We all love 7% yields here. But how do you feel about Sprint’s 7.88% bonds that mature in September 2023?

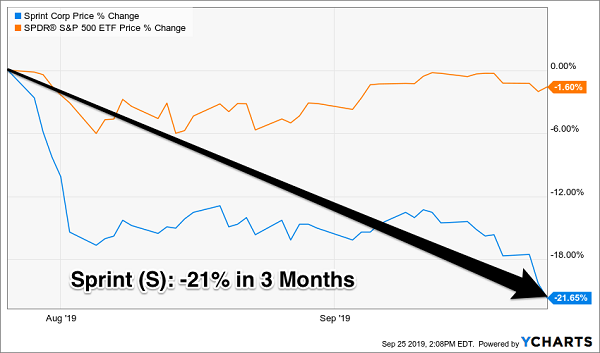

Well, the company might make it until then. Shares trade for pocket change at just over $6. Equity investors in Sprint (S), however, have been (wait for it) sprinting to the exits lately:

The Stock Feels the Weight of Sprint’s Debt

For a position this risky, I’d want to watch it closely. I’d also want to be able to sell it at the first sign of distress.

Unfortunately, that isn’t going to be possible. If you own the Sprint 2023’s, you’ve got company–$320 million to be specific!

This bond is the number two holding (0.55% of the portfolio) for the widely followed and owned iShares iBoxx High Yield Corporate Bond ETF (HYG). It is also the number three holding for America’s favorite junk yield pile, the SPDR Bloomberg Barclays High Yield Bond ETF (JNK) at 0.62% of the portfolio.

Let’s do a little back of the envelope math. These two funds have more than $18 and $10 billion in assets they manage, respectively (for $28B total). And they are piling into the same junk. Combined, they own more than $320 million in this potentially-trash piece of paper!

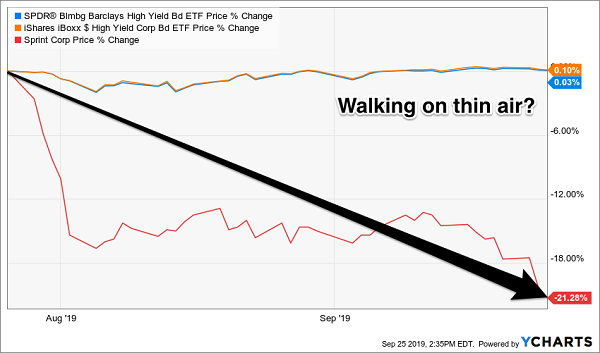

Whistling Past the Bankruptcy Graveyard?

I get it. These funds are convenient, as easy to buy as a stock. They are “diversified” with 1,894 combined holdings, at least until you start peeling back the onion. And they usually pay in the 5% to 6% range.

But you need to remember that ETFs are marketing products. They are designed to attract capital and not necessarily earn you a return on it.

Big money is spent on television, print and online advertisements. Less cash and thought are put into the actual income strategies that ETFs employ, and their lagging returns reflect it.

If the Sprint bonds begin to roll over, these funds aren’t going to be able to unwind their positions. These bonds are going to crash. And in a full-blown credit crisis, these funds are going to get whisked away.

Why are bond ETFs so bad, and what can we do to improve on them?

Let’s pick on the three biggest flaws most of these funds suffer from. Then, I’ll share a superior way to buy bonds that is just as easy.

ETF Fatal Flaw #1: Underperformance

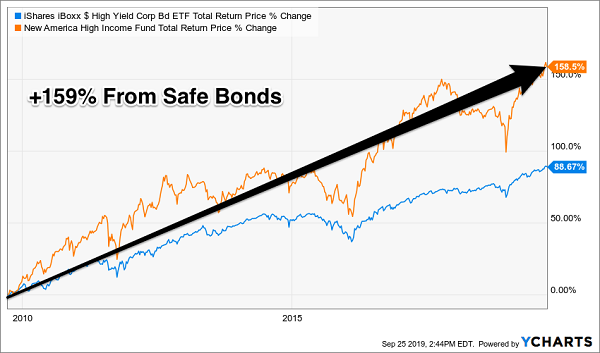

Investors who typed in “HYB” instead of “HYG” (the iShares fund above) have typo’d their way to a richer retirement. The closed-end fund (CEF) New America High Income Fund (HYB) is a better way to buy high paying bonds. It’s outperformed its ETF cousin HYG by 70 percentage points over the last dozen years:

Since inception 30 years ago, HYB has delivered outstanding returns of 9.8% per year with most of it coming as cash distributions.

