It’s a new year, and that means a lot of suggestions for new approaches to investing.

But here at Contrarian Outlook, we’re not interested in change as the illusion of progress. We’re only interested in one thing – long-term investments that allow us to retire worry-free!

So don’t worry, friends… no gimmicks for you today! Just another case-study in our proven investing strategy.

As I have outlined in previous analysis, my go-to income investments are what I like to call “MVP” stocks. Those are companies that have strong Management, an attractive current Valuation for shares, and generous and sustainable Payouts to provide reliable income.

Here are a few prime examples from the last several months:

- Walgreens Boots Alliance (WBA) – 5.2% yield, up 18% since recommendation

- JPMorganChase (JPM) – 2.9% yield, up 21% since recommendation

- Stellantis (STLA) – 6.5% yield, up 27% since recommendation

Considering the typical S&P 500 stock yields just 1.7% and the index returned a loss of -19% in calendar 2022, the power of this strategy should be clear…

So why change course?

My latest MVP recommendation is “experiential” real estate investment trust VICI Properties Inc. (VICI). Here are the specifics about VICI that make it worth a look right now, and how it can fit in with your income investment portfolio:

VICI – Our Latest MVP

VICI Properties is a nearly $35 billion real estate investment trust that owns one of the largest portfolios of gaming, hospitality and entertainment destinations in the world. Its flagship is the world-renowned Caesars Palace, but its total portfolio includes roughly 50 million square feet of properties, more than 19,200 hotel rooms and more than 200 restaurants, bars and nightclubs.

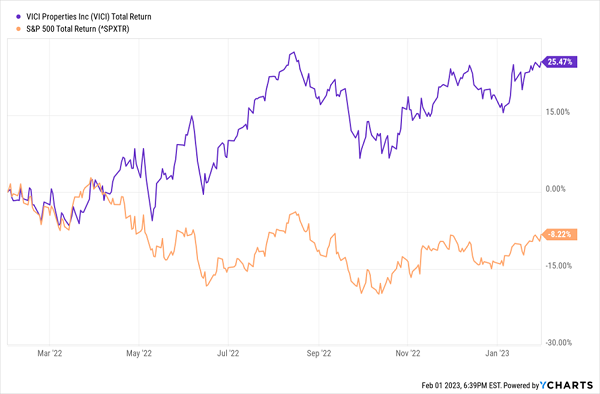

There’s obviously risk here, even in a post-COVID world. Fears of consumer spending pullbacks have weighed on many discretionary names over the last several months. But VICI has clearly sidestepped that volatility with a 12-month gain of almost 26% while the S&P 50 has lagged far behind.

That’s in part because VICI is one of those enviable “triple-net lease” properties where tenants have to pay taxes, insurance and upkeep. That helps insulate the company a bit from short-term volatility as it’s only concerned with long-term leases with top-tier clients.

That has kept VICI solid from a structural perspective. But as for specifics in 2023 that make this stock a buy right now that’s worthy of your attention, let’s run through our three MVP factors with this stock…

Management

Thanks to a revitalization of operations, VICI is tracking a phenomenal 70% revenue growth to close out fiscal 2022. Earnings won’t be released until late February, however, so there’s time to front-run what could be a blowout report. And looking forward, there are predictions of 27% growth for 2023 – even in the face of fears about the impact of weaker consumer spending.

But if you want some specifics as to how management is planning for this growth, consider that VICI Properties just closed on a deal to acquire the other half (well, 49.9% stake) of the joint venture that owns the MGM Grand Las Vegas and Mandalay Bay Resort from Blackstone. The deal ain’t cheap, at about $1.27 billion, but consider the deal VICI got. The company took on the remaining debt, maturing in 2032, with an interest rate of 3.558%. As 30-year mortgage rates approach 7%, this deal looks amazingly shrewd – and amazingly well-timed to fuel future growth at a reasonable price.

Oh yeah, VICI also owns 34 acres of prime, undeveloped land adjacent to the Las Vegas Strip that could come in very handy in the years ahead.

When it comes to REITs, responsible management of capital and investment is key. VICI seems to have that going on in spades.

