To retire on dividends, we have just two requirements. They are simple, though perhaps not exactly easy:

- Earn safe, meaningful yields. Five percent is our floor, thirteen is our stretch goal. We’ll discuss five stocks in this dividend range shortly.

- Keep our principal intact. To do this we’ll focus on “low beta” stocks—shares that move less than the broader market.

Beta says how much (or how little!) an investment moves compared to some benchmark. With stocks, beta is usually going to measure movement against the S&P 500.

Here’s an example. Let’s say a stock has a beta of 0.50. That means, broadly speaking, when the S&P 500 drops by 1% in a day, the stock will probably only drop by 0.50%. It’s not a perfect relationship—it won’t work out that way exactly on a daily basis—but over time, lower-beta stocks typically have much calmer stock movement.

Low Volatility: A Smoother Ride

Let’s highlight five low-vol payers—with dividends between 5% and 12.8%–that can provide long-term stability while funding our payout-powered retirements.

Low-Vol High Yielders

Amcor plc (AMCR, 5.0% yield) is an out-of-the-ordinary safety pick, largely because it’s part of the heavily cyclical materials sector and it’s tied pretty closely with consumer companies.

Thing is, Amcor makes packaging. Shrink bags, lidding films, custom bottle caps, you name it. That means weakness in any one consumer category isn’t necessarily going to punish AMCR. Weakness in a lot of consumer categories, however:

Amcor Is Separating From the Pack. Not in a Good Way.

Sure, some of AMCR’s weakness can be chalked up to difficult comps as well as lost business in Russia. But the real problem is weaker consumer demand, which analysts expect could persist through at least next year. Amcor has been aggressively cost-cutting in response, however, trimming $140 million so far this year and gunning for as much as $60 million by the end of the fiscal year.

Amcor could get worse before it gets better. But it’s a 5% yielder whose one- and five-year betas both stand at 0.85, which is modestly less volatile than the broader market. And it’s a Dividend Aristocrat to boot, boasting four consecutive decades of uninterrupted payout growth.

International Business Machines (IBM, 5.2% yield) is a younger Aristocrat with 28 consecutive years of annual dividend hikes. It also sports a 0.85 five-year beta, and it’s been even calmer more recently, with a one-year beta of 0.62.

IBM, like many large firms, recently announced a slew of artificial intelligence (AI) initiatives. It’s the Wild West out here, and given the disappointment of IBM’s Watson, it’s fair to be at least a little skeptical over the potential for its AI WatsonX Platform. But given AI’s heralded “quality” of being a massive job killer (er, redundancy-eliminator), IBM could see some pickup. Heck, the company thinks it can eliminate 28,000 of its own employees with the technology.

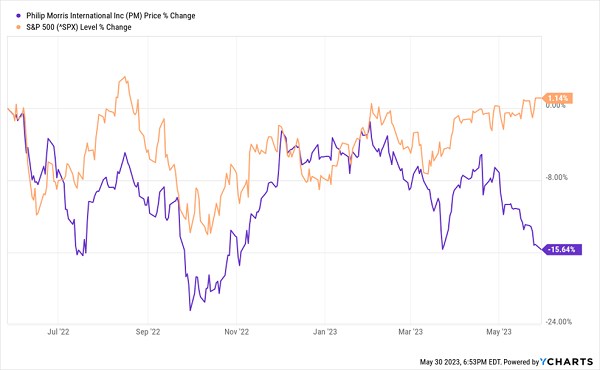

Down the road, that might be a worry for Philip Morris International (PM, 5.6% yield)—after all, robots don’t smoke (or consume anything, for that matter). For now, shareholders’ primary concern is weak second-quarter guidance that sent shares off track:

PM Burns Out

Even then, the tobacco giant is guiding for high-single-digit organic sales and profit growth this year, with most of it relying on a pivot in the second half. Especially promising is growth in the company’s heated and oral tobacco lineup.

Meanwhile, shares are cheaper than most of PM’s consumer staple peers, the yield is well north of 5%, and one- and five-year betas of 0.75 and 0.71, respectively, reflect continued relative stability that investors should expect going forward, too.

