I know it goes without saying that we’ve all loved watching our dividend stocks skyrocket this year. But October—as always, it seems—has amped-up the volatility.

The end of the year looks choppy, with a widening war in the Middle East and a contentious (to say the least!) election on tap here at home.

That makes now the time to sell any flawed dividends you may hold “on the rip.” We’ll break down one of these losers below. It’s the kind of stock that’s gone nowhere for so long that you may even have forgotten you own it!

But we’re not just going into a defensive crouch here, because despite the market run-up, there are still some cheap dividend growers on the board.

The sweet “pick-and-shovel” play we’ll talk about a little further on, which has spiked its payout an incredible 590% in the last decade, is a prime example. It’s unloved now, but it’s in the driver’s seat as central banks in China and the US turn dovish.

Let’s get started by dumping that first stock I mentioned, then rolling our cash into that sweet, growing “stimulus-powered” divvie.

Nordstrom Is as Good as It’s Going to Get. Sell Now …

Nordstrom Inc. (JWN) yields 3.5% as I write this, which is okay—it’s almost triple the sad 1.2% yield on the typical S&P 500 stock.

But I worry its business model is obsolete in a world where e-commerce continues to surge: The company runs department stores—93 Nordstrom outlets and 269 Nordstrom Rack discount stores, as of the end of the second quarter.

The other worry with Nordstrom: Debt. It’s carrying $2.6 billion in long-term debt, and even though it’s been paying that down, its current obligations are a high 72% of its market cap, or value as a public company.

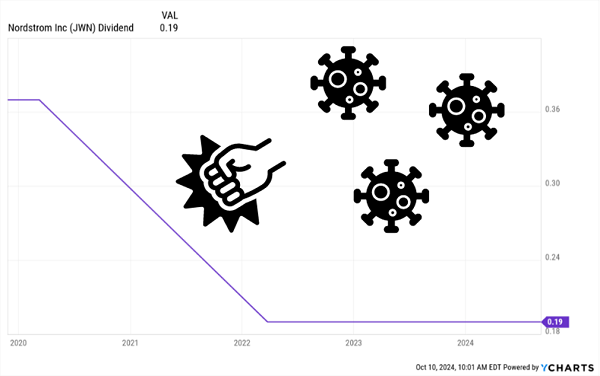

That weighs on Nordstrom’s ability to respond to rising competition from e-retailers and more specialized stores. It also cuts the odds of a hike to the dividend, which was suspended in 2020 and reinstated in 2022, though at just over half the previous rate:

COVID KO’ed Nordstrom’s Dividend—and It’s Still on the Mat

Worse, JWN devoted 91% of its free cash flow to dividends in the last 12 months, which is just not sustainable in the long run.

Despite all this, the company is charging ahead with expansion. By the fall of 2025, it plans to open 32 new outlets (11 of which are already open).

That’s a risk in the highly competitive retail market, and bear in mind that this company doesn’t have the best record of expansion. Witness its ill-fated move into Canada, which started with its first store, in Calgary, in 2014, and ended when it shuttered its last Canadian outlet in 2023.

Thanks to the broader market rally, investors have bid JWN up about 18.5% year to date, to around $22. That’s way off the $82 highs it last saw 10 (!) years ago, but it’s the best we can hope for now. Take advantage of the market bounce to unload this one.

… And Buy FDX, Whose Planes Will Soar in a “No-Landing” Economy

Another knock on Nordstrom is that it’s an also-ran in e-commerce, far behind the likes of Walmart (WMT) and Amazon.com (AMZN).

And I know it seems like we’ve been talking about e-commerce growth forever now, but there’s a good reason why: It’s one of those quiet megatrends that’s continued to pop higher, year after year.

According to eMarketer, e-commerce sales will pass $6 trillion globally this year, and leap t0 $7.96 trillion by 2027. China is the biggest e-commerce market, at nearly $2.2 trillion in online sales in 2023, according to Statista. The US is No. 2, at $981 billion.

Our favorite way to play that growth isn’t by trying to cherry-pick which retailer will win at the online game. Instead, we’re going with a “pick-and-shovel” play that profits no matter what: FedEx Corp. (FDX).

