I shudder when folks tell me their portfolios can’t give them a decent income stream. Because I know there’s an easy way for them to get safe 8%+ payouts—and everyone misses it.

Let’s be honest. When it comes to investing, most people limit themselves to the blue chip stocks of the S&P 500. The problem? These stocks pay a miserly 1.2% average yield. So you’re getting a measly $1,200 in yearly dividend income for every $100K invested!

No one is retiring on that—unless they have a couple million bucks lying around.

But there is another way. It’s a potent income generator I’ve been specializing in for more than a decade—and sharing with investors through my CEF Insider service.

The hint is right in the service’s title: CEFs, or closed-end funds. They’re a collection of 500 income investments that yield an outsized 7% on average, or nearly six times what the typical S&P 500 stock pays.

That makes them the antidote to the record-low dividends offered by stocks—and a great way to counter inflation’s drain on your income stream, too.

I’ve collected three specific funds that would make savvy additions to any portfolio as we head into 2022. They yield even more than the CEF average, paying an outsized 8.2% between them. And they’re also sporting ridiculous discounts to their true value—22% off in one case!— setting you up for quick price appreciation as those deals disappear.

More on this trio of income plays in a moment. First, let me explain how you can tell if a CEF is trading at an attractive discount. It’s a key indicator you can find on any fund screener.

The Deal on the Discount

Unlike ETFs and mutual funds, CEFs tend to trade at prices different from their portfolio value (which we refer to as the net asset value, or NAV). When they’re priced higher, we say the fund trades at a premium to NAV. And a fund trading for less is priced at a discount to NAV.

This disconnect happens because CEFs can’t issue new shares to new investors, and this causes their market prices to separate from the value of their investments.

Our job? Buy when those discounts get historically wide, then ride along as they snap back to normal, pulling the fund’s market price along with them.

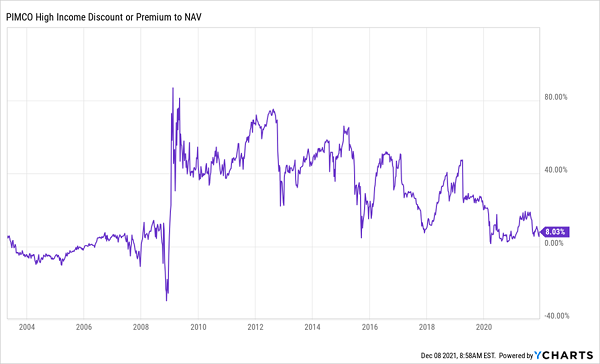

And CEF discounts and premiums can get very extreme: look at the history of the PIMCO High Income Fund (PHK).

From Cheap to Expensive and Back Again

As you can see, PHK often trades at a premium. That’s because CEF investors love funds from PIMCO, a well-known name in the CEF business, but their love wanes during crises, which is why the ridiculous 80% premium PHK boasted in the past has shrunk over time, and its “modest” 8% premium today is much lower than what you would’ve paid over the last decade.

But that doesn’t mean PHK is a buy now, because there’s no reason to pay its premium price when 60% of the CEFs on the market trade at discounts—sometimes discounts of more than 10%!

In other words, if you buy a CEF that trades for 10% less than its portfolio is worth, it’s like getting shares of Apple (AAPL), say, or whatever assets the fund holds, for less than you would if you bought that stock on the open market.

That’s also partly how these funds can pay such high dividends, since the yield on their portfolio is lower than the yield they pay out based on their market price, so long as they’re trading at a discount.

For instance, a fund trading at a 10% discount and yielding 7% on its market price only has to get about 6.3% in income and capital gains to prop up that 7% payout. Furthermore, CEFs are actively managed by professionals who buy and sell with the ebbs and flows of the market, passing off profits to us as income along the way.

Now that we’ve got a firm handle on the discount to NAV, let’s see it in action with three of the best bargain-priced CEFs to pick up as we roll into 2022.

CEF Pick #1: A “1-Stop Shop” for Stocks and Bonds Paying 9.8%

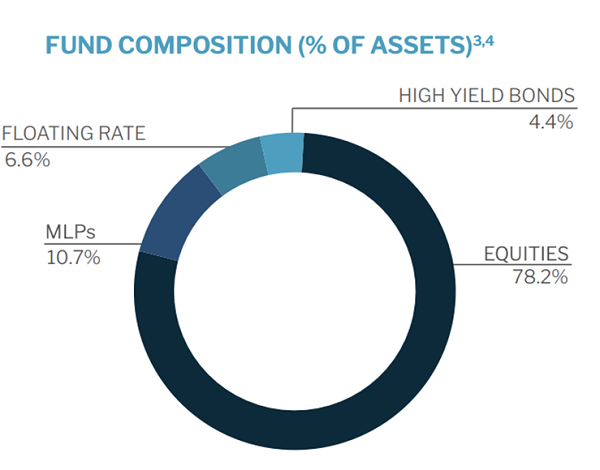

Our first pick is the Highland Global Allocation Fund (HGLB), which is small enough to deliver us some quick price gains (with just $201 million in assets under management) but big enough to give us the liquidity we need to get in and out easily.

