In just over a month, the script has flipped for us dividend investors: Russia’s war on Ukraine has cleaved the world into two teams: east vs. west.

Some pundits have dubbed it Cold War 2.0. But whatever you call it, I think you’ll agree that the risks in this new arrangement are higher for us: we’re likely looking at another pop in the inflation rate, for one, due to (seemingly) never-ending supply-chain issues.

So it follows that Fed Chair Jay Powell will probably hike interest rates further than he otherwise would have as he tries to fix those supply-chain problems by making borrowing more expensive (if you can follow the logic there, please let me know, because it beats me!).

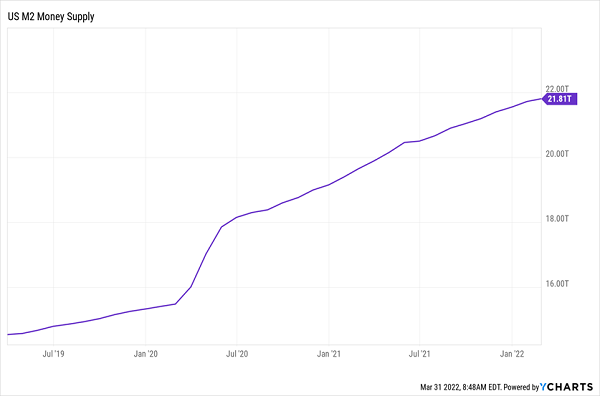

But mostly our man Jay is trying to “mop up” the mess he made by expanding the US money supply by 42% since February 2020.

“Paging Jay for a Clean Up on Aisle 6 (and 7 and 8 and 9…)”

Look, we can go on all day about ways to protect our profits (and dividends!) from this mess. And the truth is, we’ve done that to great effect in our Hidden Yields dividend-growth service.

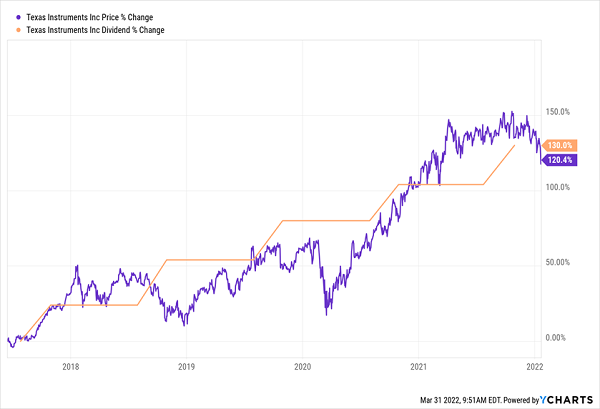

Our recent moves include easing up on rate-sensitive areas like technology—and locking in some nice triple-digit gains in the process, like we did with Texas Instruments (TXN), which handed us a 148% total return (including dividends) in just under five years when we sold it in January.

As you can see below, we rode TXN’s “Dividend Magnet” to that big win. By that I mean a stock’s tendency to track its dividend higher as the payout grows. Look at how TXN’s payout growth lifted its price during our holding period:

Taking Our “Dividend-Powered” TXN Gains Off the Table

I’ve seen this pattern again and again with dividend growers (and we’ll see it in action with the two “perfect for 2022” dividend growers we’ll discuss below, too).

And then there was customer-service-software maker Concentrix (CNXC), which handed us Hidden Yielders a fast 112% return in just over a year when we sold it in December! And cell-tower “landlord” American Tower (AMT), which we sold last month for a nice 57% gain in a little more than three years.

All three of the stocks I just mentioned are great companies—but as I mentioned, all three are a little too exposed to rate risk for our liking today. (And as much as I love AMT, I worry it may have overpaid for its latest acquisition, data-center REIT CoreSite Realty [COR].)

But we’re not just going to play defense here. We’re going on offense by tapping one of today’s most powerful (and least talked about!) megatrends—one that’s been supercharged by Russia’s pointless war on Ukraine: onshoring.

American Industry Comes Home (or at Least to Friendlier Locales)

Some folks call it “reshoring” or “deglobalization.” You may also have heard the term “friend-shoring,” where companies move to countries with strong relationships with the US.

Whatever you call it, the tariff wars of the late 2010s kicked it off, then COVID-19, with its supply-chain snarls and PPE scavenger hunts, accelerated it.

Then came the war in Ukraine, which whacked supply chains again while jacking up shipping costs. Meantime, companies that still haven’t gotten the message and have stood pat in China are getting twitchy as Xi Jinping gazes across the Taiwan Strait.

So given all that, what the heck are we going to do?

Simple: we’ll zero in on manufacturing stocks that focus on developed markets (especially the US) and/or are “onshoring” into those places.

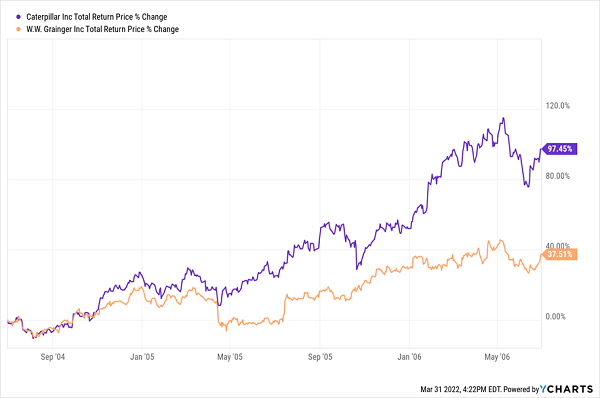

Better still, manufacturing stocks tend to do well when rates rise. Let’s look at 2004 to 2006, when rates spiked from 1% to 5.25% in just two years. That’s a landslide, and that cycle peaked far above where rates are expected to go today.

