I love the economics of real estate. But a landlord I’m not. Please, change your own lightbulb—don’t call me.

Enter real estate investment trusts (REITs), which provide us with landlord-style income from the comfort of computers and smartphones.

Why are these “virtual fourplex” deals available in convenient ticker form? Thank Congress (no, seriously!) By law, the bulk of a REIT’s income has to be returned to us, the shareholders, in the form of dividends. Even an average REIT is going to pay more than most other sectors, and some REIT dividends can get downright enormous—like the 7.8% to 22.3% yielders I’ll discuss here in a moment.

It hasn’t been a perfectly straight line, but the market has taken off this year. We’re near 2024’s midway point, and the S&P 500 has already delivered a double-digit return.

Sure, mega-caps dealing in artificial intelligence have done a lot of the lifting, but a lot of boats have been lifted by the rising tide. In fact, investors have bid up 10 of the market’s 11 sectors as of June 24.

The lone exception? Real estate.

Blame the Fed.

Higher interest rates make borrowing more expensive. That’s a weight on many types of companies, but REITs arguably suffer the worst.

Real estate was clobbered as the Federal Reserve started hiking rates at the start of 2022, and the beatings continued until a few months after the Fed’s final hike in July 2023. The sector started to bounce near the end of last year as every pundit predicted a gaggle of rate hikes throughout 2024, but—well, the Fed hasn’t delivered. The fed funds rate’s target range is stuck at 5.25%-5.50%, and expectations for this year have been tempered to one, maybe two cuts tops.

That’s great news for contrarians who still have some cash to put to work. We want to buy before the Fed finally triggers a stampede in REITs—not after.

So, let’s look at some of the potential opportunities that are waiting for takeoff. This five-pack of REITs yields 11.4%, on average, as I write and should benefit from eventual rate cuts.

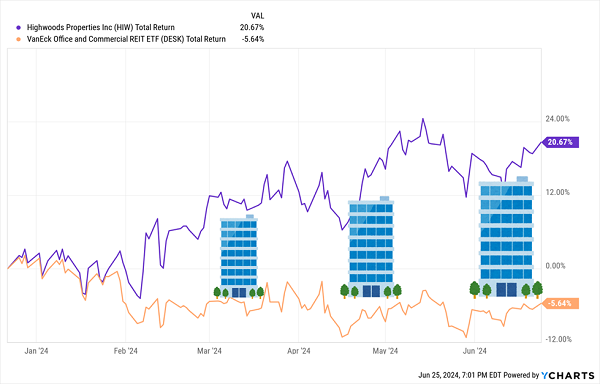

I’ll start with Highwoods Properties (HIW, 7.8% yield), an office REIT that predominantly operates in southern and southeastern markets including Atlanta, Charlotte, Dallas, Nashville and Orlando.

COVID hit nearly every corner of the market a few years ago, but few industries have suffered worse, or longer, than office real estate. While the environment for these operators has been improving amid employers pushing return-to-office (RTO) policies, metrics like security-card swipes and metro usage remain down 30%-50% from their pre-pandemic highs in many cities.

But when I last looked at HIW right before the end of 2023, I said:

“Where there is opportunity, however, is that many of these tenants are simultaneously upgrading into better-quality (and higher-priced) real estate. That bodes well for HIW, which is generally a good operator whose cash, FFO, and other important metrics have largely trended in the right direction for a decade or more.”

Apparently, the market agreed.

Investors Return to Highwoods Properties

There’s no one single thing that has propelled Highwoods higher, but a confluence of smaller factors working in HIW’s favor. In November 2023, it priced $350 million in bonds that allowed it to push out some debt maturities to 2026—ducking one headache (near-term maturities) that several of its peers still face. Leasing activity has been encouraging. Financial results have come in largely in line. And the stock’s deep discount from late 2023 has been shrinking.