The fund pays 7.5% today and it trades at an 11% discount to the street value of the bonds it holds. Investors buying HYB today are paying just $0.89 for $1 in bonds.

HYG meanwhile pays 5.3% and trades for the value of its portfolio. No discount here.

ETF Fatal Flaw #2: Ranking the Worst First

It’s no accident that both of these funds own Sprint’s paper.

“Passive” methods—building portfolios based on rules—don’t work well in the land of bonds because fixed income expertise can’t be readily pre-programmed. Top managers can deliver truly top returns.

Here’s the main reason why bond indexing is bad. Let’s consider stock indexes, which are weighted by company size. Generally speaking, the larger the firm, the more it matters in the index’s performance.

If you “buy by size” in the debt markets, it’s counterproductive. Stock market value for indexes doesn’t include debt. But bond markets are all debt by definition. Follow the computers in Bondville and you’d maximize your exposure to the bonds of the firms that borrow the most money!

That’s the opposite of what we’re looking for in bonds, where our goal is to maximize our “coupon” (the percentage yield) while minimizing our risk (and making sure we get paid back our principal).

ETF Fatal Flaw #3: False Sense of Liquidity

And here’s the “market meltdown” kicker on why you should always avoid bond ETFs:

They are subject to meltdowns if panic selling occurs.

If you sell HYG and JNK today, you’ll get your money in exchange for your shares. And it will be iShares’ and SPDR’s problem to settle up their end (by selling those 1,894 bonds en masse).

Problem is, we’re talking about bonds rather than stocks here, and there is no readily available liquid market for those bonds. Which means if a lot of selling occurs, HYG itself may take a hit if it has to unload its Sprint bonds at a discount (say, 50 cents on the dollar) to meet investors’ withdrawals. It may have to sell at any price!

CEFs like HYB don’t have this problem. They have fixed pools of assets, which help their managers ride out ups and downs. So as long as they buy good bonds that are funded by reliable cash flows, they’ll be fine.

The Best Bond Bet: CEFs for 7%+ Yields (Often Paid Monthly)

CEFs are the underappreciated darling of savvy income investors. They are better bond bets for three reasons:

- They are actively managed by pros with a legitimate “edge”,

- Their asset pools are fixed, which means they can (and do) trade at discounts to their net asset values (NAVs), and

- They get access to cheap money, which helps them lever up returns with minimal risk.

Add up these edges, and we have a superior long-term vehicle for fixed income returns. And we can buy them at a discount by being patient income-seeking contrarians. Which means we can do even better than the 9.8% that a fund like HYB provided over three decades by “cherry picking” our purchases.

Another nice benefit of HYB? It pays the same big dividend every single month.

Revealed: My 8 Top Buys for $3,333 a Month, Every Month (Forever)

And what’s better than an every-30-day payout? Monthly dividends line up perfectly with your bills and let you reinvest your dividends faster, giving your portfolio’s value a nice upside kick.

A Proven Sign of Quality

Here’s something else few people realize: monthly dividends are a crystal clear sign you’re buying a top-notch stock.

Think about it: most execs know that a dividend is a promise to investors—cut it and they’ll surely get an earful (not to mention a shriveled share price). So if management has the guts to pay monthly, you can bet they’re sure their company (or fund) has a bright future.

That’s just the type of team we want to invest with.

Which is where my “8% Monthly Payer Portfolio” comes in. The stocks and funds I’ve assembled here pay even more than THQ, LTC or RNP—an amazing 8% yield, on average, just as the name suggests!

Got a $500K nest egg? You can look forward to a nice $3,333 dropping into your account every single month. That’s a big enough “paycheck” for many folks to retire on without having to touch a dollar of their principal!

Plus, each of these stocks is cheap today, positioning you for 10%+ price upside—or another $50,000 on your $500K—in the next 12 months, no matter what happens with interest rates.

The full portfolio is waiting for you now. Click here to get all the details on these undercover 8%+ income plays: names, tickers, buy-under prices—every shred of research I have on each and every one of them.

Recent Comments