were added. Meanwhile, FSK’s gains in 2025 have partially come from a further narrowing of its discount to net asset value (NAV), which now sits at just 8%.

Sixth Street Specialty Lending (TSLX)

Dividend Yield: 9.4%

There’s a lot to love about Sixth Street Specialty Lending (TSLX).

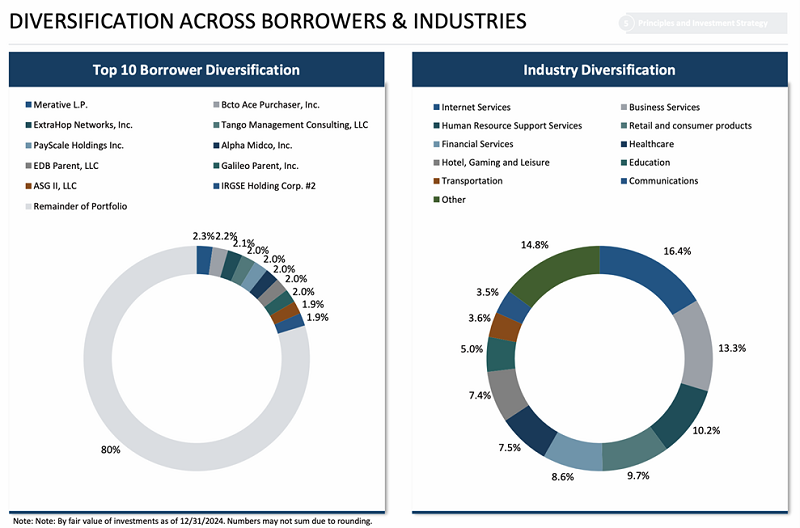

Sixth Street is a flexible provider of funding to middle-market companies, dealing in senior secured loans, mezzanine debt, non-control structured equity and common equity. It prefers transactions of between $15 million and $350 million, with companies at $50 million to $1 billion in enterprise value generating $10 million to $250 million in annual EBITDA.

TSLX’s portfolio currently sits at 115 companies ranging from exciting names like gen-AI provider Sprinklr and human resources support services firm Payscale, to also challenged retailers such as Staples and Bed Bath & Beyond.

One of Sixth Street’s classification systems divvies the business up into 16 “sector franchises,” which really are a blend of sectors, industries, and strategies—for instance, they include “Growth,” “Sports, Media, Entertainment & Telecom” and “U.S. & European Direct Lending.”

Its more traditional industry breakdown is a lot easier to understand:

Source: Sixth Street Specialty Lending Fixed Income Presentation, March 2025

In short, this BDC covers a lot of ground.

Sixth Street is up 6% year-to-date, which is better than the BDC average. No surprise there. I’ve noted multiple times that TSLX is a well-managed BDC, and that continues to be the case. In its most recent quarter, adjusted NII topped Street estimates, non-accruals just dropped from 1.9% at fair value to 1.4% in the most recent quarter, and its estimate for $1.97-$2.14 in adjusted net investment income (NII) implies that its dividend should continue to be decently covered.

Speaking of which: Sixth Street also works within a base-and-supplemental dividend system. Last year, it paid $1.84 per share in regulars, and another 24 cents per share in supplementals. While this kind of system can be murder for investors who actually need income, we’re getting more than 8%—my preferred baseline of retirement income—from the regular dividend alone.

But boy, are we paying for it. TSLX is one of the most expensive BDCs on the market, trading at a whopping 29% premium to NAV at current prices.

Trinity Capital (TRIN)

Dividend Yield: 13.0%

The same can be said about Trinity Capital (TRIN), which demands a high price for its alluring business model.