Omega Healthcare Investors (OHI, 9.0%) screams for a second look based on yield alone. This real estate investment trust (REIT) is a triple-net lease firm that provides financing and capital solutions to operating partners in the skilled nursing facility and assisted living facility industries.

Like the rest of its industry, Omega was hammered during the pandemic. COVID wreaked havoc through nursing homes and assisted living, dragging related REITs lower by 50%, 60%, 70%, sometimes more. And while shares have stabilized over the past year or so, OHI still is worth less than two-thirds what it was at its pre-COVID peak. And its dividend of late has outstripped funds from operations (FFO) and funds available for distribution (FAD).

Those with patience might prevail. Omega still has a healthy balance sheet, and the business is finally seeing some light at the end of the tunnel. OHI has concluded with a series of restructurings, and rent is flowing in from those tenants once more. The stock is stabilizing, too—its five-year beta is just a hair under 1.0, but OHI has been less than half as volatile as the market over the past year.

A brisk takeoff ahead? Maybe not. But most of Omega’s problems are no longer on the horizon, but in the rear-view mirror.

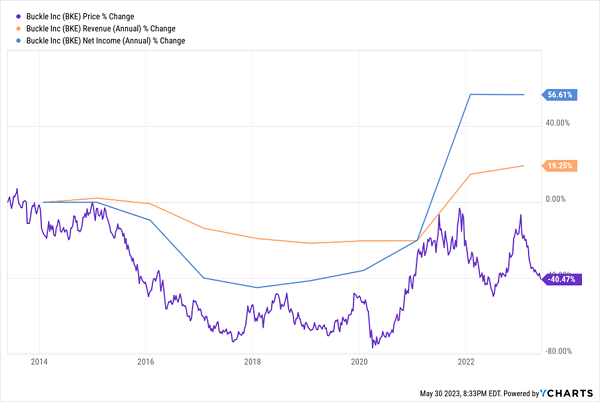

Fashion is fickle, but that has worked to Buckle’s (BKE, 12.8%) advantage over the past couple of years. The fashion retailer of mid- to higher-end clothes, accessories and footwear has become trendy once more, leading to an operational renaissance of late.

Unfortunately, That Renaissance Hasn’t Applied to Shares

The good news? Buckle technically has been less volatile than the market over the past year and the past half-decade. But the stock is slumping hard because it’s looking like a binge in denim and other Buckle staples was merely unleashed pent-up demand. The current year’s profits are expected to taper back by 13% YoY, then remain level in 2024.

But, oh, that dividend, right? At nearly 13% (from a retailer, no less), who could resist?

It’s a bit deceiving. The majority of that yield is a reflection of the company’s special dividend. BKE’s regular dividend comes out to about 4.4%; the rest came from Buckle’s most recent special payout.

To be fair, though, BKE has compiled a history of special dividends over the past few years, delivering a decent baseline, then topping out as much as it can, when it can. Investors have enjoyed extra payouts roughly once a year for some time now.

How to Retire on Just $500K

It’s a responsible way to deliver income, albeit too undependable. Buckle’s expected decline in earnings, for instance, should all but ensure a smaller special payout should BKE announce another one in the next year or so.

If you’re younger and just looking to maximize total returns, then Buckle might be worth a roll of the dice.

But if you’re looking to maximize your retirement portfolio’s income potential in a sustainable way right now … you need to do better.

Simply put, your goal should be to generate at least 8% in reliable dividends—not specials, not fixed-and-variables, but boring, beautiful, regular dividends.

Why 8%? Because that number will allow you to retire on dividends alone, even if you have a smaller nest egg—say, a mere $500,000 to work with.

Here’s the math: At 8%, you’re generating $40,000 in cash from your retirement account alone. Combine that with Social Security, you’ll have plenty to work with once you’ve moved on from your career.

And if you have an even bigger pile of cash to plug into our 8% “No Withdrawal” Retirement Portfolio, you’re looking at a downright cozy retirement—one where you may never have to touch your original nest egg!

The low-volatility stocks above don’t quite fit the bill. But I have plenty of stealth payout plays that do yield the 8% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends up to 11%!

Recent Comments