My six-year-old hooper was having an outstanding YMCA practice. She was leading the drills, encouraging her teammates and almost dribbling between her legs. So close.

And then, the very next minute, she was throwing a fit in the corner. Her tantrum would last the remainder of practice. She missed the end of the time-honored “kids versus coaches” game which the kids (as always) dominated.

One of the coaches (her father, and your income strategist) was not thrilled with her pouting but also not totally surprised. Parenting a soon-to-be-first grader is a rollercoaster. Best to enjoy the good moments and get through (or mentally block out!) the bad.

During her game on Saturday, on cue, she bounced back and sunk two baskets. If my youngest had a futures contract, I would wager on a rebound during her tantrums. (And short her good moments to hedge—ha! Just kidding. Mostly.)

Since my diva does not have a financial instrument attached to her mood, the closest we can do is to buy refineries that are due for a rebound. These are the six-year-olds of the stock market. In the long run they will be fine. In the interim, though, the swings can be wild.

As contrarian investors, we embrace chaos. While orderly moves higher inevitably give way to declines, the same can be said for washouts. Show us the stocks that have already pulled back. Let us bet on the kids crying in the corner while the vanilla types are chasing the AI du jour!

Phillips 66 (PSX) reminds me of my kid crying on her new rainbow basketball. PSX dropped 21% from its April highs. The stock’s drama reminds us why few investors have the stomach to buy and hold refiners.

They are, however, lovely stocks to trade! We can net a year’s worth of gains in one multi-month move. Would you believe that PSX is poised to kick off its third boom and bust cycle in the past year alone?

Boom Then Bust Then Boom for PSX

Why the ups and downs? Most investors have no clue because they don’t understand refiners. They confuse them with energy producers, who drill for oil and natural gas and then sell the raw products.

Refineries buy oil from producers and turn it into gasoline, diesel fuel, heating oil and other end products. Their dependency on others (the elementary school analogy continues!)—from the cost of oil as the input to economic activity as the driver of demand—can create several Wall Street “boom and bust” cycles per year.

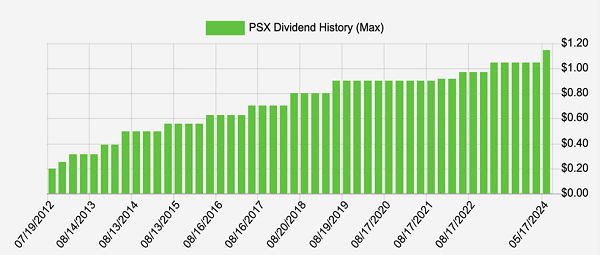

We wouldn’t know it by looking at Phillips’ dividend, up 28% over the past five years and 130% over the past decade. No drama here.

PSX: A Regular Dividend Raiser

Source: Income Calendar

The payout is funded by 13 refining facilities that can process 1.9 million barrels of crude oil per day. Phillips then sells fuel products at Phillips 66, Conoco and 76 branded gas stations. Summer road trippers fill up at Phillips’s 8,900 stations. The catalyst for the next mini-boom cycle is here.

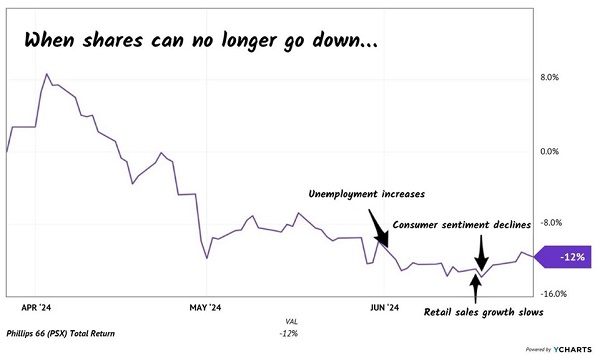

Shares yield 3.3% today. PSX has shrugged off most of the recent “bad” economic news. This is a sign that most economic worries are already priced in. When bad news does not take a stock lower, it has nowhere to go but up!

PSX Shrugs Off Bad Economic News

Meanwhile, crude oil is back above $80 per barrel, towards the higher end of its recent trading range. A near-term cap in crude would lift Phillips’ profit outlook. As you can see from PSX’s stock price, the manic Wall Street traders don’t wait for this dividend payer to report. They speculate ahead of time! And after such a serious spring decline, a quick double-digit bounce is possible.

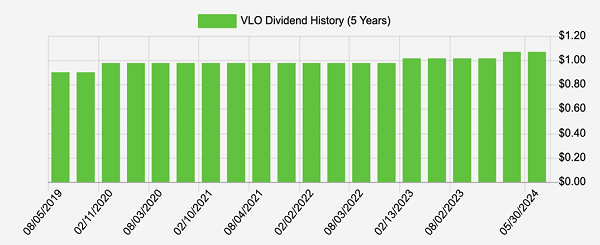

Valero Energy (VLO) looks promising here, too. VLO is down 19% from its April highs. It is usually my “go to” refiner but these days I prefer Phillips because Valero’s dividend has slowed down of late:

Valero’s Slowing Payout Growth

Source: Income Calendar

Historically, Valero was a rabid raiser—its payout popped 289% over the past 10 years! Most of that growth is in the past, however, with VLO’s divvie only 19% higher over the past five.

That said, Valero is the big dog in the refining space. These stocks tend to rally together and, if that happens, VLO as always will attract serious money. Regulators aren’t approving any more refineries and this blue chip already owns the “beachfront properties.”

Phillips and Valero are two talented kids that have been throwing tantrums since April. This is an attractive time to bet on rebounds in their behavior.

These are the types of “crisis-proof” retirement dividends I’m focusing on today. My only complaint is that Phillips and Valero don’t yield enough. Really, we need to secure 7% to 8% dividends or better to retire comfortably. Which is doable with my 7% crisis-proof retirement plan.

Recent Comments