How much money do you need to retire on dividends alone?

This is a better question to ask than the typical “magic number” formula that most “first-level” thinking firms tout. Let’s review why their approach is fatally flawed, so that we can derive a more reliable method of our own based in actual reality (and funded by actual dividend payments.)

Fidelity Says What?

You should aim to have 10 times your final salary in savings.

But why? I suppose they are claiming that, if you earned $100,000 in your final year working, that you’ll want to earn this much in income every year for the rest of your life.

So, Fidelity says save a million bucks and you’re in good shape.

But how exactly is $1,000,000 supposed to throw off $100,000 in excess income annually?

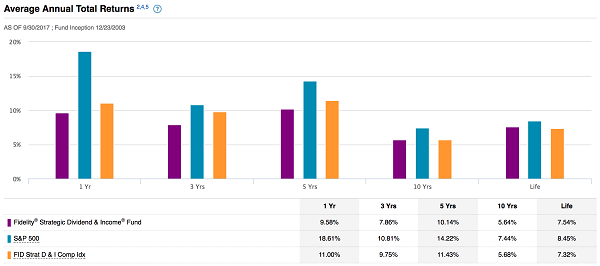

Fidelity’s Strategic Dividend & Income Fund (FSDIX) pays 2.38% today. Which means, if you follow their advice to a tee, and buy their flagship income fund, you are earning $23,800 per year in income from your million-dollar stake.

That’s a start. But where exactly is the other 76.2% of you income supposed to come from?

Apparently this is up to us to figure out, because we’ve run out of sage advice from this respected investment firm. So let’s see if we can piece together a full retirement ourselves.

Shall We Also Withdraw 4% Annually?

We saved a million like they said, and we’re earning less than our neighborhood coffee barista. I presume we’re now supposed to sell shares to make up the difference. Most mainstream-following financial advisors say that we can sell 4% of our portfolio annually for income, so let’s try this.

FSDIX has returned 7.54% annually since inception, so a 4% yearly drawdown appears sustainable. However, we see three glaring pitfalls.

First, another 4% means another $40,000 per million for a total of $63,800. Still not what we are looking for.

Second, this particular fund has underperformed the S&P 500 over the last year, three years, five years and ten years. It’s also underperformed the broader market since inception (2003).

So what exactly was the point of buying a dividend fund when we were going to have to sell shares anyway? And see them appreciate less than a dumber, cheaper index fund?

FSDIX (Purple Bar) Underperforms – Always

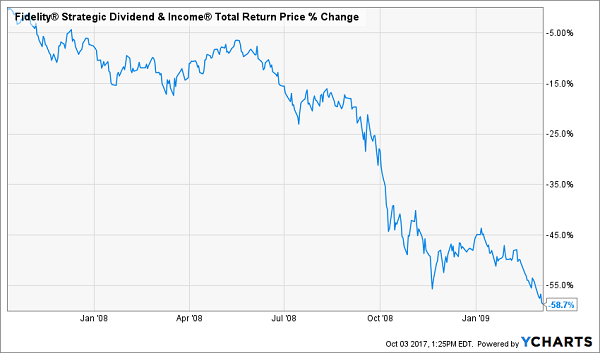

More concerning than mere mediocrity, however, is the threat of “reverse dollar cost averaging.” Peak to trough in 2008, FSDIX lost 59% of its value. If you’re selling stock for income, you’re selling more and more at lower and lower levels:

You Don’t Want to Be Selling Here

By July 2012, FSDIX investors who bought at the 2007 peak – and held 100% of their shares – had grinded their way back to even.

Buy who actually buys and holds? In reality, there are two types of investors:

- Those who bought during 2008, 2009, and 2010. They made money much sooner, because they were able to buy low.

- Those who sold during the downturn. Whether they had to sell for income, or simply got scared – many of these portfolios have still not recovered.

Back to Even (But Most Did Much Better, or Much Worse)

Dollar cost averaging is a powerful force. Make sure it’s working for you, rather than against you. Here’s how.

Fade the 4% Fallacy for a Smarter “Magic Dividend Number”

Our retirement approach is grounded in reality versus fantasy and false math. So, let’s begin with the value of your actual portfolio.

Back to the $1 million example. Let’s say we saved that money like Fidelity said to, and we still want $100,000 per year.

We’ll ditch the flawed notion of selling capital for income, and live on dividends alone. This means our portfolio’s “magic yield” is 10% annually.

But today, there’s only one safe 10% yield left on the board. And I wouldn’t recommend putting your entire portfolio in only one issue, no matter how sound its payout seems.

So, we’re faced with a decision. We can:

- Settle for less income, or

- Save (or make) more money.

While I wouldn’t recommend an entire portfolio of double-digit payers, I do like seven stocks (and funds) yielding an average of 8.3% today.

Their dividends are safe, and believe it or not, their prices are a bit undervalued to boot. This means we should enjoy price upside as well, and achieve 10%+ annual returns on these dividend machines.

Let’s talk more about these income plays, because you should be tuning out the “first-level” pundits – those who do little or no original thinking – and replacing your underperforming payers with these meaningful (and safe) 8.3% yields.

3 Ways to Safely Bank 8.3% Dividends

Most of the stocks you read about in the mainstream media that pay 5% or better are train wrecks. They have big stated yields for the wrong reason – namely, because their prices have been axed in half or worse over the past year!

For example, retailer Macy’s (M) pays 7.2% on paper. But its business model is toast. Next quarter’s payment may happen, but that’s a risky game I’m not willing to play.

Instead, I’d rather look in corners of the income world that aren’t combed over as regularly. There are three in particular that I like today. You won’t hear about them on CNBC, or read about them in the Wall Street Journal, because they don’t buy advertising like Fidelity and other firms.

Their relative obscurity is great news for us 8.3% dividend seekers.

Play #1: Closed-End Funds

If you feel trapped “grinding out” dividend income with classic 3% payers (like dividend aristocrats), you can double or even triple your payouts immediately by moving to closed-end funds, or CEFs. In fact, you can often make the switch without actually switching investments.

I’ll discuss my favorite CEFs in a minute.

Play #2: Preferred Shares

Not familiar with preferred shares? You’re not alone – most investors only consider “common” shares of stock when they look for income.

But preferreds are a great way to earn 7% and even 8% yields from the same blue chips that only pay 2% or 3% on their “common shares.”

I’ll explain preferreds – and my favorite tickers to buy – after we finish our high yield hat trick.

Play #3: Recession-Proof REITs

The IRS lets real estate investment trusts, or REITs, avoid paying income taxes if they pay out most of their earnings to shareholders. As a result these firms tend to collect rent checks, pay their bills and send most of the rest to us as a dividend. It’s a sweet deal.

Not all REITs are buys today, however – landlords with exposure to retail space should be avoided.

That’s easy enough to do. I prefer to focus on REITs that operate in recession-proof industries only. I want to receive my rent check powered dividends no matter what happens in the broader economy.

Now let’s discuss how you can get a hold of my complete “8.3% No Withdrawal Portfolio” research today, along with stock names, tickers and buy prices. Click here and I’ll share the specifics – and all of my research – with you right now.

Recent Comments