Want to know the secret to retiring on dividends alone?

Keep that capital intact.

We invest to generate income. The more we have, the greater our potential payouts. So, losing principal is the cardinal sin.

We want our dividends. And we want our prices intact, or better. (If they grind higher, we don’t argue!)

Stocks that are going “up” are tough to argue with. I know, I know—as contrarians we want to bargain shop. We can’t help ourselves to find a deal.

Well deals are great, but so is momentum—especially when it comes to dividend stocks, especially in a bear market. Show me a stock that’s going up when the world around is collapsing, and I want to know: “Why?!”

Today we’ll explore why with respect to five “power stocks” that are paying between 4.6% and 25% (yes, that’s no typo). It boils down to relative strength, which is exactly what it sounds like.

When an investment performs well in relation to something else, like its industry, sector, even the whole market. That doesn’t even necessarily mean positive returns—sometimes relative strength is just losing less.

Strong stocks tend to stay strong, giving them a solid base from which to jump. Hence, relative strength can be a powerful short-term driver—so much so that it’s one of the main factors I look for in my Dividend Swing Trader service.

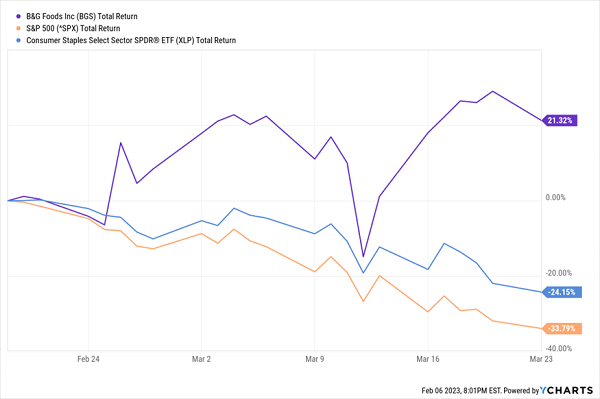

A great example from during the COVID bear market is B&G Foods (BGS), the name behind Crisco, Cream of Wheat, and Green Giant, among other major food brands. While the rest of the market (including B&G’s consumer staples sector!) was getting hammered, B&G wasn’t merely relatively strong—it was outright strong.

B&G in the Green With Giant Outperformance

Some people might have looked at this and figured all the easy money had been squeezed out. But this relative strength—combined with a still-juicy dividend—was a signal that even more strength could lie ahead. And sure enough:

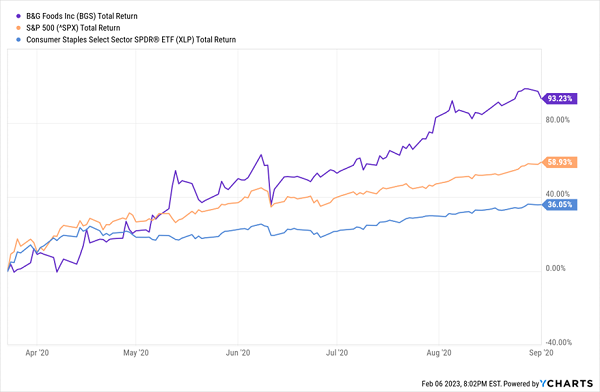

B&G Kept Trucking for Months

However, B&G was merely a dividend swing play for us; we took profits in just a matter of months. It’s a highly acquisitive company whose debt is often larger than its market capitalization—something that finally caught up to it amid 2022’s perfect storm of rapidly rising interest rates and inflationary pressures on its goods. Roughly two years after we exited the stock, the company cut its dividend by 60%, capping a miserable 2022 for BGS shareholders.

That’s because relative strength is only part of the story. For retirement dividends that we can rely on—bull or bear—we also need fundamental strength, financial strength, and dividend strength.

Right now, a mere 10 good- to great-yielding stocks across the S&P large-, mid-, and small-cap indexes are showing noteworthy relative strength, recently trading at 52-week highs. Let’s dig into five of the most interesting candidates.

