Normally when interest rates fall, we closed-end fund (CEF) investors are tempted to pick up a fund like the 7.3%-paying Royce Small-Cap Trust (RVT).

It seems like a particularly savvy move today, with this small cap–focused CEF trading at a 10.3% discount to net asset value (NAV, or the value of its underlying portfolio). Cheap!

But is that really a good value, or could RVT get cheaper still?

Let’s take a look, starting with small caps generally. Like large caps, they benefit as lower rates boost consumer spending. But there are two other factors that make falling-rate periods particularly advantageous for smaller firms:

- They mean lower borrowing costs for investors, allowing them to invest on margin more than they would otherwise. Small cap stocks, which tend to entail more risk than large caps, attract these more-aggressive buyers.

- They help companies spend more on expansion. This tends to benefit smaller firms more than bigger ones, as smaller companies tend to be more innovative.

With that in mind—plus the fact that small caps tend to be more domestic-focused, helping shield them from global instability—you’d think investors would’ve bid them to the moon this year, right?

Well, not so much.

Markets Sour on a Small-Cap Renaissance

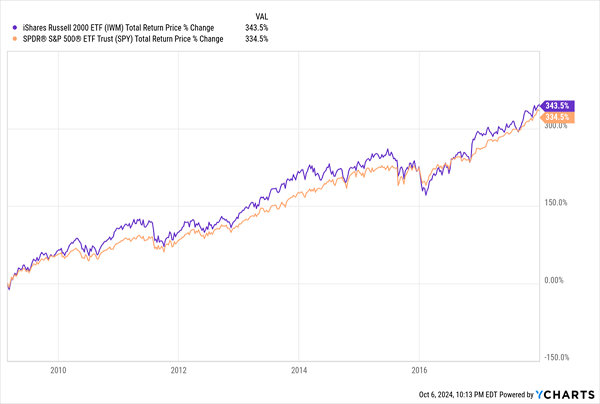

So far, traders aren’t calling for a small-cap rebound, with the iShares Russell 2000 ETF (IWM), in purple above, trailing the benchmark S&P 500 ETF (in orange). (IWM invests in all 2000 small caps that make up the primary US small-cap index, the Russell 2000.)

We normally love a contrarian setup like this at my CEF Insider service, but this time I think the herd has a point.

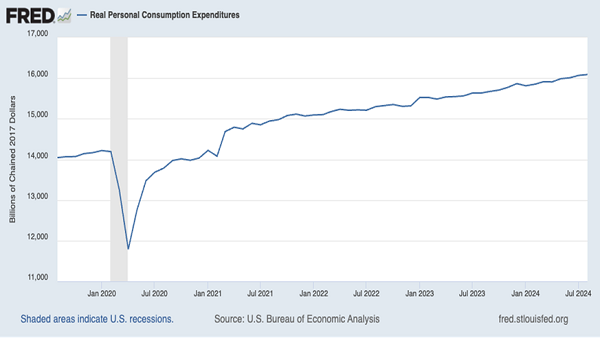

Lower Rates Boost Spending (But Only at Certain Times)

It’s true that lower rates encourage people to spend more. But remember too that rates tend to be cut during a recession. And in a recession, Americans are already cutting spending. So lower rates do tend to push up consumer spending in those times—albeit from an already-low base.

However, when Americans are already spending a lot, as they are today, cutting rates won’t necessarily do much.

As you can see above, the big jump in interest rates we’ve seen, from near nothing to 5.5% in just 18 months, didn’t slow consumer-spending growth. So it doesn’t make sense that consumer spending will grow with lower rates; that’s usually the case, but probably won’t be this time.

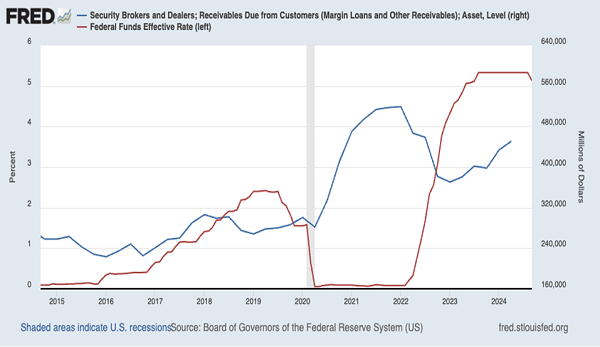

What about the buying-on-margin story? That idea is a bit broken, too.

As you can see, the lower cost of borrowing on margin (related to the federal funds rate, in red above) made for a huge amount of margin borrowing (the blue line) during the pandemic. But margin balances went back to their normal trend in 2022, when rates rose. This, by the way, is the main reason why stocks tanked that year.

In other words, the market has already gotten to a “normal” level of margin borrowing. Rates falling from 5% to 3%, where the Fed has said it wants them to settle, isn’t going to cause that speculative buying of small-cap stocks like we saw shortly after the pandemic—or for that matter, in the 2010s, when rates were also low.

That also means this chart is unlikely to repeat itself.

Small-Caps Merely Track the S&P 500 With Cheap Rates

In the low-rate 2010s, small caps started from being oversold during the Great Recession. But even with the low starting point, they merely tracked the S&P 500.

