Can we income seekers safely get back into REITs (real estate investment trusts) next year?

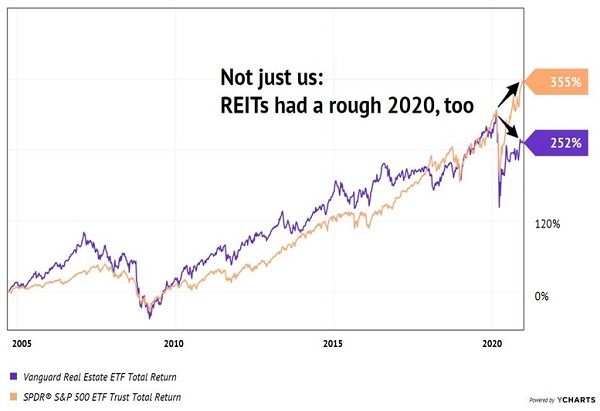

With the yield on the S&P 500 about to drop to a sad 1.5% (thanks, Tesla (TSLA) addition), renewed REIT-hope sure would be nice! The landlord industry index Vanguard Real Estate ETF (VNQ) pays 3.5%. That’s a dividend oasis in this zero-point-nothing world.

Once upon a time, VNQ performed in-line or better than the blue-chip index. It was a pretty good deal, as you could double your dividend and keep up with the Joneses’ portfolio with less heartburn.

Then, April 2020 came along, tenants stopped paying rents, and REITs-at-large got crushed:

A Good REIT Run While It Lasted

Does the fork-in-the-road above represent a paradigm shift or relative value? It depends on the tenant.

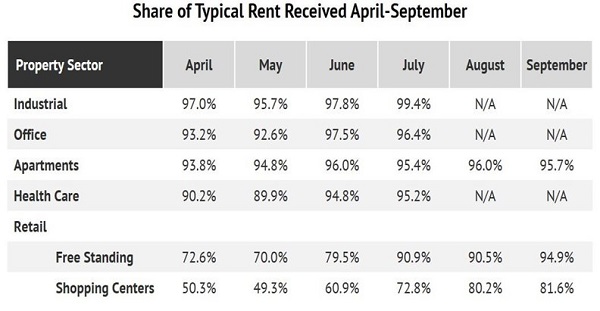

In April, the National Association of Real Estate Investment Trusts (Nareit) began collecting information on rents by property sector. They ranged from fine-throughout (Industrial) to still-disastrous (Shopping Centers):

Source: Nareit

The “N/A” you see above for August and September next to Industrial, Office and Health Care properties is actually a good thing. Nareit became so confident in these collections that it got lazy and stopped bothering to collect this data.

Which means, if we’re thinking about the best REITs for 2021, we should start with these sectors. Let’s discuss them and highlight a few ideas before moving on to the problem children.

Industrial REITs: 2019-Quality at 2020 Prices

I’ve always liked Industrial REITs thanks to the strength of their cash flows. Take W.P. Carey (WPC), which leases out business space to individual tenants. Its portfolio is diversified across 1,216 properties, with its largest tenant (U-Haul) making up just 3.4% of its total portfolio.

Virtually all of WPC’s leases include contractual rent increases. And 62% of them are linked to the consumer price index (CPI), which is a nice hedge for those of us who are concerned about inflation down the road.

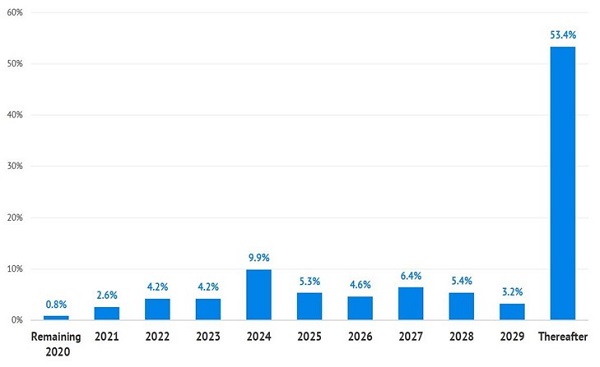

WPC’s leases are long ones, too. The average length (weighted by value) is 10.7 years. If you’re convinced we’re mired in the Great Depression II, this is the lease portfolio for you. Only 3.4% of WPC’s contracts expire before the end of 2021!