2 REITs Yielding 4%-Plus

High yields are the finest feature we enjoy when we buy real estate investment trusts (REITs). Remember: At least 90% of their taxable income must be distributed to shareholders. The sector yields much higher than the market average as a result, and most dividend-safety sticklers won’t even blink at 4%-5% yields in the space.

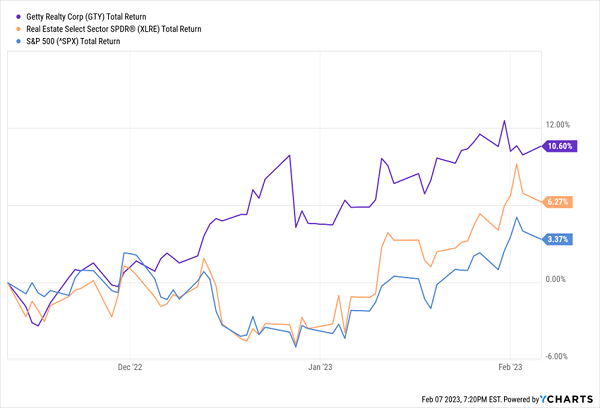

One REIT hitting 52-week highs of late is Getty Realty (GTY, 4.8% yield), a single-tenant retail specialist with more than 1,000 properties across 38 states and the District of Columbia. It’s a beautiful, boring landlord, too—tenants include Valvoline (VVV) auto parts and service stores, BP (BP) gas stations, and 7-Eleven convenience marts.

Stability, stability, stability.

If this REIT sounds familiar, I covered it back in November, calling it a “unicorn” that was bucking the market by delivering total-return gains against a down market last year. And the good times have continued since then, with GTY continuing to outperform the pack.

Getty Realty: The Getting’s Still Good

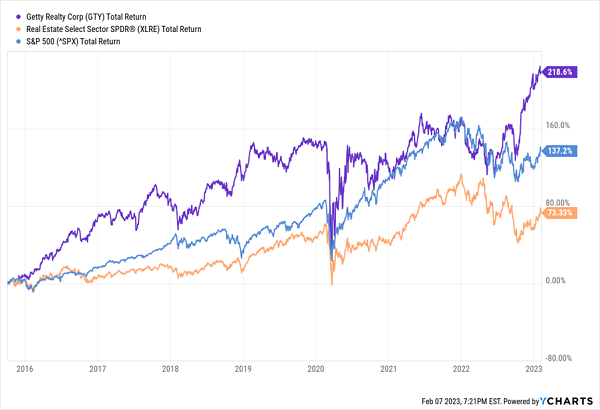

This run, by the way, continues a much longer-standing period of outperformance, with GTY roughly tripling the real estate sector over the past seven-plus years.

7-Elevens and Valvolines Are Good Business

Getty Realty kicked off the new year with an improved dividend of 43 cents per share, up 5% from its previous payout. Even if we measured GTY’s dividend coverage over the past year based on its fresh distribution, Getty’s still only paying out 82% of funds from operations (FFO) to keep it afloat.

The other nice-yielding REIT making 52-week highs of late is outlet mall giant Tanger Factory Outlet (SKT, 4.6% yield). Tanger currently boasts 36 centers (with one more in development) across 20 states and Canada, leased out to more than 600 different companies.

Unfortunately for SKT, its business isn’t nearly as boring—or dependable—as Getty’s. While management is skilled, there’s only so much you can do as a company that’s a.) heavily at the mercy of economic conditions, b.) fighting for survival against online retail, and c.) vulnerable to still-rising and relatively high interest rates. That first factor came into play during COVID, when it was forced to temporarily suspend its dividend—and while it has resumed payouts and increased the dividend a couple times since then, SKT is still doling out 39% less than it was prior to the cut.

Now wouldn’t be the time to buy, anyways. Tanger’s shares have been on a heater of late, and as a result, it’s trading at roughly 11 times forward FFO estimates. That doesn’t sound rich, but it’s plenty more expensive than its historic 9 forward P/FFO.

2 Furniture Plays Yielding 5%-Plus

A wild multiyear roller-coaster ride in furniture stocks is climbing the hill again.

