What’s better than a 9.3% dividend stock? How about one that’s poised to pop as interest rates rise?

Business development companies, or BDCs for short, are overlooked by most income investors. That’s too bad for them because these dividend deals can be pretty sweet.

Especially when rates are rising.

BDCs cut loans to small businesses. Their inflation-friendly component comes from floating rate loans. BDCs that lend this way make more money when rates rise.

BDCs came to life in 1980 when Congress whipped up these tax-advantaged entities. Like the REITs we all love, BDCs are cleared by Uncle Sam for tax-free profits, provided they dish most of their green as dividends. Hence the 9.3% yield provided by Hercules Capital (HTGC), which has been our inflation play of choice in this sector.

Nine-plus percent dividends are great when enjoyed responsibly and in harmony with macro trends. Fortunately an amazing 94% of HTGC’s investments are floating rate loans—with interest rate floors. HTGC makes money all the time, but even more when rates rise!

Chief Financial Officer Seth Meyer recently commented that as the Fed hikes, the “timing” for HTGC’s higher profits is “pretty instantaneous.”

The beauty of floating rate loans! Powell plays catch up and HTGC goes ka-ching!

HTGC boasts many cutting-edge technology clients. Previous clients included social media darlings Meta (the artist formerly known as Facebook) and Pinterest. It also lends to technology, life science and sustainable and renewable energy firms like:

- 23andMe, a consumer DNA genetic testing company

- Postmates, an online delivery and pickup services app

- Bicycle Therapeutics, a biotech developing treatments for unmet needs

HTGC had record “spillover” earnings of $1.65 in 2021. This is extra cash that the firm collected from its loans, but doesn’t need!

The extra cash inspired a special dividend of $0.60 per share, dished out in $0.15 quarterly increments (boosting the forward yield above 10%!)

The firm’s “goal” is to reduce spillover to $1 per share by year end. But even the three more special payouts may not dent the cash mountain. Spillover is likely to climb by year’s end.

HTGC’s eye for good credit is outstanding, too. The firms’ dividend took only a modest breather during the ultimate “stress test” of 2020, then resumed its climb.

This all sounds great. Which begs the question: “Why are shares of HTGC down in recent months?”

Stop me if you heard this before, but it’s the Federal Reserve’s fault.

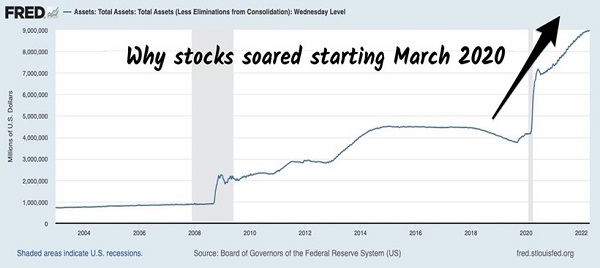

The Fed is cleaning up its own mess. Prior to the pandemic, the agency had $4 trillion on its balance sheet. That soared to nearly $9 trillion, why stocks soared starting in March 2020.

$5 Trillion in Easy Money Flowed to Stocks

The thing about freshly-printed money is that it tends to find its way into asset prices quickly. It flowed directly into the stock market, housing market, and cryptocurrencies. They ignited a speculative bubble that began to deflate in March 2021 (when many stocks quietly peaked and began to roll over).

The average NASDAQ stock is way down. Most tech stocks rely on easy money and low interest rates—both of which are “over” for the moment.

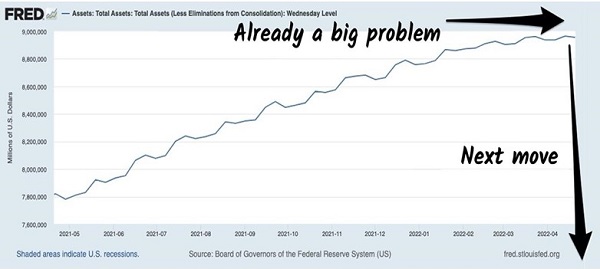

One week from today, the Fed will officially begin to taper its balance sheet. Its $4 trillion pile rocketed nearly to $9 trillion. The slowing growth has already been a big problem for stocks.

I’m concerned what the post-June 15 belt tightening will bring. Especially for the easy-money-addicted NASDAQ.

Fed’s Balance Sheet Moves Down Next Week

Why’d we get off on a NASDAQ tangent when we were talking HTGC? Well, the BDC lends to tech companies. A crashing NASDAQ weighs on HTGC’s stock price. It sops up the liquidity that the tech sector thrives upon.

Fundamentally, this correlation—between the price of the QQQs and HTGC’s underlying business—may be a stretch. But that’s how bear markets have operated over the past 14 years.

Energy is the only sector defying gravity this year. (Hate to say it but that’s how 2008 started, too.)

I don’t think we’re going to see another financial crisis. But we’re in a bear market, and it is very difficult to stock pick our way to the other side of the bear.

We contrarians recognized early that the stock market was likely to break down in 2022. That’s what has happened.

The downdraft has taken some perfectly fine stocks—like HTGC—with it. It happens in bear markets. The good news is that these declines don’t last forever.

Our goal is to keep our capital intact between here and there so that we can buy some great bargains this fall, or whenever the equity prices finally bottom. If recent history is any guide, more stocks than not will find their ultimate floors on the same day.

Until then let’s stash cash and stay calm but realistic about the stocks we do still own like HTGC.

If we have to sell HTGC at some point and buy it back later, that’s what we’ll do. For now we’ll keep an eye on those lows from May to make sure that they hold.

Which, by the way, is a fair strategy for any dividend stock. If the previous lows don’t ultimately hold, that will be a sign that something worse is on the way this summer. There’s no reason for us to grit our teeth and bear the bear. I’d rather stuff cash in my favorite safe fund (under my mattress) and go on a shopping spree when we reach the other side of this mess.

This raging inflation really is bringing a 50-year retirement income storm. We long-term income investors are forced to focus on factors like the Fed and NASDAQ—things we don’t typically concern ourselves with.

Which is why I put together an inflation-protected portfolio that is worry free. Please click here and I’ll share my favorite dividend stocks to buy now.

Recent Comments