“C’mon daddy.”

Pause. And a sigh.

“I’ll pay you back?”

Ah, there it was. The fiscal responsibility we’ve been working to instill in our seven-year-old clicking in. An acknowledgement that money does not grow on trees.

(Everyone knows that greenbacks only grow on the Federal Reserve’s balance sheet!)

My daughter’s intentions were sweet. She had successfully lobbied to reroute the “daddy bus” to a boutique retail store. The young boss had her eyes on a toy, and offered to buy one for her sister, too.

Well, I should clarify. Initially she offered me the opportunity to purchase both. Your income strategist offered a compromise:

“How about you pay for your own. And I’ll buy the other for your sister.”

Her rebuttal was quick. “But I don’t have my money with me.”

It was not, however, her dad’s first rodeo with a broke accomplice. I had a friend in college who would regularly roll out to the bars with his ID but no wallet (and hence, no cash.) Younger me would cover his beers, which routinely ran into the double digits.

“You can pay me back,” I offered my daughter.

The credit risk of my child not paying me back was low. She was about to owe me $10, and the new sign on her piggybank read $34.91. Only seven, she already had a tip top credit score with me.

Your Income Strategist’s Loan Collateral

Now she’s looking to replenish her war chest by performing household chores. Which was great, until she began asking her mother how much specific items cost. And she began quoting me $20 for every task.

(“She knows how expensive everything is,” my wife explained to me this morning.)

The Fed’s money printing has created wage inflation in my own household. Twenty dollars to pick up the playroom—ridiculous.

Hot inflation numbers and rising interest rates are weighing on bond prices, too. Rising rates have weighted on these popular bond funds:

- The iShares 20+ Year Treasury Bond ETF (TLT) is down 11% year-to-date. This is not what investors sign up for when they buy “safe” Treasuries. But who wants to hold TLT’s 1.7% yield in a country with 8% inflation?

- The iShares iBoxx $ High Yield Corporate Bond ETF (HYG), meanwhile, is only down 5% year-to-date, thanks to its 4.3% yield.

Still, we don’t like to see bond funds lose value. Their job is to pay us and, if nothing else, tread sideways. Should we be worried about the safety of bond dividends?

After all, in Stockville, falling share prices often signal a dividend that is in danger. Does this apply to Bondland?

Not really. Bond prices have two drivers: duration risk and credit risk, in industry parlance. Most bonds and bond funds have been penalized for duration year-to-date, because the long rate (10-year Treasury rate) and inflation have risen.

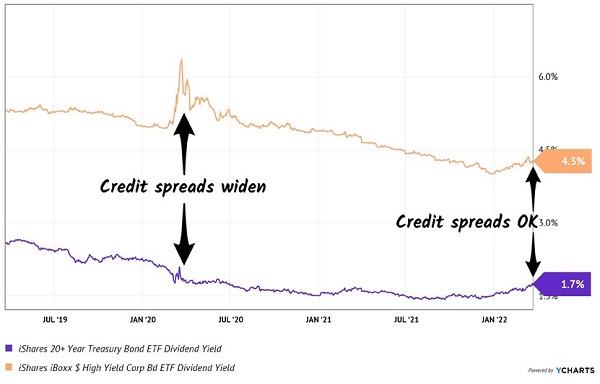

Credit risk isn’t an issue today—which means the payments are safe. I’ll show you how we can verify with a quick check of credit spreads.

Credit spreads show the probability of payback—the “$34.91 piggybank signs” of the bond world. Steady spreads show that fixed-income investors are not worried about credit risk because they are willing to trade risk for more yield.

A quick way to check credit spreads is to compare the yields on the HYG and TLT funds. I chose each because they are big, liquid and reflective of their markets. TLTs is a one-click proxy for Treasuries while HYG is the largest high-yield (“junk”) bond fund in the world.

If trouble was brewing in the credit markets, the relationship between these funds would show it. Specifically, the “spread” between the yields offered by each ETF would be widening.

In March 2020, spreads between TLT and HYG widened quickly. The global economy was on the brink as we hunkered down. Because corporate debt looked like a bubble about to burst, investors fled into higher-quality Treasuries (and TLT) and fled junk bonds (and HYG).

These spreads really could have blown out, except the Fed started printing money like crazy. With the new cash, Fed boss Jay Powell bought debt across the board—from Treasuries to junk bond ETFs themselves! Powell’s printer quickly calmed these credit spreads down:

In March 2020, Spreads Widened. They’re OK Now.

Moving to the right-side of the chart, we can see that as of today, spreads are OK (within their normal range). Subject to change, sure, but currently credit risk is low in the bond market. We should expect our dividends will continue to be paid.

Duration risk, unfortunately, is another story today. The long rate keeps rising, and why wouldn’t it? Inflation is higher than Snoop Dogg, medicated at its most extreme levels in forty years.

To protect against inflation, rising rates and potential problems in our retirement portfolios, I’ve created the Perfect Crisis-Proof Retirement Portfolio.

With this retirement strategy, you can 4x your current investment income with very little risk. Please let me share the details, plus my full dividend research with you, right here.

Recent Comments