Last week’s oil-price drop has set us up to buy some top-flight energy dividends on the cheap. We’re going to grab one with a “hidden” 10.3% yield in just a moment.

First, this buy window goes well beyond a dip in the price of the goo. Fact is, oil dropped because things calmed (slightly) in the Middle East.

But of course, that can change again, and quickly. The real oil story for us is that the drop (along with a double-digit decline in natural-gas prices since the start of October) is happening as energy demand is set to rise.

So desperate is the need for energy these days that Big Tech is turning to long-shuttered nuclear reactors. Microsoft (MSFT), for example, recently signed a deal with Constellation Energy (CEG) to restart a reactor at Three Mile Island—site of America’s worst nuclear accident, in 1979—to generate the power needed to satisfy AI’s voracious appetite.

Meantime, I continue to believe that a “no-landing” setup is increasingly likely here in the US, in which the economy keeps humming along but inflation comes back.

Not great, I know. But the fact is, when the Fed hikes rates, it usually does so until it breaks something—the main example being Paul Volcker, who was so determined to break inflation’s back that under his watch, the federal funds rate hit 22% (!).

Inflation was crushed, but the hike sent the US into a deep recession, with unemployment soaring to 11% in 1982.

Jay? He “broke” a couple marginal banks that were circling the drain anyway.

But that was enough to cause him to blink and pump liquidity into the system through the “back door” while continuing to talk tough on rates, as this chart of bank reserves clearly shows:

Meantime, as we’ve written about previously, government deficit spending is completely out of control.

It is possible, perhaps probable, that Uncle Sam will overwhelm Powell. For fiscal 2024, the Congressional Budget Office (CBO) projects a $1.9 trillion deficit on $4.9 trillion in tax receipts. (And yes, this is the CBO that paints its projections with rose-colored ink.)

So we have nearly $5 trillion in revenues and almost $7 trillion in expenditures.

A 40% overshoot.

That $2 trillion is a big reason why the economy remains strong (the latest evidence: last week’s better-than-expected retail sales report and lower than expected jobless claims). But the resulting monetary inflation could flow back into consumer price inflation.

Then there’s China, which joined the stimulus party a few weeks back, when its central bank rolled out a sweeping set of stimulus measures.

The PBoC lowered interest rates (including mortgage rates) and announced “stock market support” plans to help companies buy back their own shares and to allow investors to borrow against their portfolios.

Shares of Chinese firms, as well as resources like copper, popped. And while it will take a while for the PBoC’s moves to work through the economy, they’ll likely boost energy demand, too.

This Refiner Is in the “Sweet Spot,” Sports a 10.3% Yield No One’s Noticed

This is a perfect setup for refiners like Phillips 66 (PSX), since they’re paying less for their main raw material (oil) these days, while demand for their finished products (gasoline, diesel and home-heating oil among them) look set to gain.

Investors often misunderstand refiners, confusing them with oil and gas producers. And when they do bother to pay attention to these stocks, it’s usually in the spring, ahead of the summer driving season. (PSX has some 7,260 gas stations in the US and 1,670 outside America’s borders.)

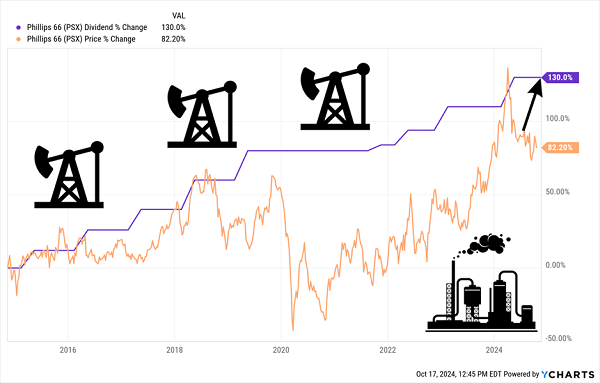

That’s too bad for the mainstream crowd, because they’re missing a window on a stock that’s sent its payout up a stout 130% over the last decade, with the only pause coming during the pandemic dumpster fire:

PSX “Refines” Cheaper Crude Into Big Payouts

As you can see, the firm’s share price has struggled to keep up with the surging payout. But I expect that gap to close as PSX’s Dividend Magnet (or the tendency for share prices to track payouts over time) kicks in.

Moreover, while we collect that payout, and get ready for more hikes, seasonal demand will swing back PSX’s way as we move through the colder months.

The kicker here is that management is all-in when it comes to rewarding shareholders. In addition to its strong payout growth, Phillips 66 is a big repurchaser of its stock—having taken some 23% of its outstanding shares off the market in the last decade.

That matters because those buybacks make per-share indicators like earnings per share, free cash flow per share and dividends per share look better. That supports share prices.

About That “Hidden” 10.3% Yield

That tees up the last thing I want to talk to you about today: shareholder yield.

Wait, shareholder what?

We know from the free screeners out there that PSX’s current dividend yield is around 3.5%. Simple, right? But shareholder yield goes further and includes the value of dividends and buybacks to us.

To calculate it, we take the amount spent on buybacks over the last 12 months, minus any cash brought in through share issuances, plus the amount spent on dividends. We then divide the total by PSX’s market cap, or the value of all its outstanding shares.

For PSX, the difference between the dividend yield and shareholder yield is dramatic: For the 12 months ended June 30, PSX spent $1.855 billion on dividends and a whopping $3.909 billion on buybacks, with $175 million in share issuances, which we’ll go ahead and subtract.

Divide the $4.014-billion total by PSX’s $55.71-billion market cap (as of this writing) and you get a sweet 10.3% shareholder yield.

PSX’s shareholder-friendliness is another reason why I see investors moving to this stock, especially as interest rates fall and economic growth—and energy demand—rise.

PSX’s Stock Is a Pressure Cooker Waiting to Pop. Here are 5 More.

The oil-price dip, Jay’s premature rate cuts and PSX’s share-price growth, which lags its surging payout, work together to put upward pressure on the share price. This stock will pop and catch up to—and likely shoot past—the payout.

And we’ll be here for it!

I’ve seen it time and time again—it’s why I call this phenomenon the Dividend Magnet. It’s at the heart of the stock-picking I do for my Hidden Yields dividend-growth service.

I’ve targeted 5 MORE dividend growers I see as primed for big gains in the coming months, and they ALL show the same pressure-packed “stock-price lag” as PSX.

BTW, if you want to avoid the volatile energy sector I get it: It’s why I pulled these 5 payers from across the economy: sectors like utilities, technology and recreation. These are all sectors I see as winners in the “no-landing” scenario ahead.

The time to buy these 5 stout dividend growers?

Right now, before the rest of the crowd drives their share prices back above their dividends. Click here and I’ll tell you more about these 5 “payout-powered” winners and give you a free Special Report revealing their names and tickers.

Recent Comments