Most folks don’t know it, but real estate has clobbered stocks in the long run, and it’s poised to pull off a win again in 2023.

And we dividend investors are nicely lined up to cash in, thanks to a fund throwing off a blockbuster 9.9% yield that’s the perfect play here. I’ll drop the name and ticker in a sec.

First, you read that right: real estate does outperform stocks over the long haul—and by no small amount, either! It’s clear as can be in this comparison between the SPDR Dow Jones REIT ETF (RWR), the index fund for publicly traded real estate investment trusts (REITs), and the S&P 500 over the last 20 years.

Real Estate Outruns Stocks, With More Dividend Income, Too

Bear in mind that this period included the COVID-19 crash and the subprime mortgage crisis, which, of course, walloped housing. No problem. REITs—publicly traded companies that own everything from warehouses to apartment buildings—bobbed right back up to the surface!

The key to REITs’ appeal is that they’re “pass through” investments: they collect rent checks from tenants, skim off enough to keep the lights on and the buildings clean, then hand the rest to us as dividends. The result is a bigger income stream than regular stocks pay: the typical REIT yields 3.2%, doubling the S&P 500’s miserable 1.5%.

But even though RWR has crushed stocks, we do not want to go the passive ETF route here. For one, RWR’s 3.2% yield is nowhere near big enough to get our hearts racing. And second, with REITs (as with pretty well everything these days), having a smart, responsive manager is critical.

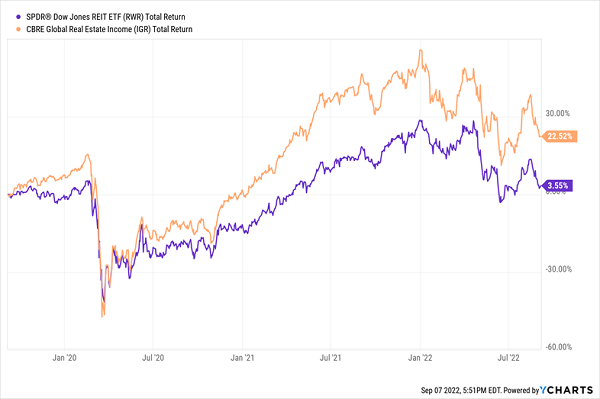

The proof is in RWR’s return over the last three volatile years, compared to that of the closed-end fund (CEF) we’re going to talk about today, the CBRE Global Real Estate Income Fund (IGR)—shown in orange below. IGR throws off that massive 9.9% payout I mentioned a second ago (and it pays you monthly, no less):

Active Management Gives IGR an Edge in a Cutthroat Market

The main reason for this comes down to IGR’s expert portfolio managers, who’ve deftly navigated the local markets they know best. That’s key in real estate, which we all know is really just a collection of small markets that are all behaving differently at any given time.

And when it comes to real estate, the fund’s management firm, CBRE, has no shortage of knowledge: in addition to IGR and private-investor funds, it manages properties, operates a brokerage and invests its own money in real estate. The company boasts 80,000 employees in over 100 countries, giving it a global perspective and relationships in foreign countries that no algorithm-run ETF can match.

CBRE has leveraged that knowledge to smartly lean IGR’s portfolio heavily toward the US (68%), a prudent move as the US economy continues to grow at a healthy clip, with inflation looking like it’s starting to crest and consumer spending (not to mention employment) holding up nicely.

But buying a well-managed real estate fund isn’t just about buying into management’s research power and access to information—it’s also about diversification, which is particularly key in real estate.

IGR, for example, invests in over 80 REITs, which themselves own hundreds and sometimes thousands of properties apiece. And like the many other REIT funds that do the same, it doesn’t notice when one bum tenant stops paying rent, because there are thousands of others that do.

Right now, for example, IGR’s top holdings include REITs that own a wide range of properties. Crown Castle International (CCI), for instance, owns more than 40,000 cell towers around the globe, plus 115,000 “small cells” that boost local-network capacity in bigger cities; Prologis (PLD) owns 4,732 warehouses across the globe; and residential REIT Invitation Homes (INVH), rents out more than 85,000 single-family homes.

So we’ve already got a ton of diversification here, and that’s just from three of IGR’s holdings!

