If you’re on the lookout for an expert to help you build your nest egg—and bulk up your dividend stream to, say, a 6%+ yield—you have two main choices: a professional wealth manager or an investment advisory service (or a newsletter, as they’re more commonly known).

Which is for you? Let’s break down both options. Then we’ll dive into the kind of three-fund portfolio a newsletter might tip you off to, with a healthy 6.1% income stream and a history of double-digit yearly returns, too.

Wealth Managers Charge More, But They’re a Help in a Crisis

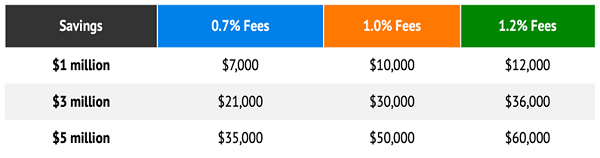

With active wealth management, the main concern most people have is fees. The industry standard is somewhere around 0.7% to 1.2% of your portfolio’s value annually.

That’s far less than, say, the 6% commission real estate agents typically charge on a home sale, but these fees do add up, especially on a larger nest egg: with $5 million saved, a manager on the lower end of the above range will still cost you $35,000 per year in fees.

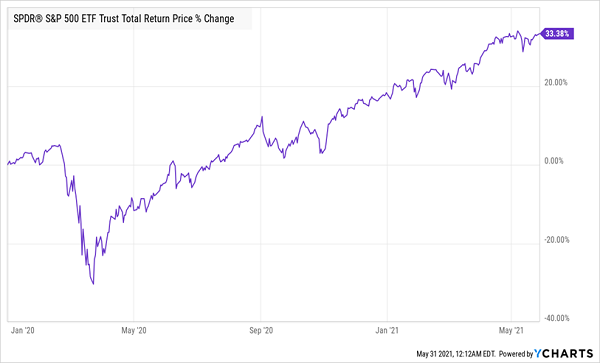

Still, thousands of people pay those fees every year, so surely there’s something to hiring a wealth manager, right? There definitely is. For instance, during the 2020 downturn, a lot of panicked investors wanted to sell and were talked off the ledge by wealth managers, who told them to be patient and stick it out. That, obviously, was the right call.

Emotion-Based Moves Locked in Big Losses in ’20

If your $5 million nest egg dropped by $1 million in March 2020 and you sold, you not only lost a million dollars, but you also missed out on the $1.5 million in profits the market has delivered since before the pandemic began. If a wealth manager helps you both avoid $1 million in losses and get $1.5 million in profits, surely that’s worth shelling out a 1% fee for.

Newsletters Can Help You Track Down Big Dividends at Less Cost

Obviously, the courage to hold on during a dip is valuable. But it is possible to get that elsewhere, for less, on your own if you have the right temperament for it.

You can do what many wealthy investors do and subscribe to newsletters written by experts they trust. Among the newsletter writers out there, you’ll find those who are successful investors themselves and/or former workers at hedge funds and investment banks; in other words, people who are obsessed with markets and spend their time finding the best ways to minimize losses and optimize gains.

One place a newsletter can make a big difference is in helping you seek out safe, high dividends, something that’s particularly helpful these days, when the typical S&P 500 stock yields just 1.4%. Skilled newsletter writers can turn up these income opportunities in part because they have industry connections and access to tools most individual investors don’t. That, in turn, lets them get into corners of the market many folks may not even know about.

A good example of the kind of oft-overlooked investment a newsletter could turn up for you is a municipal-bond closed-end fund (CEF). These funds hold bonds issued by municipalities, states, cities and other public organizations for funding infrastructure. As such, they’re typically very stable, with minuscule bankruptcy rates.

What’s more, “muni-bond” CEFs are managed by experts in this market, which is what we want, because top managers often get the best pick among these funds. The big advantage of muni-bond CEFs is that they boast high yields that are also tax-free for most Americans. So a muni-bond CEF yielding, say, 4.4%, could amount to a 7% yield for you, depending on your tax bracket.

To give you another example on the income side, the portfolio of my CEF Insider service yields 6.6% today. On $5 million, that’s $27,500 per month, versus just $6,000 per month with the typical S&P 500 index fund. And you’re not holding anything exotic to get that dividend: CEF Insider’s portfolio contains funds holding the same companies you’ll find among the S&P 500 and is more diversified into less risky assets, including, yes, municipal bond CEFs.

Newsletters also tend to charge a lot less than a full-service advisor, and they certainly won’t charge you a percentage of your assets! You’ll instead pay a fixed subscription price, as you would on a magazine or newspaper.

Something to keep in mind with newsletters, however, is that they don’t provide personalized tax advice, so you’ll need to make sure you have a good accountant working for you.

A 3-Fund DIY Start

So let’s say you’ve found a good accountant and you want to go the newsletter route. What kind of funds are you likely to end up with?

If you’re an income investor, you’ll want a diversified portfolio with a large, reliable income stream, so the goal is to get a variety of stocks and bonds and high yields. A typically newsletter portfolio might look something like this:

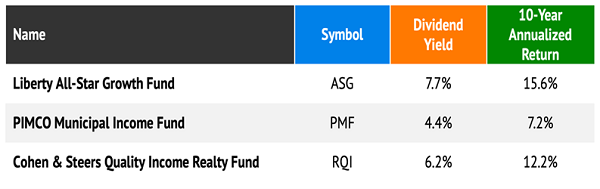

Here we’ve got tech-stock exposure through the Liberty All-Star Growth Fund (ASG); the PIMCO Municipal Income Fund (PMF), for muni bonds; and the Cohen & Steers Quality Income Realty Fund (RQI), which mainly holds real estate investment trusts (REITs). Combined, we’ve got three asset classes and a 6.1%-yielding portfolio (before accounting for PMF’s tax advantages). And these three funds have delivered a solid average annualized return of 11.7% on average over the last decade.

My 4 Top CEF Picks Yield an Incredible 7.7% (and Set to Soar)

Right now I’m urging my readers to buy 4 other CEFs that yield even more than these three: an outsized 7.7% today. And these funds are even better positioned for gains due to their unusually deep discounts. In fact, they’re so cheap that I’m calling for 20%+ price gains in the next 12 months!

That gets you a livable income stream on a reasonable nest egg—with, say, $500K saved, you could pull in a steady $38,500 a year in dividends!

Recent Comments