Highwoods still faces an uphill battle in general office trends. Continued high interest rates aren’t a help, either—though they’re not as much of a hindrance to HIW as they would be to its poorer-capitalized peers. The dividend, at least for now, seems decently covered. It’s hardly a rah-rah operator, but Highwoods at least looks more comfortable than its competition.

Gladstone Commercial (GOOD, 8.7% yield) is another REIT that has suffered from its exposure to the office industry, though its presence in other markets has shielded it from even more downside.

Gladstone Commercial is part of the Gladstone family of REITs and business development companies (BDCs), which also includes Gladstone Land (LAND) and Gladstone Investment (GAIN) and Gladstone Capital (GLAD). It owns 132 single-tenant and anchored multi-tenant net-leased industrial and office properties across 27 states. A roughly 40% allocation to office properties kneecapped shares over the past few years, and also forced GOOD to reduce its monthly dividend by 20%, to 10 cents per share, in 2023.

GOOD is also solidly in the black in 2024, but I’m less enthusiastic. Gladstone is moving in the right direction—it has unloaded a few vacant office properties, bringing its office exposure to 36%. But those dispositions represented a mere morsel of the portfolio. It’s hardly being acquisitive, either, making it unlikely that its property mix will change significantly anytime soon. Combine all that with a fair valuation, and there’s little to get excited about.

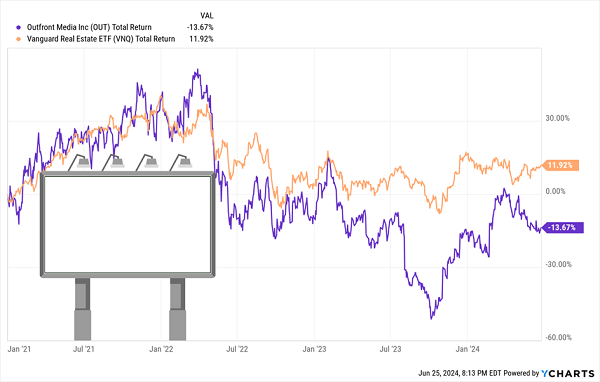

Outfront Media (OUT, 8.7% yield) is proof that we can invest in just about any kind of real estate we can think of. Specifically, Outfront allows us to get a piece of—well, anywhere advertisers want to stick an ad. That means billboards, transit stations, vehicles, even “mobile assets” (mobile ad campaigns tethered to, say, a customer in a store, or a person walking around a specific area).

Outfront has been enjoying an uplift in one of its weakest areas post-COVID: transit. That is, following the start of the pandemic, ridership in metro systems like the MTA and WMATA cratered; however, RTO policies have been continuing to lift those results.

Still, the situation is hardly perfect. Outfront is still struggling with weak national-media revenues, as well as rising billboard, posting and maintenance expenses.

Outfront is a decently positioned stock in dire need of a spark. OUT shares trade at just 8 times estimated adjusted funds from operations (AFFO), and the dividend, which yields nearly 9%, is plenty safe at just 70% of AFFO. Yet shares refuse to fully escape their funk.

Outfront Investors Are Waiting for a Sign

Global Medical REIT (GMRE, 9.5% yield) is an owner of off-campus medical office and post-acute, inpatient medical facilities. At the moment, it owns 185 buildings leased out to 268 tenants, with an occupancy of over 96%.

GMRE likely bottomed out in late 2022 after one of its tenants, Pipeline Health System, entered Chapter 11 bankruptcy protection. Regardless, it has been a roller coaster to nowhere, still down by roughly a quarter of its value over the past three years after a lot of hills and valleys.

Global Medical REIT is actually staring down yet another bankruptcy—this time by tenant Steward Health Care, which operates 31 hospitals and a physician group. But unlike Pipeline, the effect here should be minimal; only one of the six properties Steward leased from GMRE was material (less than 3% annualized base rent).

That said, GMRE has gone on the offensive, acquiring a 15-property portfolio for roughly $81 million, though interestingly, the company hasn’t yet determined exactly how it’s going to fund the deal.