As COVID drove people out of the office and into their homes, any stocks involved in remodeling, furnishing or otherwise improving things around the house took off—but after about a year or so, even though their operations continued to thrive, their stock prices came back to earth.

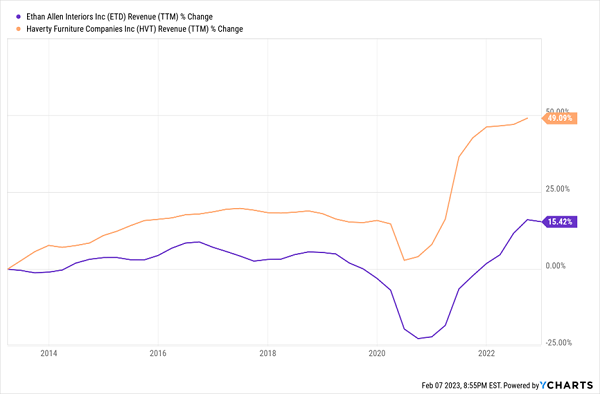

Furniture Revenues Are Still in the Post-COVID Upswing

They’re launching again, however, and two particularly nice yields in the space—Ethan Allen Interiors (ETD, 6.0% yield) and Haverty Furniture Companies (HVT, 5.9% yield)—have bolted to 52-week highs.

Haverty Furniture has more than 100 showrooms in 16 states, primarily in the South and Midwest. Meanwhile, Ethan Allen has 139 company-owned retail design centers in the U.S. and Canada, as well as independently operated stores in the U.S., Asia, the Middle East and Europe; it also has 10 manufacturing facilities.

Both stocks’ success has come alongside improvements in sales and operating margins over the past few quarters. Ethan Allen is a particularly interesting story—investments in digital marketing have paid off, as have investments in VR software, and its higher-end customer base is more recession-proof than most.

There’s a lot to like here, but dividend investors should know their headline yields are—not misleading, but perhaps a bit optimistic for the long term. Both yields are augmented by special dividends (ETD actually yields 4.3% based on its regular payout, while HVT yields 3.1%). Both stocks’ regular dividends have been on the upswing for years, which is laudable—but the special payouts might not always be there.

And it bears reminding readers that both stocks had to cut their payouts during the Great Recession. It’s a while back now, but it’s not unprecedented.

A Shipper With a Whopper 25% Yield

It’s hard not to salivate thinking about shipper Dorian LPG (LPG, 25% yield), which has doled out fully a quarter of its share price in dividends over the past year.

That’s a flabbergasting 15x the S&P 500’s yield right now.

Dorian LPG is a liquefied petroleum gas (LPG) shipping company that owns and operates very large gas carriers (VLGCs)—massive ships that typically run 250 to 300 meters long capable of transporting 100,000 to 200,000 cubic meters of gas.

Dorian’s shares have run up by more than 75% over the past year as LPG wasn’t spared from the global energy shortage. The company has enjoyed fat time charter equivalent (TCE) rates, which have sent profits spiking (net income tripled YoY over the most recent quarter).

To the delight of shareholders, Dorian is taking those profits and dumping them straight into investors’ laps. It doesn’t have much of a dividend history—payouts started in 2021—but that’s not my worry with LPG’s dividend program.

My worry is that there is no formal dividend program.

Dorian has been paying dividends on a fairly regular basis, but the shipper makes no bones about the potentially ethereal nature of its dividends: It refers to them in all mentions as “irregular” dividends.

No surprise there. Shipping is a notoriously volatile industry, so it makes sense for LPG to simply pay what it can, when it can.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

I know, I know. I’d kill for a 25% yield in retirement, too. But those massive double-digit yields are often too good to be true.

Or at least, they’re often too good to be reliable—and reliable is one of the most vital qualities that your retirement holdings simply must have.

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we can’t rely on special dividends that disappear and reappear every few years. We need to be able to plan around our income with laser precision.

Which is why we only hold dependable payers in our “Perfect Income” portfolio.

What makes these dividend holdings “perfect”?

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for every position in my “Perfect Income” portfolio.

Let me show you the stocks and funds you need to stabilize your retirement today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Recent Comments