One group of funds is doing something very unusual right now: they’re raising their dividends by double digits! And those huge hikes have driven the yields on some of these unsung income plays well above 7%.

Today we’re going to jump on this red-hot contrarian opportunity.

These smartly run dividend payers (and growers!) are closed-end funds (CEFs) that hold floating-rate loans. These assets are often overlooked, which is too bad, because they’re corporate bonds that do the opposite of what most bonds do. That makes them perfect buys for upside in today’s market, when “regular” corporate bonds’ prices are plunging.

Let me explain how floating-rate loans work, and how we’ll squeeze them for strong gains and growing 7%+ dividends.

The Contrarian Income Seeker’s Best Friend

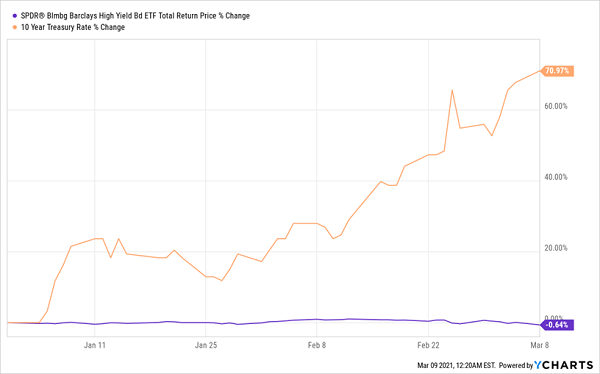

When inflation fears rise and interest rates go up, most bonds—especially corporate bonds—lose value. That’s why the SPDR Bloomberg Barclays High Yield Bond ETF (JNK), the benchmark for the corporate-bond market, has declined nearly 2% in the last month. Meantime, the yield on the 10-year Treasury note, which sets the tone on interest rates paid on everything from lines of credit to mortgages, has skyrocketed.

Yields Rise, Bonds Fall

That higher interest rate is due to inflation. Thanks to the recently passed $1.9-trillion stimulus package, a recovering economy and higher-than-expected consumer spending, economists warn that prices could rise above the sub-2% yearly rate we’ve seen over the last decade. And that’s caused corporate debt of all kinds to sell off.

But this is the kind of market in which floating-rate loans thrive.

There are two reasons for this. The first is that, unlike with the fixed rates of bonds, yields on floating-rate loans go up with interest rates. This is how two of the 21 floating-rate CEFs out there raised their dividends last month, and it’s why the other 19 will likely follow suit soon.

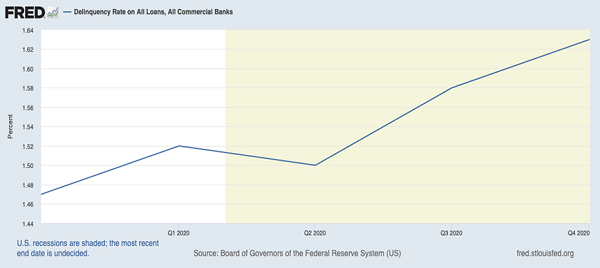

The other reason is not so obvious, but arguably more important, and it has to do with solvency. Interest rates rise in an improving economy, and an improving economy means businesses are less likely to default on their debts. Obviously, 2020 was a time when many businesses struggled to repay their loans, which is why delinquency rates rose by over 10% last year, despite the business-loan relief programs that were passed.

Coronavirus Adds Risk to Business Loans

But 2021 is different. For one, the $1.9-trillion relief plan adds even more money to help businesses keep up with their debts. And second, we now have vaccines quickly rolling out, so companies will see more customers coming through their doors. And that means floating-rate loans will likely see even higher demand.