And while I love the 9%-plus yield, Global Medical’s 21-cent-per-share dividend is perhaps a little too close to AFFO projections for comfort.

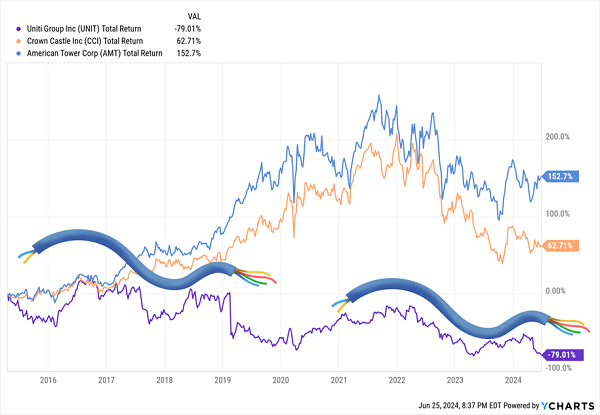

The screaming yield of the bunch belongs to Uniti Group (UNIT, 22.4% yield), a top-10 fiber provider in the U.S., boasting more than 141,000 fiber route miles and more than 8.5 million strand miles of fiber, connecting 300 metro markets and providing high-speed and networking services to more than 28,000 customers.

It’s a telecommunications infrastructure name that’s similar to the likes of American Tower (AMT) and Crown Castle (CCI).

Well, OK. Maybe Not All That Similar.

Uniti’s infrastructure powers what effectively are basic necessities at this point. That’s great for the status quo, but it hasn’t really meant anything for growth ever since Windstream spun off Uniti in 2015.

Things didn’t go so well for Windstream, either; the telecom filed for bankruptcy protection in 2019, then emerged from bankruptcy a year later.

But now, they’ll have a chance to recover together.

In early May, Uniti revealed it would merge with now privately held Windstream in a deal that’s expected to close in the second half of 2025. Says Reuters: “The proposed deal offers Windstream shareholders $425 million in cash, $575 million of preferred equity and a 38% stake in the combined company. Uniti shareholders will own the rest.”

Wall Street wasn’t exactly thrilled with the transaction, however, hammering shares by 37% in the two days following the announcement.

No small wonder. The prevailing expectation—echoed by Fitch Ratings and S&P Global Ratings, among others—is that Uniti will “de-REIT” when the merger closes, as well as put the kibosh on its dividend.

Earn a Reliable 8%+ in Retirement—Paid MONTHLY

As I frequently say, “What good is a double-digit yield today if it disappears tomorrow?” Normally, that’s just a general warning about the potential for shaky dividends to be reduced. But in Uniti’s case, it’s pretty literal—that 22% yield is amazing now, but it’s almost certainly going to vanish.

We don’t need that kind of drama in our lives, and we certainly don’t need it in our retirement portfolios.

What we want is dull, unremarkable, yawn-worthy holdings that just drip-drip-drip dividends into our accounts.

And that’s exactly what you’ll get with the beautifully boring, high-yielding blue chips I hold in my “8%+ Monthly Payer Portfolio.”

The “8%+ Monthly Payer Portfolio,” as the name would imply, can clearly deliver high levels of yield.

But it’s not just about that—this portfolio is about earning high levels of yields by leveraging steady-Eddie holdings with the potential to deliver meaningful price upside, too.

That means no more reaching for the Pepto every time the S&P gets the jitters.

That means no stressing about nest-egg shrinkage in your 60s, 70s, 80s, and beyond, either. Because unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

If you put this portfolio to work with a mere $500,000—less than half of what most financial gurus insist you need to retire—you’ll generate a roughly $40,000 annual income stream.

That’s $3,330 every month in regular income checks!

It’s time to get serious about locking down our core retirement holdings. Click here to learn everything you need about these generous monthly dividend payers right now!

Recent Comments