Since traditional banks have backed off on business lending over the years, BDCs (business development companies) have stepped in. They provided much-needed debt, equity, and other financial solutions to small businesses—and much-needed income to dividend investors.

As an asset class, BDCs yield 8%. We’ll discuss three popular payers—with dividends up to 8.3%—in a moment.

Congress whipped up BDCs with a few pen strokes in 1980, creating a structure that’s incentivized to provide smaller companies with financing. BDCs receive special tax privileges, and in exchange, they must return at least 90% of their taxable profits to shareholders as dividends.

If that sounds familiar, that’s because that same tradeoff is enjoyed by real estate investment trusts (REITs), which were formed the same way, 20 years prior.

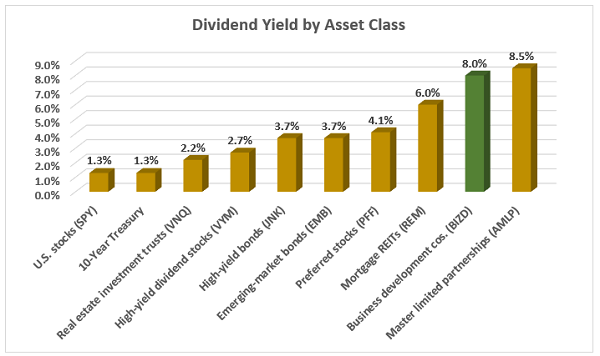

As with REITs, the provision that BDCs must dole out 90% of their income as dividends leads to super-sized yields. An average yield of 8% is huge:

That’s an 8% Yield … On AVERAGE

Source: Contrarian Outlook

Just make sure you explore this industry with your eyes wide open.

The BDC space is notoriously difficult—both to operate in, and to invest in. Business development companies do have to compete with other sources of financing; they tend to invest in smaller companies, which are exceptionally sensitive to economic conditions; and they’re difficult to assess given minimal information about their portfolio companies. (Track records matter in this space.)

But if you want to take a stab at some truly life-changing yields with the potential for growth, it’s difficult to match these PE-esque stocks.

Today, I’ll introduce you to three BDCs that are showing potential.

PennantPark Floating Rate Capital (PFLT)

Dividend Yield: 8.9%

Back in February, I explored a few high-yield plays that could actually get a jolt from rising interest rates.

Remember: BDCs are lenders. To varying degrees, they can deal in loans with a “floating-rate” component—and the higher interest rates go, the higher the BDC’s profits.

Enter PennantPark Floating Rate Capital (PFLT).

PennantPark’s current portfolio is around 100 middle-market companies, scattered across 42 different industries. These firms include the likes of glass distributor American Insulated Glass, marketing service Phoenix Marketing International and veterinary hospital services provider Pathway Partners.

As the name implies, PFLT makes these investments almost entirely through floating-rate senior secured loans.

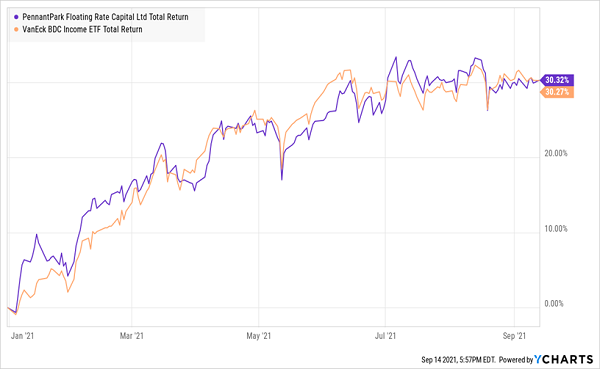

That exposure seemed like a blessing at the start of the year, when interest rates appeared poised to take off amid an unbridled economic recovery. But then they didn’t. Rates turned tail, in fact, from 1.7% in March back down to 1.3% today, and PFLT has plain ol’ industry-matching performance to show for it.

PennantPark Floating Rate Capital’s Takeoff Is Delayed

On the one hand, PFLT still offers up a high dividend—paid monthly, no less—and is among the best-positioned BDCs for whenever interest rates finally bounce off the bottom.

The flip side? Dividend safety remains a question mark. I mentioned that in February, Janney Montgomery Scott’s analysts forecasted that PFLT wouldn’t earn enough net interest income (NII) to cover the dividend in both 2021 and 2022. Well, more recently, Oppenheimer concurred, saying NII would fall short of the core $1.14 in dividends that PennantPark is projected to pay out.

Main Street Capital (MAIN)

Dividend Yield: 6.1%

Main Street Capital (MAIN) is the closest thing the BDC industry has to a dependable blue-chip stock.

This $2.8 billion business development company provides debt and equity capital solutions to lower-middle-market companies, and debt financing (primarily floating-rate first lien senior secured debt) to middle-market firms.