And talk about a high payout—as I write this, HGLB yields a whopping 9.8%. It also has a huge discount to NAV: 20.2%, to be exact, making it the second-cheapest CEF on the market.

Source: Highland Funds

That bargain valuation is totally unjustified. With a mix of stocks, high-yield bonds and senior loans (more on those in my analysis of our third CEF pick, below), HGLB is a one-stop shop for stocks and bonds, with income coming from a nicely diversified portfolio.

HGLB also invests in real estate, so as rents go up, its holdings benefit. And right now, rents are skyrocketing across the board and particularly on the residential side, with the average rent on a one-bedroom apartment in the US up a staggering 20% in November from a year ago, according to Apartment Guide’s latest report.

CEF Pick #2: An Energy Titan Throwing Off a 6.5% Payout

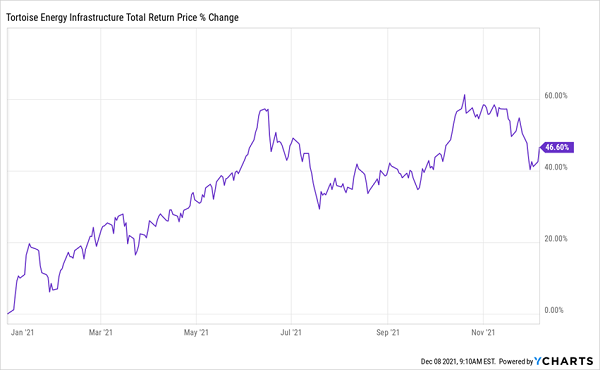

The Tortoise Energy Infrastructure Corp (TYG) has been a bad bet in the past, and I’ve panned it when it deserved to be criticized. But the past is the past, and with inflation kicking up, energy prices are taking off, pushing TYG higher.

TYG: a Smart Inflation Hedge

The fund mainly holds master limited partnerships—higher-yielding firms that operate oil pipelines—including industry leaders like Enterprise Products Partners (EPD), Energy Transfer LP (ET) and ONEOK LP (OKE).

(You may have heard that investing in MLPs means you get a complicated K-1 package for reporting your dividend income at tax time. But investing in MLPs through a CEF eliminates that problem. You’ll get the much simpler Form 1099 instead.)

With a 46.8% return in less than a year, TYG has proven it’s making the right moves, but the market still hasn’t stopped punishing it, despite its turnaround. With a 22.4% discount to NAV, it is the most heavily discounted CEF on the market, even though it’s in the top 4% in terms of returns for 2021. Oh, and TYG yields a solid 6.5% that management only needs to earn 5.7% to cover, thanks to the fund’s big discount. That’s an easy return for them to get in this market.

CEF Pick #3: A Smart Way to Play the Fed for 8.3% Dividends and Gains

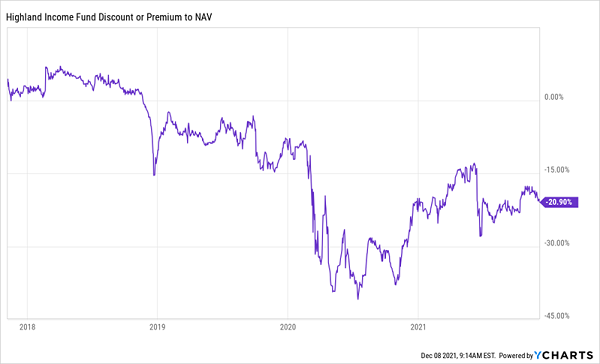

Another attractive option from Highland is the Highland Income Fund (HFRO), a holding of Dividend Swing Trader, a sister service to CEF Insider. HFRO has a unique focus: senior loans, which go up in value when the Federal Reserve raises interest rates, as it has hinted it’s going to start doing next year. That makes HFRO a timely buy now, especially with the fund trading at a historically wide 21% discount and yielding an outsized 8.3%.

HFRO’s Buy Window Opens

Investors began to realize this at the end of last year, causing HFRO’s ridiculous 40% discount to shrink, but it’s still at an unusually generous level. This means capital gains are likely as investors buy more senior loans.

When market trends shift next year, we may see a different mood, and HFRO could trade at the premium it fetched in 2018 (when the Fed was raising rates). That makes now a good time to buy and ride along as the discount dissolves.

My Top 4 CEFs Yield 7%+. They’re “Spring-Loaded” for 20%+ Gains in 2022

These 3 are far from the only CEFs sporting big discounts as we roll into 2022. The 4 “essential” CEFs I’m urging EVERY investor to buy now are screaming bargains, too! You can get their specific names and tickers right here.

These 4 funds yield a rich 7%, on average, and as their unusual discounts snap back to normal, I fully expect them to catapult their prices to 20%+ price gains in the next 12 months.

When you add their big dividends, you’re looking at an easy 27%+ total return by this time next year!

I’m sure you’ve been told that you can have either a big dividend or big gain potential in one investment, but never both. Well, CEFs turn that so-called “wisdom” on its head!

I want to share my complete research on these 4 “must buy” CEFs with you now. Go right here and I’ll take you on a guided tour of each one. You’ll learn their names, tickers, current yields and discounts, the track record of their management teams and much more.

Recent Comments