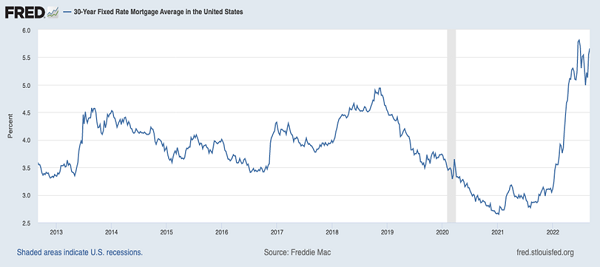

Another often-overlooked reason to consider REIT funds is that both these funds and REITs themselves have access to cheaper leverage than you and I. Right now, for example, spiking mortgage rates are a big problem for individual investors who own rental property—but not so for REITs:

Mortgage Payments Go Through the Roof

With interest rates hitting 5% earlier this year and staying at that level, home loans have soared. But interest rates for REITs are much lower, with many currently having borrowing costs on the books below 3%.

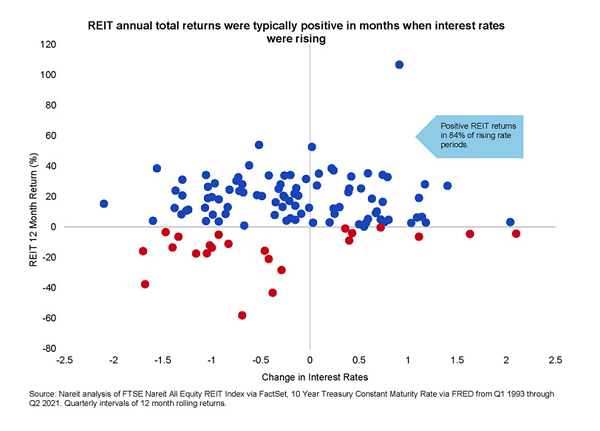

REITs enjoy lower rates because they’re professionally managed and diversified across many properties, so they’re lower risk than your typical individual property investor. This is one of the reasons why REITs actually have a fairly consistent record of posting positive returns during periods of rising interest rates.

This chart is based on a study by NAREIT, a REIT research and data firm, and it clearly shows that REITs typically earn profits during periods of higher interest rates. This is because their lower borrowing costs somewhat insulate them from the trend. Moreover, rising-rate periods typically come with a strong economy (as is the case today). That means higher demand for REITs’ properties, which lets REITs boost the rent. Those increases far outpace any rise in borrowing costs due to higher rates.

Buy IGR as “Discount Momentum” Builds

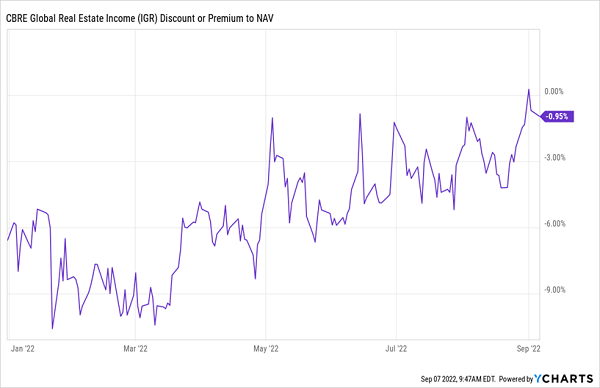

Finally, let’s talk about IGR’s discount to NAV, or the difference between its market price and the per-share value of its portfolio (this measure is unique to CEFs). Right now, that discount is small, meaning IGR is more or less fairly valued. But as you can see below, its discount has been swiftly narrowing:

Discount Looks Set to Break Into Premium Territory

The trend here is clear: IGR’s discount is headed into premium territory—the question is how far. As that happens, it will put more thrust under IGR’s stock price. And of course, you’ll pick up that healthy 9.9% payout (paid monthly) the whole time.

Trade Alert: 5 Ridiculously Cheap CEFs to Buy Now (for 8.6%+ Yields)

Finding ignored dividend opportunities like IGR is exactly what we do in our CEF Insider service, and I’m urging my members to grab 5 other CEFs now, for two crystal-clear reasons:

- (Overdone) fears of the Fed have (unjustly) driven these 5 funds’ prices to massive–and temporary–discounts, and …

- These 5 funds’ 8.5% dividends far outpace anything you’ll get on a regular stock, ETF or Treasury.

Let’s talk diversification: beyond real estate, these 5 stout income plays hold top pharma stocks (which will profit from our aging population and more people paying attention to their health post-COVID), battle-tested blue chip stocks, top-quality corporate bonds and (overly) beaten down tech names.

I think you’ll agree that this is a diverse crop, which gives this 5-CEF “mini-portfolio” an added level of safety. Plus these 5 funds combine to hand you that healthy 8.6% average dividend I mentioned a second ago!

The sooner you buy, the sooner your first dividend payout will arrive! Click here and I’ll tell you how I find lucrative dividend opportunities like these. Plus I’ll give you my complete research on these 5 off-the-radar 8.6%-yielding CEFs in an exclusive Special Report.

Recent Comments