In recent weeks, we’ve discussed proven strategies for protecting and growing our nest egg (and dividends) in this crisis. These are the times when fortunes are made and big income streams are built. However, we must be extra careful about our purchases, with plenty of “payout landmines” suddenly spread around the market.

In last Tuesday’s article, for example, we covered the most powerful indicator of dividend safety: the payout ratio, specifically dividends as a percentage of free cash flow (FCF). Unlike net income, which can be manipulated, FCF is the clearest picture of the cash a firm is generating.

That makes the FCF payout ratio the perfect one-step test to run on your holdings. And if you discover any paying out more than, say, 50% of FCF, you should consider selling, especially if the company is in a sector—like travel—that will be on the mat for many months (if not years).

By doing so, you’re benefiting in two ways:

- Protecting your income (and nest egg) from snap dividend cuts and,

- Freeing up cash for the many bargains headed our way. (It’s a given—I’ll be flagging these deals in my Contrarian Income Report service.)

I can’t stress that second point enough: every bear eventually gives way to a bull—and your portfolio will bounce right back when it does. So today we’re going to get a head start with three stocks perfectly positioned to roar back faster than the market.

In particular, we’re going to focus on dividend-paying tech stocks, because these companies have the biggest cash reserves out there. That will help them weather this crisis and keep paying their bills (and dividends!) even if business drops off.

We’re not going to stop there, though. We’re also going to test our tech plays’ resilience by looking at how they did in the best parallel to today’s crisis that we have: the 2008/09 meltdown. That’s because many of the companies that will rebound faster from this crash will be the same ones that did so in the last meltdown.

3 “Recession-Fighter” Tech Dividends to Target

Let’s dive into our three “recession-fighter” stocks: all racked up double-digit gains (at least!) from the time the S&P 500 hit its pre-crisis peak on October 9, 2007, until it regained those heights six years later, on April 9, 2013. And all three have fallen much less than the market in this latest crisis, too.

That makes them reliable buys to give your portfolio extra ballast, strong upside when this outbreak passes and safe—and rising—dividends throughout.

Our 3 “Recession-Fighter” Tech Plays

“Recession-Fighter” Dividend No. 1: Crown Castle International (CCI)

If you’re looking to play the surge in mobile-data use triggered by this shutdown, CCI is the way to go: the real estate investment trust (REIT) is a “toll bridge,” charging its users—including AT&T (T), Verizon Communications (VZ), T-Mobile US (TMUS) and Sprint (S)—“rent” to use its 40,000+ cell towers.

Unlike other REITs—I’m looking at you, shopping mall owners—CCI won’t have to worry about missed payments, because its clients’ services remain in high demand.

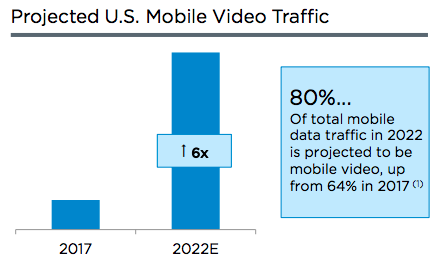

And once this period of self-isolation is over, I expect the numbers on mobile-data consumption to be astronomical, and they’ll keep rising as the work-from-home trend accelerates. That’s on top of data use that was already surging pre-crisis. Check out CCI’s projection on mobile-video alone from back in fall 2019:

Source: Crown Castle November 2019 investor presentation

That’s a clear opportunity for Crown Castle. And as you can see below, the stock has shown resilience in this pullback, falling much less than the S&P 500 as of this writing:

CCI Outperforms in a Crisis

History suggests it’s poised for strong upside, too: as I showed you in the table above, CCI soared 86% in the ’08 meltdown, just in the time it took the market to get its head back above water.

Meantime, we can buy CCI for less than 24-times 2019 funds from operations (FFO, a better measure of REIT performance than FCF or EPS). That might sound steep, but it’s low for this REIT, whose share price is always racing to catch its FFO (which jumped 9% in 2019). If you’d bought on February 21, you’d have paid almost 30-times FFO.

What’s more, CCI’s dividend has risen sharply, up 242% since it initiated the payout in 2014. And even though its payout ratio looks high, at 84%, that’s reasonable for CCI, whose clients sign up under long-term contracts (its weighted average remaining contract term is five years).

“Recession-Fighter” Dividend No. 2: Equinix (EQIX)

Equinix, like CCI, provides IT infrastructure that businesses can’t do without—in this case the data centers housing the servers companies need to keep running. Equinix is a pioneer in the field, having been founded in 1998.