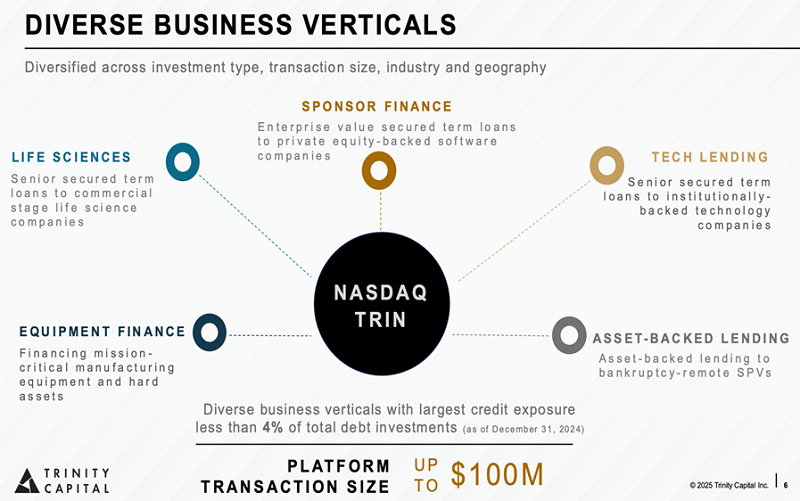

Trinity has built itself a niche as a venture-debt firm that deals almost exclusively with growth-stage companies. Its business is broken up into five verticals, shown here:

Source: Trinity Capital Q4 2024 Investor Presentation

It’s hardly an even distribution across those verticals, though. At fair value, 75% of its investments are loans, 18% is equipment financing, and the remaining 7% is equity and warrants.

Trinity Capital’s roster is filled with bleeding-edge companies dealing in health wearables, fintech, and medication analytics. Its equipment financing portfolio companies are perhaps the most interesting, including names like launch service and spacecraft component provider Rocket Lab, as well as Athletic Brewing, which is riding the rise of non-alcoholic craft beers.

Despite its growthy focus, though, TRIN’s management has been able to whittle down hype and find real substance. Non-accruals are typically low, and sit at a razor-thin 0.8% at fair value right now. It’s also positioned well for a declining-rate environment—only 77% of debt is floating-rate, and of that, 43% of its positions are at the floor.

Dividend coverage is often tight, however, and Trinity doesn’t use supplementals—the entirety of its 13% yield is on its quarterlies, which means owners need to keep close watch on NII.

I’ve also previously written that this growth profile hasn’t really filtered down into performance, with Trinity mostly just producing industry-average results with more volatility. Well, on the one hand, TRIN has come alive of late, delivering a fat 11% total return so far this year. Much of that stems from an expansion of its premium to NAV, which has ballooned from 9% in December to 18% today.

CION Investment (CION)

Dividend Yield: 12.7%

I won’t spend much time on CION Investment (CION) because I covered it at my recent look at small caps with monster yields. But it still warrants a mention here given both its strength and outrageous discount.

CION Investment is an externally managed BDC that targets companies with annual EBITDA between $25 million and $75 million. Its 103 portfolio companies are spread fairly evenly across numerous industries, including business services, healthcare/pharmaceuticals and media.

CION has delivered an 8% return year-to-date to easily beat the industry average, and yet it’s still trading at a deep, deep 23% discount to NAV.

This BDC Wiggles More Than Most, But Lately, That’s a Good Thing

One thing I was pleased to see in its just-announced fourth-quarter earnings was a reduction in non-accruals. Back in Q3, non-accruals were 1.9% at fair value, which was higher than its BDC peers (1.4%). However, in Q4, that figure was reduced to just a hair above 1.4%, which is a step in the right direction.

SLR Investment (SLRC)

Dividend Yield: 9.5%

SLR Investment invests primarily in senior secured loans of private U.S. middle market companies, but it does have some specialties.

That sentence could be used to describe many BDCs, but SLRC does play in some specialty niches. Here’s a look at its portfolio as of the end of 2024:

- Cash-flow loans (traditional sponsor finance business): 21% of portfolio at fair value

- Asset-based loans: 34%

- Equipment financing: 37%

- Life science loans: 7%

- Equity and Equity-Like Securities: 1%

The risk is extraordinarily spread out for a BDC, too. Its portfolio companies number almost 900 (!), which do business in 110 industries.