(“Pick and shovel” refers to the California gold rush, in which the real winners were the merchants who sold the miners the picks, shovels and other supplies they needed—not the gold-panners themselves.)

I mention China and the US because I see big catalysts coming out of both that are great news for FedEx’s profits.

A Smart Play On “Dueling” US, China Stimulus

On the US side, we’ve got the rising possibility of a “no-landing” setup, something we’ve been talking about here on Contrarian Outlook for the better part of six weeks (and most recently last Tuesday)—though it’s only recently caught the press’s attention.

Here’s what I mean: Normally when the Federal Reserve hikes rates, it does so until it breaks something. That didn’t happen this time (with the exception of Silicon Valley Bank and a handful of other brittle lenders).

Now the Fed is in cutting mode, and while inflation has fallen, it remains stubborn, as last week’s CPI report showed.

Meantime, government spending is out of control, with expenditures outrunning the tax receipts by just under $2 trillion. And you and I both know that no matter who wins the election, that’s not likely to change.

Where does that leave us? Well, an “extra” $2 trillion will do a lot to keep an economy rolling! Too bad it also makes it likelier that inflation returns. Not great, I know. But a continually growing economy is great for FedEx.

And our Fed isn’t the only dovish central bank! A couple weeks back, the People’s Bank of China (PBoC) announced a sweeping set of stimulus measures.

The PBoC lowered interest rates (including mortgage rates) and announced “stock market support” plans to help companies buy back their own shares and to allow investors to borrow against their portfolios.

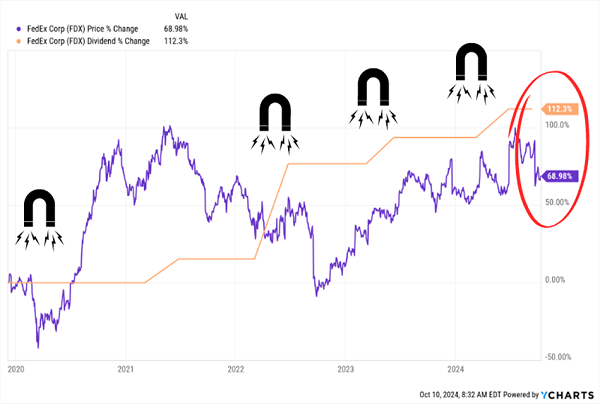

In this setup, FedEx benefits. The stock dropped on weak first-quarter profits in September, giving us a nice buy window. As I write this, FDX has some 40% upside from here, just to catch up with its ever-rising dividend.

FDX’s September Swoon Opens Our Buy Window

(If you’re a regular reader, you likely know about the Dividend Magnet—the tendency of stock prices to match dividend growth over time. This is why the current yield, or the yearly payout divided into the current share price, on your favorite stock never seems to change very much.)

The payout only yields 2% today, but we can consider that a “starter” yield on a buy made now, especially when you bear in mind that FDX has hiked its dividend an incredible 590% in the last decade.

Moreover, the divvie only accounted for 49% of the company’s free cash flow over the last 12 months, far less than Nordstrom’s worrying 91%. That shelters the payout from whatever might be coming, economy-wise, and sets the table for more growth, too.

5 Dividends That LOVE Volatility (October Is the Best Time to Buy Them)

History tells us that October is the most volatile month on the stock market. With the market still running hot, this means now is the time to purge your portfolio of peaking duds like Nordstrom.

As we discussed, the retailer’s outdated business model, high debt, and shaky dividend make it a stock to sell now.

Instead, we’re looking to the few oversold tickers still out there, like FedEx, with 40% upside potential and rising dividends.

It’s just the start. I’ve hand-picked 5 more dividends whose payouts are growing fast—and pulling up their share prices in lockstep. I call these cash-rich, reliable payers “Recession-Proof” dividends, and they’re “must buys” now, while they’re still cheap.

Click here and I’ll tell you more about them and give you my “dividend-powered” plan for profiting in bull or bear markets. I’ll also give you a free Special Report revealing these 5 stocks’ names and tickers.

Recent Comments