Market-Busting Yields

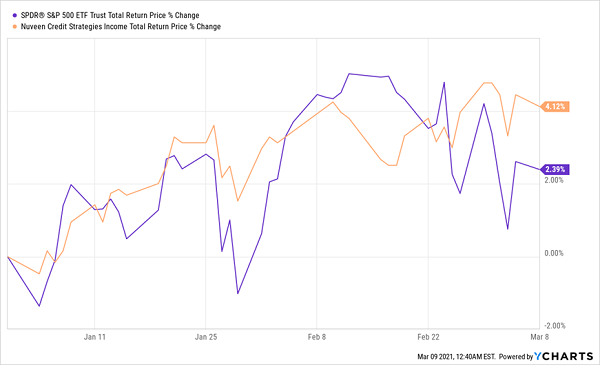

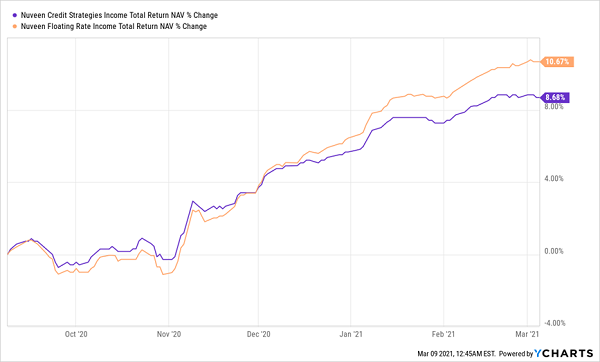

All of this makes floating-rate loans a great investment for upside in this environment, and as I mentioned earlier, their dividends are high—and growing—too. The biggest floating-rate CEF is also the highest yielding; the Nuveen Credit Strategies Income Fund (JQC) yields an almost-unthinkable 12.7%, and the fund, marked in orange below, has posted a total return that’s doubled that of the S&P 500 this year.

Floating-Rate Mania Is Just Beginning

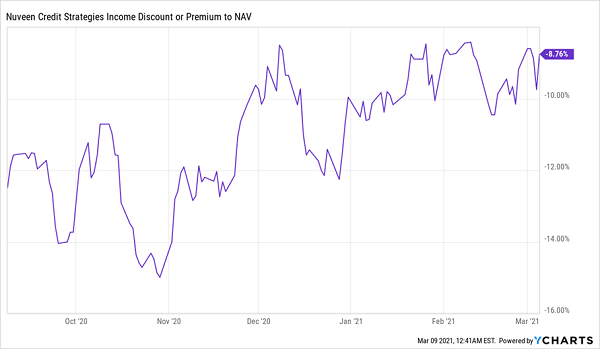

What makes JQC even more tempting is its 8.8% discount to net asset value (NAV). That’s another way of saying the fund trades for less than its portfolio’s intrinsic value. We can also see that its discount is steadily shrinking, and I expect it to keep doing so in the coming weeks.

A Sale on Borrowed Time

That makes JQC worth your attention if you’re on the hunt for a high current yield. But what about dividend growth?

That’s where the Nuveen Floating Rate Income Fund (JFR) comes in. Its 7.3% yield is lower than that of JQC, but its 7.9% discount is similar, and it just hiked its payout by a whopping 21%. Plus, if we look at the value of both funds’ portfolios, we see that JFR is doing a much better job of increasing the value of its NAV.

Dividend-Growth Star Tops the High Yielder

This outperformance makes JFR a good place to park some money and generate high dividends and strong growth amid a still-volatile stock market and inflation worries.

These CEFs Make Money 99% of the Time (and yield 7%+!)

JFR and JQC are just two of the many safe high yields you can get from CEFs. I’ve uncovered 5 more funds that pay big 7.5% yields now, and they trade at such unusual discounts that I’m calling for 20%+ price upside in the next 12 months as these unusual deals disappear.

Here’s something else you should know about CEFs: they’re among the safest investments out there, especially if you focus on the oldest and most well-established funds (which we always do!).

Get this: of the 330 CEFs that are a decade old or older, only 14 have lost money in the last 10 years.

That’s a 96% win rate!

What’s more, of those 14 funds, 11 were in the energy sector. Dump those laggards and these CEFs’ win rate jumps all the way to 99%!

My 5 best picks from among these money-making CEFs are waiting for you. Go here and I’ll share my full research on each of them, including names, tickers, best-buy prices, discounts, complete dividend histories and more.

Recent Comments