In other words, investing in small caps based on the idea that others will borrow to invest in them wasn’t a great move when rates were at 0.25%, let alone 3%. Which leads me to the final point: small caps’ investments in innovation.

Technology has become a big part of the total US stock market because tech firms have provided tremendous innovation over the last decade: Companies from across the economy depend more on Alphabet (GOOGL), Microsoft (MSFT), Oracle (ORCL) and the like more than ever. That trend has been running since the end of the dot-com bubble. The current scramble among big firms to integrate AI just exacerbates it.

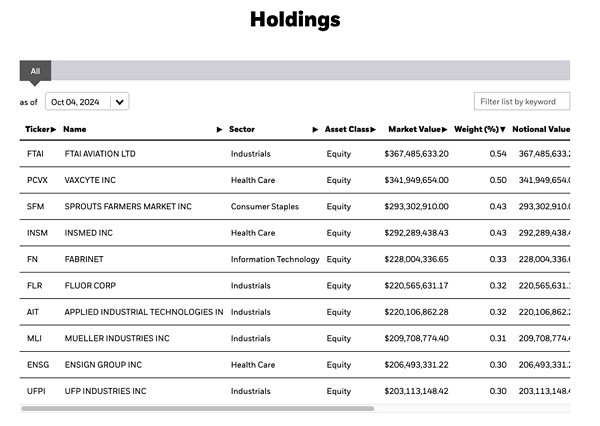

And that’s why the top constituents of IWM, the main small-cap index fund, are a worry.

Source: iShares.com

There are good companies in here, like FTAI Aviation (FTAI), which repairs and maintains jet engines.

But, as a few industry reports note (like this one and this one), the big aviation firms, like Boeing (BA) and Airbus, already use AI to improve their aircraft-maintenance services. So smaller firms like FTAI will need to invest in cutting-edge AI tech to compete.

That’s squeezes smaller companies’ profits more than those of larger firms. But the main winners are those that provide the AI infrastructure both the FTAIs and Boeings need—companies like Amazon.com (AMZN) and NVIDIA (NVDA).

This Small Cap CEF Looks Cheap, but It Could Get Cheaper

This brings us back to RVT. While its yield sounds great, at 7.3%, it’s actually low for CEFs, which yield 8.2% on average.

And while we love being contrarians at CEF Insider, in this case we can’t be, since RVT’s past performance shows that it should actually be cheaper. Let me explain.

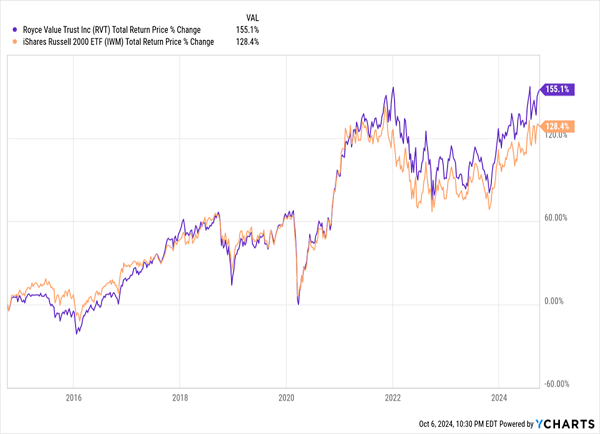

Outperformance: Now You See It …

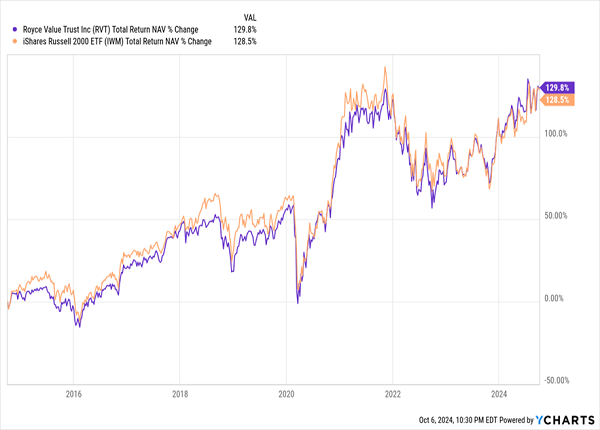

RVT’s market price (in purple above) has been beating IWM by a healthy margin over the last decade. But if we compare IWM to RVT’s total NAV return, which reflects the actual performance of the CEF’s managers, things look different.

… Now You Don’t

RVT has actually been tracking the small-cap index for a long time, and if its discount falls to 15% or lower, that’d be a great entry point. But at a 10.3% discount, given its 10-year average discount of 11.1%, RVT is still not a great deal for us.

Skip RVT: Grab This 10.5% Income Stream (Paid Monthly) Instead

RVT’s 7.3% dividend sounds great, but because it’s a more speculative CEF, its payout can fluctuate. We might be able to overlook that if there weren’t a higher, much steadier dividend on the table instead.

That would be the 10.5% payout on the 5-CEF “mini-portfolio” I want to share with you now. These 5 funds’ payouts are as steady as they come, drop into your account monthly and, because these 5 CEFs are bargains, I’m calling for strong price upside from them in the next 12 months!

Recent Comments