Upcoming Lease Expirations (or Lack Thereof)

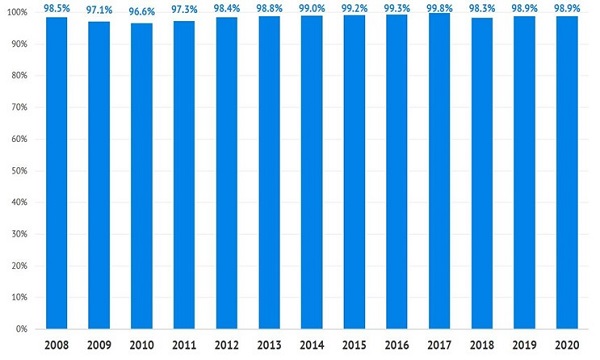

Occupancy, meanwhile, never seems to dip. This is no accident. In the words of CEO Jason Fox, WPC is a picky landlord that only extends leases to companies in industries that can withstand “dislocations in the market.” Its underwriting team is acing its second dislocation test.

During its first major test, the firm’s occupancy rate held strong through 2008 at 98.5% and merely dipped to 96.6% in 2010. Through the first two quarters of stressful 2020, its properties are humming at an incredible 98.9% occupancy (same as 2019 levels):

Occupancy (% Square Feet) Staying Strong

WPC pays a nice 6% today, a fatter yield than mega-Industrial REITs:

- Prologis (PLD) pays 2.7%,

- Duke Realty (DRE) 2.5%, and

- Americold Realty Trust (COLD) 2.3%.

PLD and COLD in particular appear to have peaked earlier this year. These stocks became quite expensive with respect to cash flow, and investors now seem to be questioning if these landlords were really worth their premium valuations (hint: probably not).

Office REITs: Be Careful

In 2003, I got my first office job—and hated it.

Fast-forward to 2008, after two years of working from home—I hated that.

The following summer, I rented a converted motel room (no joke) to house myself and my startup’s summer intern. Eleven years and four (increasingly comfortable) offices later, you won’t find me without a non-home office.

The View From My First Desk

I have experimented with many combinations of “home versus office” work combinations over the past dozen years, and the ideal mix is somewhere in between for most people.

With many information workers trapped in their housing cells for most of 2020, they are looking forward to a return to the office. The first time they commute, they are going to ask themselves: “Why?”

Similarly, many Office REITs have rallied furiously. Investors who keep holding these names may soon be asking themselves: “Why?”

Beware blue-chip names in the sector like Boston Properties (BXP). I have nothing against the way these companies are run—but I worry that their business models may be at least partially obsolete.

Alexandria Real Estate (ARE) and SL Green Realty (SLG) are two more dividend growers to keep an eye on in 2021. If they can “cross the chasm” to our post-virus world, we’ll consider them. More evidence is required, however.

Healthcare REITs: Buy on Pullbacks

Healthcare REITs (or, as Nareit calls them, “health care”), are more attractive than Office landlords from an income standpoint because, as with WPC, we can find some secure rent collectors paying 5% or more.

For example, Physicians Realty Trust (DOC) focuses on medical offices. The company has collected 97% or more of its rent every month since the lockdowns began and boasts a 96% occupancy rate as I write.

And there are reasons for more upside. For one, many of DOC’s properties are aimed at outpatient care, which is growing fast as more procedures are done outside hospitals. Ambulatory surgical centers (ASCs), which provide day procedures or those requiring a short stay, are a good example: Deloitte sees the ASC market growing 6% annually through 2023.

DOC yields 5% today, and its cash flow easily supports its payout. With that yield and price stability—DOC sports a five-year beta rating of 0.81, making it 19% less volatile than the S&P 500—we’ve got a potential “bond with upside” setup here.