Valuation

There is admittedly a bit of risk here given consumer spending concerns, which is part of the reason investors are going to get a fair price for shares. But most importantly, when you compare apples to apples it appears that VICI is as good a bargain – or even better – than its peers.

VICI has applied the “triple net” leasing model to its experiential real estate assets, which means its tenants are responsible for all the maintenance, taxes, and other expenses required to actually operate the properties. While this form of leasing has clear benefits to the landlord, it is sometimes criticized for creating “commodity” type real estate where often so much value can be ascribed to the contractual lease payments over the term of a given lease, that an investor can end up paying a price for a triple-net-leased asset that ends up representing a premium to its replacement cost.

But VICI has managed to buck this trend, with one example being their acquisition of The Venetian Resort last year which the company acquired at approximately $300 per square foot. Management has suggested this price represented a whopping 62% discount to its estimated replacement cost. And that deal came with 80+ acres of land as a bonus. VICI now collects an initial annualized rent of $250 million on an initial term of 30 years, with annual escalators set to trigger when the resort’s net revenue returns to pre-COVID levels; the rent will then start bumping higher each year by at least 2% (and up to 3% depending on the level of change in the CPI). Against its $4 billion investment, that’s a 6.25% “yield” from a triple-net lease, with rent growth on the horizon as an added bonus.

Payouts

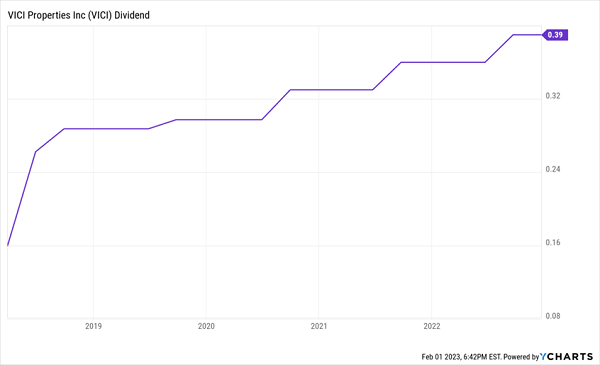

At the beginning of 2018 at its IPO, VICI paid 16 cents per share each quarter and has only gone higher since then. After a 3-cent bump in payouts last year, the company now pays 39 cents per quarter. That’s more than 140% more in dividends, after just five short years! What’s more, just before Halloween VICI posted quarterly funds from operations of 49 cents per share that easily cover that payout. And that comes after its earnings in May where the casino giant upped its full-year estimate for FFO to $1.92 a share – a forecast it reaffirmed late last year.

That means even with an above-average yield of 4.5%, which is almost 3X the average dividend of 1.7% for the S&P 500 right now. VICI has a history of big increases, as well as a dividend that is very secure and perhaps ready for even more increases in the months ahead.

Stick to What Works in 2023

While it’s not always easy to identify an MVP like VICI, these rare dividend stocks are definitely out there if you know what to look for – and if you are patient. That means not lowering your standards or changing strategy on a whim just because of the latest headlines.

A focus on stable stocks that offer long-term income is the only way to ensure you have a safe retirement. Buy good stocks at a great price, lock in generous dividends, and sail into the sunset without worrying about day-to-day gyrations on Wall Street.

It’s what we like to call the “No Withdrawal Portfolio.”

The 15 or 20 stocks that make up this exclusive Buy List may change year to year based on circumstances , but the proven, underlying strategy is the same. And it’s deceptively simple:

- Forget “buy and hope” investing in vanilla index funds, or an antiquated 60/40 portfolio,

- Prioritize MVP stocks that have strong outlooks, fair valuation and supersized yields, and

- Protect your principal and ignore bear markets with a “No Withdrawal” approach.

We’ve just published 2 Special Reports detailing this powerful, low-risk retirement strategy – full of picks with even brighter outlooks and bigger dividends than VICI. In these publications, you’ll find all the details – including rock-solid dividend investments that offer yields of as high as 10%, or more!

Don’t fall victim to the fear of 2022, or the “flavor of the month” strategies that are making the rounds in early 2023.

You have to stick to your guns and be selective in this environment… but you don’t have to settle for yields that are half of what you deserve.

Recent Comments