The stock market keeps falling and falling because, for the first time in 14 years, there is nobody there to catch it.

The “Fed put” has expired.

The genesis of the Federal Reserve’s implicit put—the notion that the Fed will fix any decline—was the 2008 Financial Crisis. The financial system was on the ropes and the stock market itself became “too big to fail” as far as the Fed was concerned. Then-Chairman Ben Bernanke printed a bunch of money, boosted the market and was heralded a financial hero.

Since then, the Fed has been reluctant to let the stock market drop. Anytime the S&P 500 has a hiccup or correction, the central bank has stepped in to print money, and this liquidity stabilizes stock prices.

This implicit “insurance” has been called the Fed put. It’s a word play on options investing.

When we buy puts, we are generally buying insurance on our portfolio. Puts rise in value as stock prices drop. The Fed kindly provided US investors with—in effect—complimentary portfolio insurance (a put) for the past 14 years!

The Fuel Behind the Fed’s Put

This floated a bull market in which investors rarely worried about stock prices going down. Anytime the S&P 500 (“America’s ticker”) dipped, there was no need to fear. The Fed would cut rates, accommodate, and do what it had to do to keep the market from tumbling.

It seemed like the easy money would last forever. Heck, I shrugged off nearly every market concern for this reason. Why worry when we know that the Fed will just paper it over?

On repeated Contrarian Income Report webcasts I cited the Fed as the ultimate catalyst for stock prices. Geopolitical tensions, virus numbers and domestic political unrest couldn’t weigh stocks down while the Fed printed money.

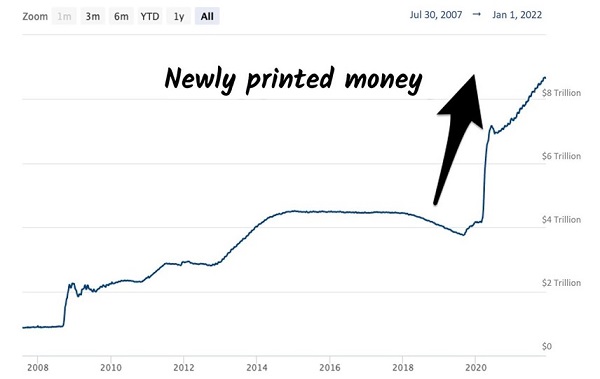

But Jay Powell finally overdid it with this 2020-inspired balance sheet explosion:

The Fed Just Printed $4+ Trillion!

That guy knows how to throw a party! No wonder consumer prices went bonkers. There’s a ton of cash chasing a fixed amount of goods.

The biggest threat to Powell’s job security is inflation. He must make a choice between Main Street and Wall Street. With push coming to shove he’s sacrificing the stock market to bring inflation down and save himself.

Skyrocketing inflation forces Powell to sop up his flood of money. “Paging Mr. Chairman for a cleanup on aisle five (and six, and seven, and…)!”

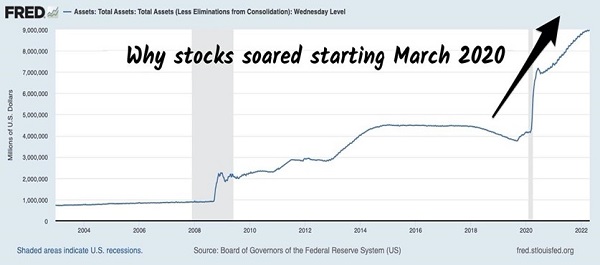

Powell’s monetary moonshot previously ignited a bull market. Unfortunately, he must now take away the punch bowl and hook intoxicated investors up to saline IVs. The headaches are already setting in and the party hasn’t even officially ended yet.

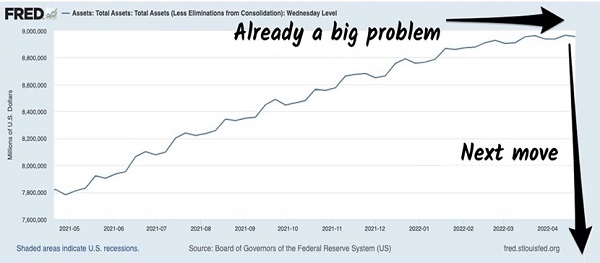

The slowing of the agency’s massive money printer has already caused the broader stock market to, ahem, correct. But the real capital cleanup is yet to come. The Fed is supposed to remove $1 or $2 trillion from its balance sheet at the rate of $95 billion a month!

How do we think that’ll go?

Next Up: The Hangover

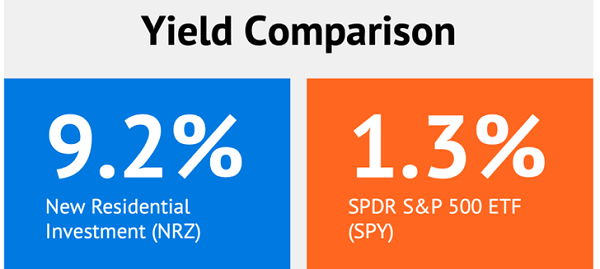

There’s probably more pain to come. Which is why we should seek out inflation-friendly dividends. Like the payer we discussed two weeks ago, New Residential Investment (NRZ).

NRZ rewarded us with a “Contrarian Outlook told you so” earnings report last week. Book value jumped 10%—a whopper!—and shares followed suit. Investors enjoyed 9% total returns in two weeks while the stock market at large unraveled.

What is NRZ’s secret? How can it soar while the market sinks?

The firm owns a boatload of mortgage service rights (MSRs). These gain value when refinancing activity slows, which is happening right now while long rates jump. US mortgage rates have risen above 5% to their highest levels since 2009.

MSRs are therefore worth more because home refinancing is over for now. The best business is servicing existing loans. NRZ owns the rights to these gravy trains. Which means the firm’s book value—and stock price—should continue to rise.

If you can stomach a yield of “only” 9.2% (ha!), then NRZ just may be a better play than the most popular ticker in America, SPDR S&P 500 ETF (SPY).

NRZ is the type of dividend payer we want to own to protect us from the inflation retirement storm that is on the way. If you didn’t buy it two weeks ago, well, you missed out on a quick 9%.

Fortunately, we have a few more that haven’t yet rallied. Click here for my full “inflation retirement storm” dividend stock list.

Recent Comments