I would also keep an eye on skilled-nursing REIT Omega Healthcare Investors (OHI) and hospital landlord Medical Properties Trust (MPW). They pay 7.2% and 5.2% respectively. Their stocks tend to swoon once a year or so—even in normal years—so another buying opportunity may be ahead in 2021 (provided that these firms can keep collecting rents, of course).

Meanwhile, Sabra Healthcare (SBRA) is a bit too erratic for my taste. The firm’s dividend was cut in 2020, and its payout and share price sit lower today than they did five years ago. No thanks.

Apartment REITs: Be Picky

Apartment tenants are still paying their bills at a respectable clip—nearly 96%—last we heard. Who’d have guessed? (Not the “first-level” thinking crowd!)

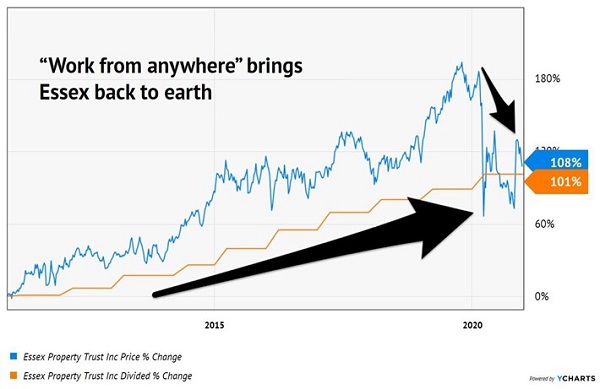

As rents received go, so go the accompanying REIT dividends. Essex Property Trust (ESS) has been a great apartment name to own. It’s doubled its dividend (+101.2%) over the past decade.

Essex rents to the high-earning tech brainpower that makes Google, Amazon and Facebook run. Its 240+ apartment complex footprint is focused on Northern California (42% of income), Southern California (41%) and Seattle (17%).

Essex yields 3.6% today, which is on the high end of its historical range. One concern I have with these apartment markets, though, is (again) the smooth transition from the home office. What happens to rental prices when the tech sector officially admits that you can be just as efficient working from home (in another city, state or even country?)

This Dividend Double Sobers Up

There are already reports that San Francisco rents are falling fast (by their standards). I left SF myself in 2007, cut my cost of living and improved my quality of life to boot. Cheaper cities, states and suburbs should benefit if a distributed tech workforce is here to stay.

Few apartment REITs yield 5% or 6%, so we would be buying them for the potential growth of their payouts. Right now, that picture is a bit too murky. Stay away from leading names such as Equity Residential (EQR), AvalonBay Communities (AVB) and UDR (UDR) for now. All three yield between 3.9% and 4.2%, which is not enough to compensate for their price risk in my opinion.

Retail REITs: Please, Just Don’t

Brick-and-mortar locations have looked dicey for years. They earned my “worst REIT award” nearly four years ago, and since then, business has gone from kind of crummy to downright dreadful.

Commercial landlords are spending the holidays in denial, holding rents high while hoping for a miracle in 2021. But we don’t bet on hope here, we wager on cash flows. With in-person retail aging in dog years, we’re going to take a pass on this entire property sector.

Realty Income Group (O), National Retail Properties (NNN), Cedar Shopping Centers (CDR), Simon Property Group (SPG) and KIMCO Realty Group (KIM) are the dividend traps to watch here. Sure, we can trade them and scrape some profits if we stay for a few months. But these aren’t the types of stocks to sock away and ignore while their rent collections evaporate.

My #1 Income Play for 2021

You’re probably noticing a theme by now. The best REITs are “all-weather assets” that deliver income whether stocks soar or crash.

And the truth is, the markets could go either way in 2021. So, what specifically should we do with our money?

My #1 income play for 2021 delivers maximum returns and dividends with minimum risk, no matter the road ahead environment. Click here for more details on my #1 dividend investment for 2021.

Recent Comments