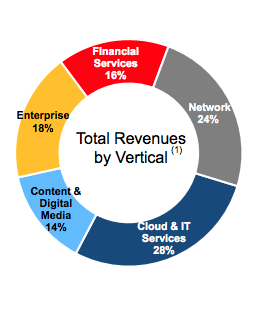

First off, the REIT boasts 210 data centers across 55 cities and five continents, so it’s diversified both geographically and by client base, with tenants across sectors:

A Diversified IT Provider

Source: Equinix February 2020 investor presentation

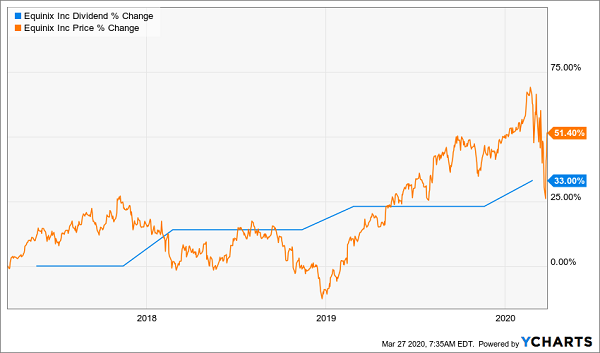

Equinix’s clients also sign on via long lease terms, and these leases have a long time left to run (18 years, on average, in this case, if all extensions are enacted). The company’s resilience is also showing up in its stock price, which is crushing the S&P 500 in this crisis:

Equinix Repeats Its Strong 2008 Performance

The stock doesn’t boast the highest yield of the bunch, at 1.9%, but Equinix has hiked the payout 57% since it originated the dividend in March 2015. It also boasts an ultra-safe payout ratio for a REIT, at just 46.6% of FFO.

Finally, the company’s rising dividend helps support the share price: you can clearly see Equinix’s stock rising with each hike in the past three years, even with the crash:

Dividend Up, Share Price Up

“Recession-Fighter” Dividend No. 3: Oracle (ORCL)

No introduction needed here: Oracle makes the software that’s essential to making businesses work. It also boasts a huge presence in cloud computing and makes servers and other hardware that power the world’s IT networks.

Like Equinix and CCI, Oracle boasts a share price that’s outperforming the market in this crisis, just like it did back in ’08:

Oracle’s “Pullback-Proof” Stock

Oracle doesn’t raise its payout religiously every year—the last hike was declared more than 12 months ago—but when it does, it goes big: the last increase was a 26% boost declared in March 2019, and the company has raised its payout a solid 380% since initiating it in 2009.

There’s one more compelling reason to give Oracle a look: a big move by one of its insiders. According to Barron’s, Oracle director Charles Moorman bought a total of 30,000 shares on March 23 and March 26, putting $972,000 of his own cash into the company. It was the biggest insider buy of Oracle stock in over 10 years.

In the words of legendary value investor Peter Lynch, “Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise.” That makes now a good time to follow Moorman’s lead.

5 “Dividend Lifeboats” Paying Big 9.4% Dividends (Buy Now)

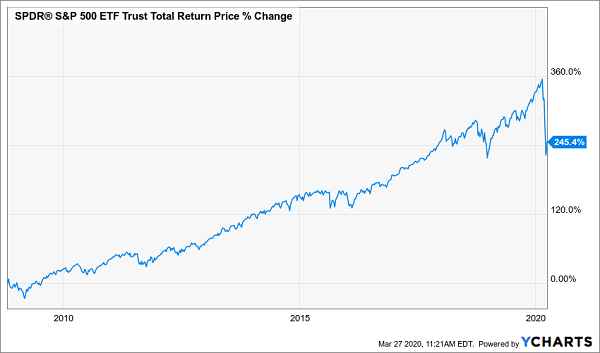

I know it’s hard to think of buying at a time like this, but history tells us it’s absolutely the right thing to do. Heck, even if you bought an S&P 500 index fund just halfway to the bottom of the 2008 disaster, you’d still be sitting on 245% in gains and dividends today.

Crisis Buying Delivers a Huge Return

And just as our tech dividends above demonstrate, we can hedge our downside (and juice our upside) by zeroing in on companies with 3 unbeatable strengths:

- Rising dividend payouts.

- Business stability, in the form of big cash cushions and reliable revenue.

- The ability to tap long-term megatrends, like soaring-mobile data use.

I’d add one more “must-have” to that list—and it’s one where our 3 tech plays fall just a little short: high current yields—I’m talking 9% and up here.

That’s why I put together my new 5-stock “recession-resistant” dividend portfolio and quickly rolled it out to investors to help counter this market crash. It delivers a huge 9.4% average dividend (with the highest payer of the bunch throwing off an amazing 13%!).

And these payouts are backstopped by some of the biggest discounts available on any investment today.

The end result: stock prices that hold their own while you collect your massive 9.4% average payout. And if you hold these stocks for, say, 11 years, you’ll have recouped your entire upfront cost in dividends alone.

Everything else is gravy!

That’s the gold standard when it comes to safe investing in a crisis, and it’s why high, safe dividends are absolutely essential right now.

Don’t leave your retirement vulnerable to wild swings in the market when you could be cutting your volatility, year after year, by getting a big slice of your return in safe dividend cash.

These 5 stocks should be at the top of your list. I’ll share my complete research on all of them, and give you their names, tickers, complete dividend histories and more, when you click right here.

Recent Comments