“First-level” investors – those who buy and sell on headlines – mistakenly believe that real estate investment trust (REIT) profits will suffer if rates rise.

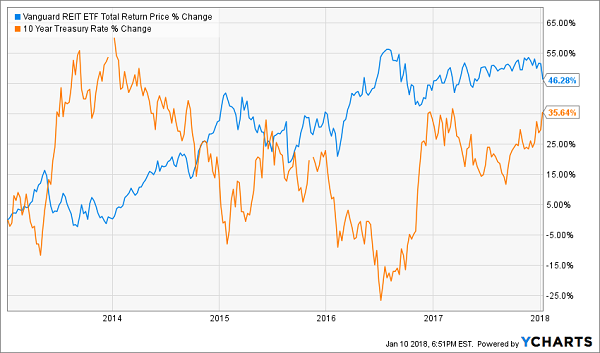

Sure, in the short run, the “rates up, REITs down” theory puts on quite the show. When the 10-Year Treasury’s yield rises, REITs usually fall. And when its yield drops, REITs usually rally. This inverse relationship tends to hold up over multiple days, weeks and even months:

A Short-Run Seesaw Between REITs and T-Bill Yields

However the “long view” shows that many of these short-term moves are merely noise. It is possible for REITs and higher rates to coexist in profitable harmony:

But Long-Run REITs and High Rates Can Co-Exist

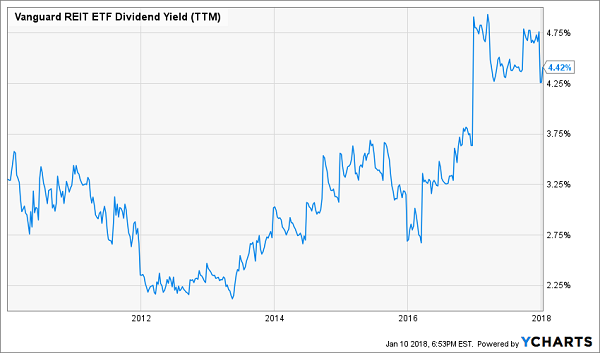

Investors who are bailing on REITs are missing out, because they are currently paying their highest yields this decade:

Highest REIT Yields Since the Financial Crisis

Most income hounds get it wrong. They pile into REITs when their yields are low because they are desperate for any positive income stream. That’s a bad idea because there are only two ways REITs can pay you:

- With today’s dividend, and

- With tomorrow’s (hopefully higher) payout.

As with stocks in general, it’s usually a bad move to accept a lower-than-usual dividend today in hopes of future growth. That’s a sure way to guarantee underperformance.

A better strategy is buying stocks – especially REITs – when their yields are higher than usual. Over VNQ’s 11-year history, its price has tended to mirror its yield:

Buy VNQ When Yield is High

The Best REITs to Buy for Rising Rates

The behind the “rates up, REITs down” price action says that, because these landlords borrow money to grow their property empires, they need cheap cash. Yet this isn’t a “must have” criterion for all such firms. If their costs increase, they can simply raise the rents when the lease is up for renewal, passing on their higher borrowing costs to tenants.

For example, let’s look at a three-year period starting in May 2003 when the 10-year rate climbed two full basis points – from 3.2% to 5.2%. Based on recent REIT price action, you’d expect most firms would be out of business!

But blue chips such as mall operator Simon Property Group (SPG) and self-storage stalwart Public Storage (PSA) not only survived the rate increases – they thrived:

The Best REITs Climbed With Rates

Why? Because rising rates signaled a booming economy – one in which these firms had no problem raising their rents. Both boosted dividends while investors in each stock enjoyed 129% total returns over the three-year period!

Which REITs Will Thrive This Rate Hike Cycle?

Firms having no problem issuing rent increases today are easy to spot. They report higher and higher funds from operations (FFO) year after year, which finds its way back to shareholders in the form of an ever-rising dividend.

FFO represents the amount of cash a REIT actually generates from its operations. It’s where our dividend originates – which makes it the building block for everything else in the REIT-world.

FFO is the driver of dividend growth for REITs. Figure out where FFO is going, and you know where the payouts are heading – and how fast.

If FFO is stagnant, a firm can only increase its payout by increasing its payout ratio. And this isn’t sustainable over time.

Rising FFO on a per share basis, on the other hand, will basically force management to raise its dividend. And that’s what ultimately drives the stock price higher, because dividend growth is all that matters for REITs. Figure out where the dividend is going, and you know where the stock price is heading.

2 Dividend Growth REITs to Buy Right Now as Rates Rise

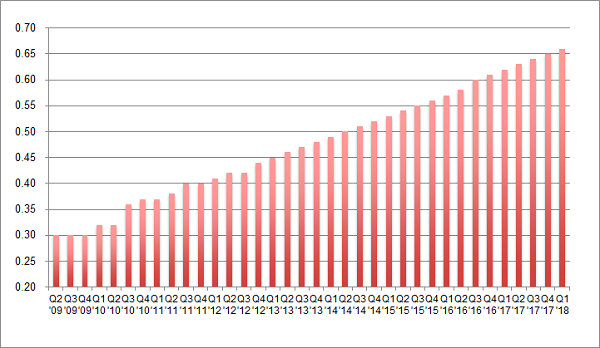

My favorite REIT just raised its dividend again by 4% over last quarter’s payout. This marks the 22nd consecutive quarterly dividend hike for the firm:

Dividend Hikes Every Quarter

It pays a 10% yield today – but that’s actually a 10.5% forward yield when you consider we’re going to see four more dividend increases over the next year. And the stock is trading for less than 10-times funds from operations (FFO). It’s ridiculously cheap.

This sale won’t last long. I expect its valuation and stock price will rise by 25% over the next 12 months as more money comes stampeding into its REIT sector – which makes right now the best time to buy and secure a 10.5% forward yield.

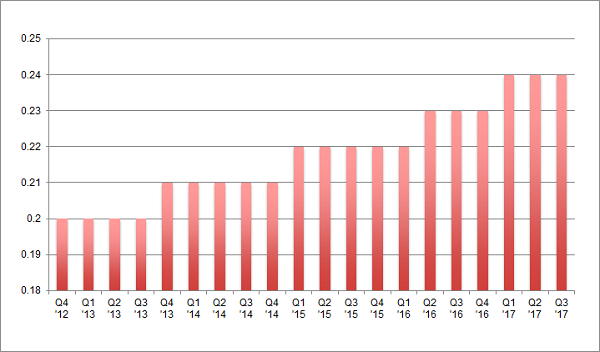

Same for another REIT favorite of mine, a 7.4% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years.

The firm’s investors have enjoyed 86% total returns over the last five years (with much of that coming back as cash dividends.) And right now is actually a better time than ever to buy because its growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

An Accelerating Dividend

This stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof,

- It yields a fat (and secure) 7.4%, and

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at.

Remember, there’s never been a better time to buy REITs and live off their dividends. But it’s important to choose wisely.

To help you play this trend profitably, I’ve put my research into a newly updated special briefing. It includes details on the 3 most promising REIT sectors ahead, the two you absolutely must avoid and details on my 2 favorites picks right now (one of which pays a whopped 9.7% dividend!).

Click here to read The Best bargain REITs for 7%+ yields for 2018 now.

Recent Comments