Three weeks into 2024 and here’s the state of play: rates have fallen and likely headed lower. That’s going to light a fire under our favorite dividend payers.

It already has!

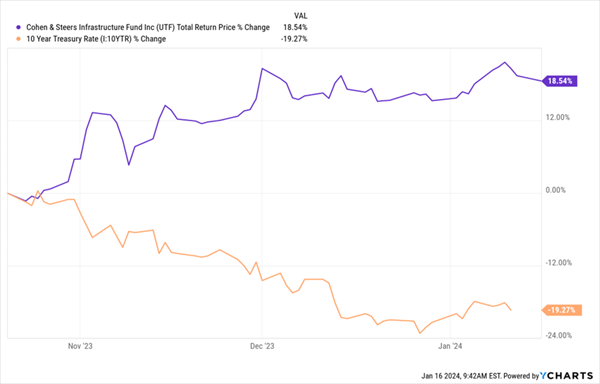

Think back three months, to mid-October. Back then, 10-year Treasury yields sat at just under 5%. Now they sit at 4.1%—a 19% drop! It’s been great for our dividend payers, as income-hungry folks start to look for other options.

That shift has just started, and it’s got plenty more room to run.

Consider the 8.5%-paying Cohen & Steers Infrastructure Fund (UTF), a closed-end fund (CEF) that’s a classic dividend play, holding shares of “recession-resistant” utilities like NextEra Energy (NEE) and Southern Company (SO).

It then complements those with other infrastructure stocks like American Tower (AMT) and pipeline operator TC Energy (TRP). UTF, as you might expect, has roared as the yield on the so-called “long bond” tanked:

High-Yield Pick Continues to Ride a “Rate Tailwind”

Right now, futures traders are calling for six Fed rate cuts this year. That might be a little aggressive, but even three or four would put a drag on Treasury yields and provide a further lift for stocks. UTF, with its portfolio of “bond proxy” utilities, is one way to play it (as utilities tend to rise when bond yields fall, and vice-versa).

But if you’re like me, there’s one thing you dread about adding new high-yielders to your portfolio: tracking their payouts!

Like most people, my bills come in every month. And I’m not cutting checks any longer; most of my expenses are on autopay. Which makes income tracking more important than ever. I need to make sure I have the money in the account before it gets dinged.

Your go-to these days is probably a spreadsheet. (It was mine until recently). But now we have a better option: a new toy whipped up by our IT team here at Contrarian Outlook called the Income Calendar.

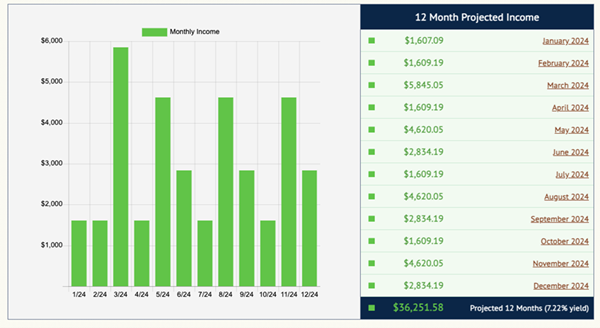

Let’s do a quick run-through, using five strong income plays (including UTF) that stand to gain as the 10-year Treasury yield drops further: STAG Industrial (STAG), a 4%-paying warehouse landlord; residential-real-estate lender Arbor Realty Trust (ABR)—current yield: 12%; long-term-care-home investor LTC Properties (LTC), with a 7% payout; and insurer Prudential Financial (PRU), whose yield rings in at just under 5%.

These five pay dividends both quarterly (ABR and PRU) and monthly (LTC, STAG and UTF). Let’s go ahead and plug them into Income Calendar, allocating $100,000 to each, for a $500,000 sample portfolio.

Right away, IC gives us the vitals—no finicky Excel formulas needed!

On the left, we’ve got an “at a glance” custom income forecast served up for us in an easy-to-read bar chart. And on the right, Income Calendar gets granular, giving us a dollars-and-cents monthly forecast, including our total projected income for the year of $36,251.58, good for a 7.2% yield. Not bad!

(And note that we intentionally don’t forecast dividend growth in IC, to be as conservative as possible, but we could likely expect a bit more than 7.2% as 2024 plays out.)

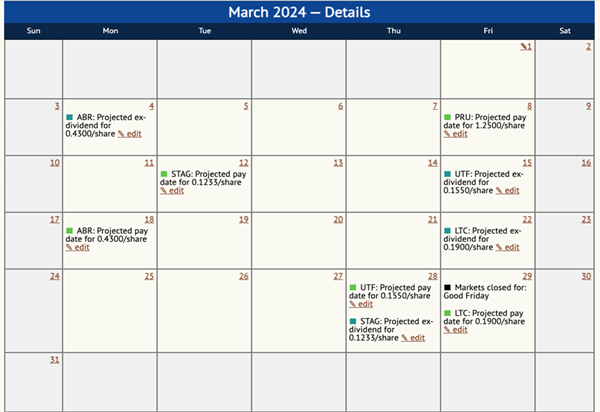

There’s more. Let’s dial up March 2024, a month in which we get paid by all five holdings in our “mini-portfolio.”

You can see that Income Calendar not only tracks our payouts but forecasts other key dates, like the ex-dividend date (or the date by which you need to be a shareholder to receive the next payout) and non-dividend-related events like market holidays.

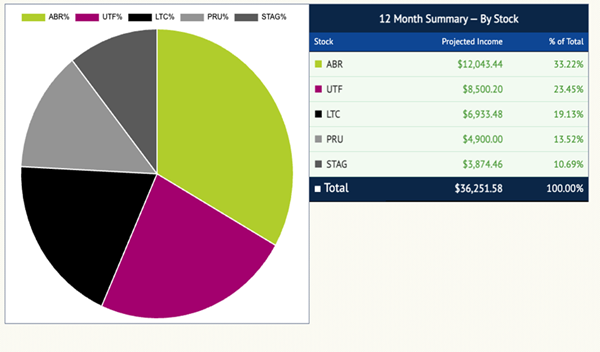

It’ll also tip you off to expected earnings dates (there aren’t any of those in March 2024, but they normally show up in red). Moreover you can get a sweet breakout by stock, too (no surprise that Arbor is the star of the show here, thanks to its 12% yield):

Let’s see an Excel spreadsheet do all that!

Income Calendar really is a complete roadmap that makes sure you’re always on top of what’s coming up for your holdings, and you’re never caught short of dividend cash when you need it.

One final note—we’ve recently made a major upgrade to IC: we’ve integrated it with Plaid, a service that safely and securely links up to your brokerage account and imports all your tickers and share counts—so you don’t have to do any inputting at all.

It’s easy to use, and if you appreciate convenience (who doesn’t?), I’m sure you’ll love it.

My Personal Invitation to You: Try Income Calendar With No Obligation

The best way for you to see what Income Calendar could do for you is to try it out yourself. Log in, drop in a few tickers. Maybe include a couple stocks you’ve been watching, just to see how your income stream could change with an extra buy or two.

I think you’ll quickly see how this new tool can save you valuable time—and give you peace of mind that your dividend cash will be in your account before your bills come out.

It couldn’t be easier to set up, and you’ve got no obligation whatsoever.

Simply click here to see the investor briefing I’ve put together on Income Calendar, including quick videos that demonstrate, step by step, exactly how to use it. You’ll also get a chance to “road test” the service for 60 days.

The start of a new year is the perfect time to try this new tool and get the next 12 months of dividend payouts lined up. Give it a shot today!

Recent Comments