No matter. The two stocks we’ll look at below—heavy-equipment maker Caterpillar (CAT) and parts-distributor W.W. Grainger (GWW), soared.

Top Manufacturers Rolled Through the Last Rate Surge

Both have a big presence in America or “friendly” countries, and both have fast-growing dividends that “magnetize” their share prices.

Caterpillar: Onshoring Before Onshoring Was Cool

Caterpillar is the quintessential American success story: the Deerfield, Illinois–based heavy-equipment maker is nearing its 100th anniversary, having been founded back in 1925.

Let’s take a second here to tip our hat to co-founder Ben Holt’s “Caterpillar,” which he invented by replacing the wheels on his tractor design with treads in 1904, so the machines could traverse muddy fields:

Source: Holtcat.com

Caterpillar’s dividend is almost as old as the company itself: the payout started rolling out to investors in 1933 (in the depths of the Great Depression, no less), and CAT has hiked it every year for the last 28, earning itself a spot on the Dividend Aristocrats list.

The company has been expanding in the US over the last decade, opening new plants in Georgia, for example, and expanding its operation in West Fargo, North Dakota. And how’s this for a Dividend Magnet?

CAT’s Payout Doubles—and So Does Its Share Price

We’ve got plenty of reasons to expect CAT’s “magnet” to get stronger, thanks to the 27% jump in trailing-12-month free cash flow (FCF) the company has booked in the last three years. Plus it boasts a very safe payout ratio, with 49% of FCF headed out the door as dividends. That potential dividend growth means you can expect the 2% yield you get on a buy made today to start arcing higher before long.

Grainger Hiked Dividends Through the Last Cold War

Grainger is another built-to-last American firm, but unlike CAT, almost no one talks about the humble parts distributor. But it should be on every dividend investor’s radar.

The company was founded in 1927, only a couple of years after CAT, so it, too, has survived booms, busts, inflation, deflation, wars, you name it. Also like Caterpillar, it has been paying (and hiking) dividends for decades: Grainger’s payout has climbed annually for 50 straight years.

The company distributes all manner of parts manufacturers need: fasteners, plumbing pieces, motors and lighting among them. It deals with 5,000+ suppliers and boasts some 4.5 million customers.

Grainger’s operations are mainly in North America, Japan and the UK, which puts it in an excellent position to deal with supply-chain snarls. In fact, the folks at Grainger are probably wondering what all the fuss is about! In the fourth quarter, adjusted earnings popped 49% from a year ago on a 14% jump in sales.

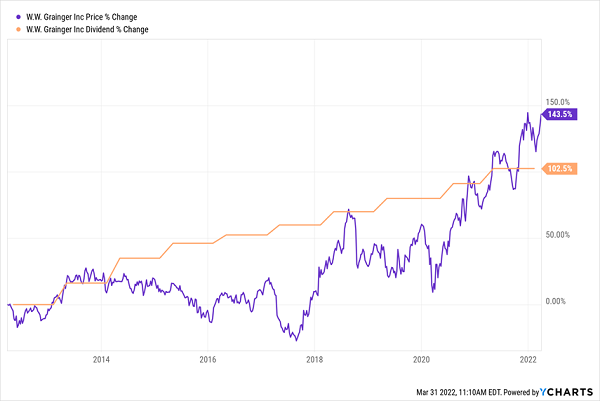

And like CAT, Grainger boasts a potent Dividend Magnet:

Dividend Doubles, Share Price Doubles

Also like Caterpillar, we can expect this run to continue: the payout occupies a safe 52% of FCF and only 34% of earnings. Resilient demand for goods across the globe, plus a continued restoration of supply chains, will support Grainger’s cash-flow growth and help grow its payout faster.

On that note, Grainger typically declares dividend hikes at the end of April, and its last one came in at a nice 6% increase. That makes now a good time to buy, before news of the next (likely substantial) hike breaks—and draws more buyers to the stock.

I’ve Handpicked These 7 “Great Reset” Stocks to Surge in ’22—and Beyond

As globalization fades and more companies come home, a select group of investors are poised to cash in. I want you to be among them.

I’m talking specifically about the folks who buy my top 7 stocks for the coming “Great American Reset.”

Of course, we know this reset is well underway: it started when COVID hit two years ago. Thing is, most people think it’s now nearly done, with restrictions lifting and everyone clambering to get back to “normal.”

But “normal” is over! As we just discussed, globalization is a fading trend, while the ways we work, play and communicate have changed forever.

Caterpillar and Grainger are two stocks that are perfectly positioned to play this shift. And I’ve uncovered 7 more I want to show you right here.

These 7 companies all have powerful Dividend Magnets poised to yank their share prices higher, and all are cheap now, as mainstream investors desperately try to ignore the changes taking place and pretend it’s 2019 again.

I expect these 7 names to surge in the back half of 2022, as off-the-radar trends like onshoring finally go mainstream. In the long haul, I’m calling for 15%+ annualized returns as these 7 winners lead the markets higher!

Recent Comments