Our favorite tech-sector dividend growers are finally on sale—and our time to “lock in” these fast-growing payouts has arrived.

Our Tech Buying Opportunity: Fully Booted Up

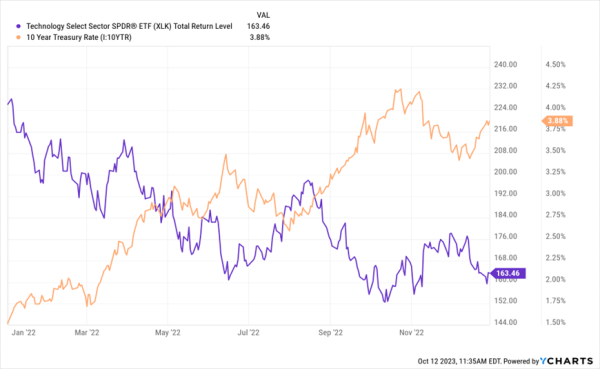

These days, fear surrounds us, and we contrarian income seekers know that times of fear are when we go shopping. That goes double for tech stocks, which tumble when the 10-year rises (and vice versa).

Take last year, when the rate on the “long bond” spiked and high-flying techs, shown in purple below by the performance of the benchmark Technology Select Sector SPDR ETF (XLK) hit the deck:

10-Year Tells Us When to Buy—and Sell—Top Tech Divs

Sure, the AI hype has fueled a nice rebound this year, but this latest spike in the 10-year has given us a nice—and rare—second chance to buy in, washing out many of our faves.

Over the last few weeks, I’ve been saying the 10-year would bump its head on the “4.3% ceiling” and retreat. The fact that it’s blown through that ceiling only means its fall will be that much harder—and our favorite tech-sector dividend payers will rip that much higher in response!

We’ve already started to see that happen, but it’s not too late to lock in historically high payouts (and rapid payout growth) from our favorite big-name techs.

Here’s something else most folks forget when it comes to Big Tech: it’s sitting on a pile of cash rivaling that of just about any sector except banks. The poster child here, of course, is Apple (AAPL), with its $167-billion hoard. As that cash gets put to work in buybacks, dividends, R&D or, as we’ll see in the two stocks below, acquisitions, we stand to benefit.

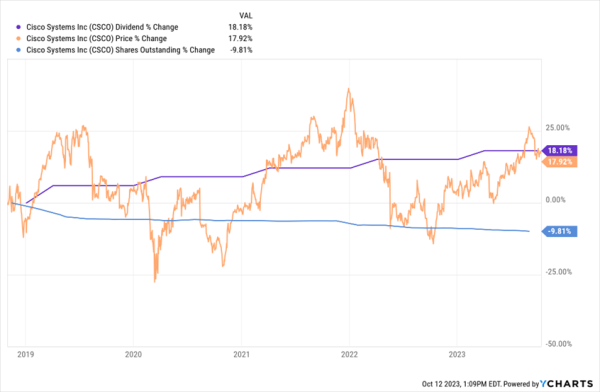

Big Tech Dividend No.1: Cisco Systems (CSCO)

Cisco’s networking gear puts it square in the tracks of AI’s rapid growth. But that’s just the headline. Look deeper and you’ll see something equally important: Its ongoing move into software—which, in turn, is driving its shift to a subscription-based model.

That shift will further stabilize Cisco’s revenue, and it’s taking hold nicely, with recurring revenue rising 5% in its 2023 fiscal year, to make up 43% of the total.

The company’s acquisition of Splunk (SPLK), announced in September, is yet another move in this direction, bringing in Splunk’s subscription-based cybersecurity software and putting Cisco in an even better position to leverage AI.

Cisco can easily afford Splunk, with $26 billion in cash and just $8 billion in long-term debt, a sliver of the company’s $219-billion market cap. Even so, it trades at just 13.3-times forward earnings. The deal won’t jeopardize Cisco’s payout growth, as it’s expected to add to cash flow in the first year. Plus, the dividend—current yield: 2.9%—already makes for a light load, at just 33% of Cisco’s last 12 months of free cash flow (FCF).

And while this payout isn’t growing as fast as it once did, it is a reliable “magnet” on the share price, as you can see below.

Dividends, Buybacks Combine to Pry CSCO Stock Higher

And we’ll give management a bit of a pass on payout growth because they’re buying back shares at a solid pace, as shown in the blue line above. And check out the drop in shares outstanding as everything—particularly tech—went into the dumpster in ’22. That’s a sign management knows when its stock is oversold—and when to accelerate its buybacks. That’s the kind of savvy we want.

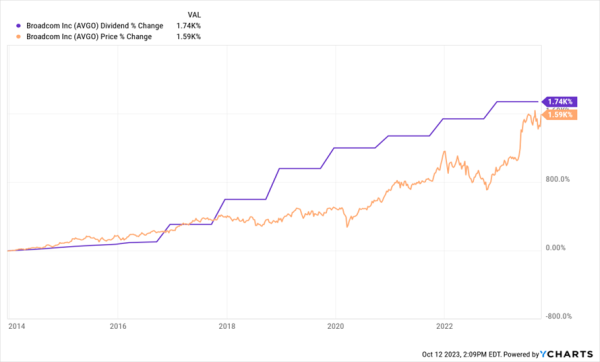

Big Tech Dividend No. 2: Broadcom (AVGO)

Semiconductor maker Broadcom ticks many of the same boxes as Cisco, starting with gains as AI drives demand for computing power. But there is one key difference: a much higher current yield: a stout 4.6% today.

Let’s rattle through the similarities between these two tech-dividend giants:

- No rate worries, thanks to a “fortress” balance sheet: Broadcom’s sitting on $12 billion in cash, and while it does carry $39 billion in debt, that’s just over 10% of its (massive) value as a public company: $373 billion. Peanuts.

- A big acquisition: That strong balance sheet leaves Broadcom plenty of room to close its looming $75-billion cash-and-stock purchase of VMware (VMW). The move will boost Broadcom’s presence in AI and cloud computing. Plus, VMW is profitable, with EPS jumping 34% in the latest quarter and revenue up 2.2%

- A safe dividend, at 43% of FCF, this one’s also easy to carry, especially when you consider revenue was up 5% in the last quarter, while EPS jumped 8%.

- A potent Dividend Magnet: No question! As I’ve said before, share prices always catch up to dividend growth—something Broadcom’s stock resisted for most of the past decade—till its 1,700% (!) payout growth in that time recently broke the stalemate.

Broadcom’s Dividend Magnet Wrestles Its Share Price Higher

To be sure, that stunning payout and share price growth has left Broadcom pricier than Cisco, at 21-times forward earnings. So it may not rip quite as high when rates do pull back. But that 4.6% yield and quadruple-digit payout growth more than make up for it. We can also consider that 4.6% a “starter” yield, with Broadcom set to announce its next hike in December.

The Dividend Magnet—Our Ticket to the Biggest Gains as Rates “Roll Over”

A decline in the 10-year will throw a lift under many stocks, with techs likely to soar the highest.

The two tickers above are great ways to climb onboard. But we’re not stopping there. We’re going to give ourselves an extra edge by sifting out the stocks with the fastest-growing payouts, which, as we saw above, always pull their share prices higher.

I’ve zeroed in on 5 picks with the most powerful Dividend Magnets … and the share prices that are (for now!) lagging that payout growth. When they “snap back,” we’ll be looking at big gains to go along with our fast-growing payouts!

It’s time to get ready. Click here and I’ll share more about my Dividend Magnet strategy and give you the opportunity to download a free Special Report naming these 5 picks.

Recent Comments