Its typical target company generates annual revenues of between $10 million and $150 million, and roughly $3 million to $20 million in EBITDA. The portfolio currently stands at 177 investments, with the largest one representing just 3.2% of total investment income. Meanwhile, no single industry makes up more than 7% of the portfolio by cost, and MAIN is even diversified geographically, with no less than 15% invested in any one of five U.S. regions.

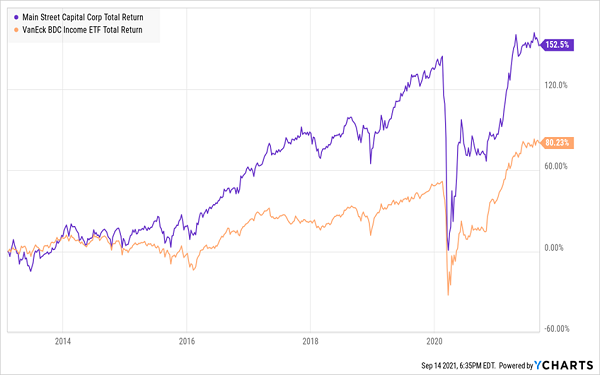

Distributable net investment income (DNII) has improved every single year since 2007, and its long-term performance largely reflects that tale.

Main Street Capital Is Heads-and-Shoulders Above the Rest

That pattern is a little spottier on a per-share basis—while DNII grew between 2018 and 2020, DNII per share of $2.76 in 2018 actually declined to $2.66 in 2019, then $2.26 in 2020. But things are clearly normalizing in the short-term. Trailing 12-month DNII is 11% higher than 2020’s total, and up 6.6% on a per-share basis.

In fact, things are so good that Main Street even returned to growing its regular dividend, by 2.4% to 21 cents monthly. That might not sound like much, but it’s better than what most of the rest of the industry has done over the past couple of years. Not to mention, Main Street has a history of issuing special dividends from excess profits—it quit during the pandemic to keep its regular payout intact, but a return to normalcy could mean an eventual return to that extra cash.

The biggest rub is an unsurprising one. Investors tend to flock to best-in-class operators, and that’s clearly the case in MAIN shares, which trade at 1.8 times the company’s net asset value—one of the fattest premiums in the entire industry.

Prospect Capital (PSEC)

Dividend Yield: 9.3%

Prospect Capital (PSEC) is another massive BDC with $6.2 billion invested across 124 portfolio companies. It primarily does business via first- and second-lien senior loans and mezzanine debt, though it will also invest in products such as collateralized loan obligations (CLOs), marketplace lending and multifamily real estate.

Like Main Street, Prospect Capital spreads its investments around a wide range of industries, from energy to healthcare to financial services to food. But worth noting is a fairly large concentration risk—namely that 20% of the portfolio is invested in National Property REIT, making it even more difficult to assess PSEC given that the REIT is essentially its own portfolio of 58 properties.

Sized at $3 billion in market cap, Prospect Capital is one of the few BDCs that are larger than Main Street. But it’s rarely considered to be in the same class … at least, not by income investors. That’s because PSEC has a pockmarked dividend history that has seen the BDC cut its monthly payout in both 2015 and 2018. That has largely kept a lid on shares long-term.

Does Prospect Capital’s Recent Outperformance Have Staying Power?

It also means investors should keep a close eye on PSEC’s ability to meet its obligations. And right now, it looks like the BDC has little room for error. Most estimates for 2021 and 2022 have Prospect Capital’s NII just a cent or two over or below its projected 72 cents per share in annual dividends.

The “A” Squad: Monthly Payers Doling Out 7%-Plus Yields

No monthly payout—even one delivering a whopping 9.3% in annual income—is worth buying today if you can’t count on it tomorrow.

That’s the rub with so many high-yielders, isn’t it?

It has a nice yield … but you can’t depend on it.

I love this payout … but the stock is so overpriced.

Fortunately, if you’re ready to take action and whip your retirement plans into shape right now, my “A” squad has everything income investors need, right here, right now. No settling. Certainly no “buts.”

My “7% Monthly Payer Portfolio” is an elite set of high-income, high-frequency dividend payers that, at current prices, are smack-dab in the middle of our ideal “buy zone.” And as the name suggests, these 7% dividends are paid out to investors each and every month.

Many of the picks in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate not just massive yields, but shockingly aggressive price performance. That allows us to do the unthinkable from an income strategy: double our money much more quickly than traditional blue-chips-and-mutual-funds portfolios.

These dividends aren’t just good.

They’re not just great, either.

They’re downright life-changing.

If you drop $500K—less than half what most financial gurus suggest you need to retire—into this powerful portfolio now, you’d kick-start a $35,000 annual income stream. That’s more than $3,000 a month in regular income checks!

The time to get in is now, while you can still buy these names at bargain prices. Click here to get everything you need—names, tickers, complete dividend histories and more—instantly!

Recent Comments