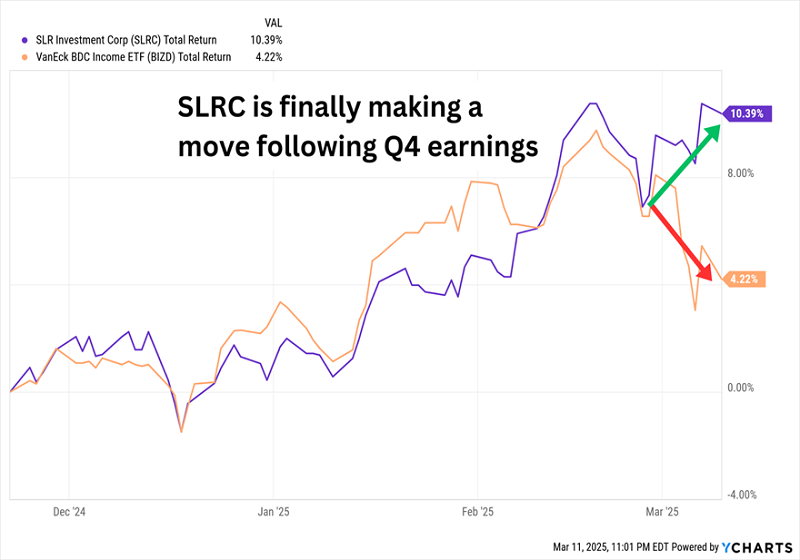

In 2024, I highlighted SLR Investment as a company that Wall Street just does not like—most of the analysts covering it call it a Hold or a Sell. That’s in part because the stock has largely trailed the industry for some time, but shares finally came to life in late February after the BDC’s quarterly report.

SLRC’s Earnings Jump: The Start of Something, Or a Short-Term Disconnect?

However, one of the most common analyst complaints is “earnings clarity.” SLRC has been acquiring more specialty finance portfolios, and the pros just aren’t sure how they’re going to pan out. Also, despite a good chunk of fixed-rate investments (39%), there’s still a lot of question as to how this BDC would be able to absorb further rate cuts.

Unfortunately, investors are less incentivized than normal to test the waters. SLRC’s recent burst has closed its NAV discount from double digits just a couple months ago to a mere 5% now.

But it’s possible that the pros are too negative on the name. I’ve previously pointed out that SLR Investment has trailed the industry for some time, but that track record is at least improving on the back of better-than-expected quarterly results. And SLRC shares do offer a 10% yield at a 10% discount to NAV.

How to Collect a $48,000 “Portfolio Paycheck” When You Retire

SLR Investment also disappointed investors near the end of 2023 by “downgrading” its dividend from monthly distributions to the Wall Street-standard quarterly dole.

Don’t get me wrong: SLRC has exactly the level of income we want.

But I’d prefer to get it from more stable businesses—and I’d prefer to receive them monthly.

That’s exactly why I’ve built the “8%+ Monthly Payer Portfolio”: A who’s who list of companies and funds that check off the “3 H’s”:

- High yields

- High quality

- High durability

A lot of dividend portfolios try to offer up names that you know, and that you’re comfortable with. But Wall Street’s over-trodden blue chips tend to deliver relatively modest yields at high valuations … not to mention, they always pay quarterly.

My 8%+ Monthly Payer Portfolio is filled with names that many investors have (wrongly) slept on—despite kicking out 8%+ dividends that roll our way each and every month.

That dividend schedule means when you’re done collecting a regular workplace paycheck, you can quickly transition to collecting a regular “portfolio paycheck” of roughly $48,000 annually on just $500,000 invested—and that paycheck will still sync up with your monthly bills!

Don’t miss out on these terrific income plays while you can still get in at a bargain. Click here for all the details, and to download a FREE Special Report revealing the names and tickers of all the stocks and funds in my 8%+ Monthly Payer Portfolio.

Recent Comments